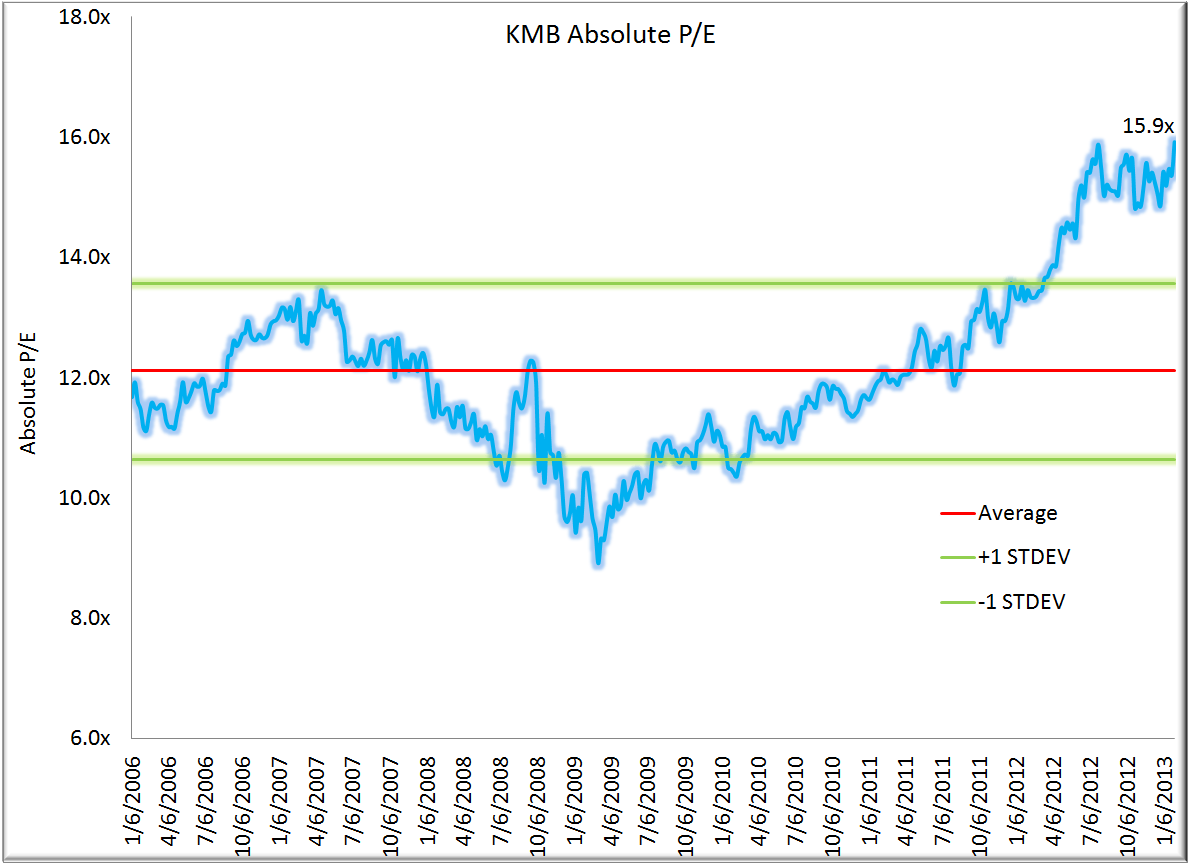

We have been vocal in our dislike for KMB at these levels given what we see as a deterioration in earnings quality - valuation is getting stretched and Keith is getting the signal to short.

Have a great weekend,

Rob

We have been vocal in our dislike for KMB at these levels given what we see as a deterioration in earnings quality - valuation is getting stretched and Keith is getting the signal to short.

Have a great weekend,

Rob

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.