TODAY’S S&P 500 SET-UP – February 1, 2013

As we look at today's setup for the S&P 500, the range is 26 points or 0.88% downside to 1485 and 0.86% upside to 1511.

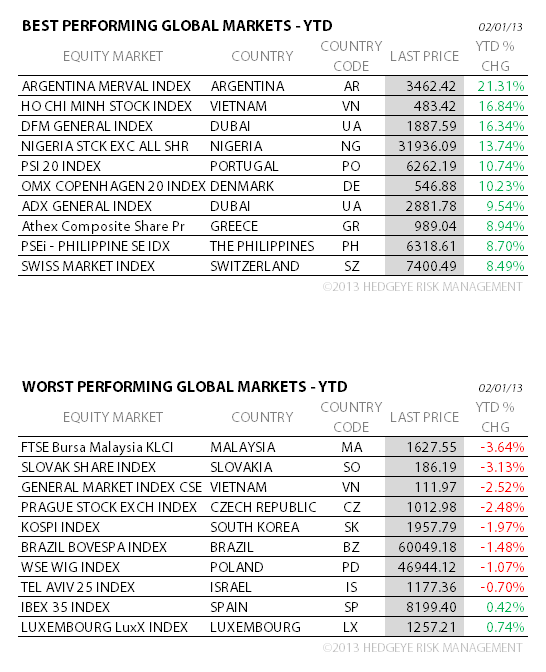

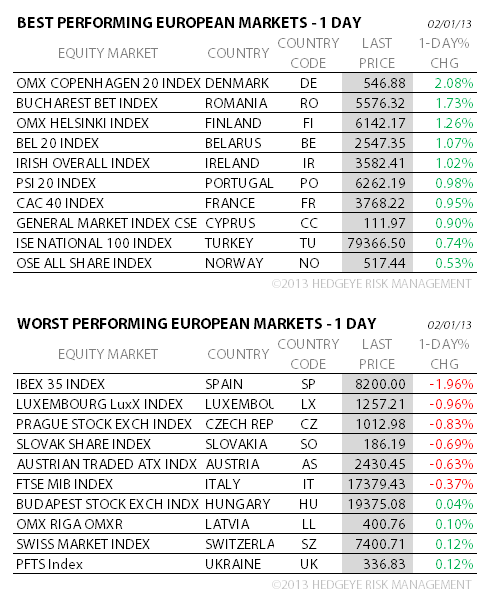

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

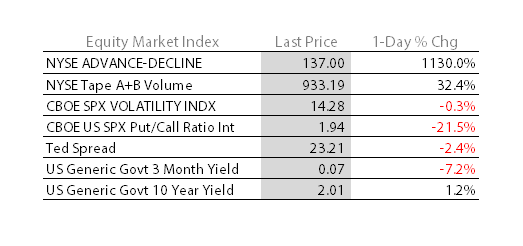

- YIELD CURVE: 1.74 from 1.72

- VIX closed at 14.28 1 day percent change of -0.28%

- FLOWS – pundits (specifically perma bears) can kick and scream about this not happening all they want – on the margin (where trading macro matters most), it’s happening. US Equity Fund Flows (ex-ETFs) positive for the 4th consecutive wk, showing inflows of $5.8B (vs $3.7B last wk). If this jobs report is good, 10yr yield could hit 2.09% today alone.

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Nonfarm Payrolls, Jan., est. 165k (prior 155k)

- 8:30am: Unemployment Rate, Jan., est. 7.8% (prior 7.8%)

- 8:30am: Fed’s Dudley speaks at New York Bankers Association

- 8:58am: Markit US PMI Final, Jan., est. 55.5 (prior 56.1)

- 9:55am: U. of Mich. Conf Final, Jan., est. 71.5 (prior 71.3)

- 10am: Construction Spend M/m, Dec., est. 0.6% (prior -0.3%)

- 10am: ISM Manufacturing, Jan., est. 50.6 (prior 50.2)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- House meets in pro forma session, 11am

- SEC advisory panel meets on rules for small, emerging companies under federal securities laws, 9:30am

- Washington Day Ahead

WHAT TO WATCH

- U.S. payrolls probably expanded at a quicker pace in Jan.

- AB InBev may need to sell brewery to end U.S. Modelo lawsuit

- Apple loses U.S. court bid to block Samsung Galaxy Nexus phone

- Jan. auto sales: Light-vehicle sales may have risen 14%

- Pfizer’s Zoetis raises $2.24b pricing IPO above range

- China’s manufacturing sustained expansion in Jan.

- Euro-area Dec. unemployment rate holds at 11.7%, est. 11.9%

- Abe shortens list for BOJ chief as Japan faces monetary overhaul

- Google submits antitrust proposal to EU commission, Almunia says

- MetLife sees Provida deal adding about 5c/shr to 2013 earnings

- Apple TV said to start carrying HBO shows in 1H of 2013

- Wal-Mart gains 60-Day hiatus from picketing in U.S. labor accord

- China approves HSBC’s sale of Ping An stake to Thai billionaire

- Dell buyout by CEO, Silver Lake possible on Feb. 4: Reuters

- Rajaratnam 2-time tipper Roomy Khan gets 1 yr in prison

- China Export Rebound, IPad, ECB, Super Bowl: Wk Ahead Feb. 2-9

EARNINGS:

- Mattel (MAT) 6am, $1.15 - Preview

- Newell Rubbermaid (NWL) 6:30am, $0.42

- AON (AON) 6:30am, $1.25

- Brookfield Office Properties (BPO CN) 7am, $0.21

- Imperial Oil (IMO CN) 7am, $1.00 - Preview

- Lear (LEA) 7am, $1.38

- Legg Mason (LM) 7am, $0.53

- Merck (MRK) 7am, $0.81 - Preview

- National Oilwell Varco (NOV) 7am, $1.44

- Tyson Foods (TSN) 7am, $0.42

- Ingersoll Rand (IR) 7am, $0.70

- LyondellBasel (LYB) 7am, $1.14

- WisdomTree Investments (WETF) 7am, $0.04

- Beam (BEAM) 7:01am, $0.66

- Domtar (UFS) 7:30am, $1.36

- Perrigo (PRGO) 7:51am, $1.31

- Brink’s (BCO) 8am, $0.68

- Tidewater (TDW) 8am, $0.42

- Exxon Mobil (XOM) 8:04am, $2.00 - Preview

- Chevron (CVX) 8:30am, $3.06 - Preview

- Franklin Resources (BEN) 8:30am, $2.38

- NuStar Energy (NS) 8:54am, $0.38

- Cymer (CYMI) 9am, $0.04

- NuStar GP Holdings LLC (NSH) 9am, $0.38

- Globus Medical (GMED) 4pm, $0.19

- Realogy Holdings (RLGY) 4:25pm, $(0.11)

- Brown & Brown (BRO) Post-mkt, $0.27

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- LME’s Only Woman Floor Trader Quits to Join Hong Kong Exchanges

- Copper Trade Most Bullish in 15 Months on Recovery: Commodities

- Blast at Pemex Headquarters in Mexico City Kills 25, Wounds 101

- Oil Heads for Longest Run of Weekly Gains Since 2004 on Economy

- Copper Set for Biggest Weekly Advance in Four on Chinese Revival

- Wheat Rises as Lingering U.S. Drought Curbs Production Outlook

- Gold Rises in New York as Investors Await U.S. Employment Report

- Robusta Coffee Advances on Top-Producer Vietnam; Sugar Rises

- Billionaire Singer’s Fund Sees Gold Rally Amid Losing Wager

- Rebar Climbs to 8-Month High on China Manufacturing, Home Prices

- Brent Oil Rally May Stall Near $118 a Barrel: Technical Analysis

- Carbon Swings Hit Year High Amid Supply Concern: Energy Markets

- Reshaping Panama Canal Trade Means Boom in U.S. Gas Flow to Asia

- Gold Exports Caving No Bar as Deficit Stabilizes: Turkey Credit

CURRENCIES

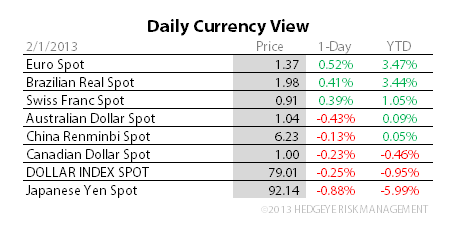

YEN – getting Taro Aso’d to a fresh new low this morning as the old band (Japan’s Serial Money Printers) buy 10.3% of ESM (Europe) debt in January. Take their word for it, they are burning their currency.

EUROPEAN MARKETS

GERMANY – with a manufacturing PMI print of 49.8 in JAN (vs 46 in DEC), there are very few countries in our GIP Model (Growth, Inflation, Policy) that look as good as Germany does right now = Growth Accelerating, Inflation Decelerating. Contrary to popular Keynesian belief, there is big upside to a strong currency – and that is the Euro right now, new high at $1.36 vs USD.

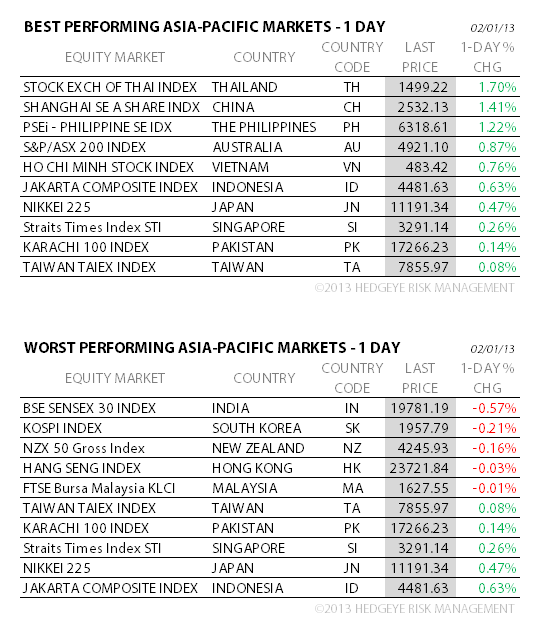

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team