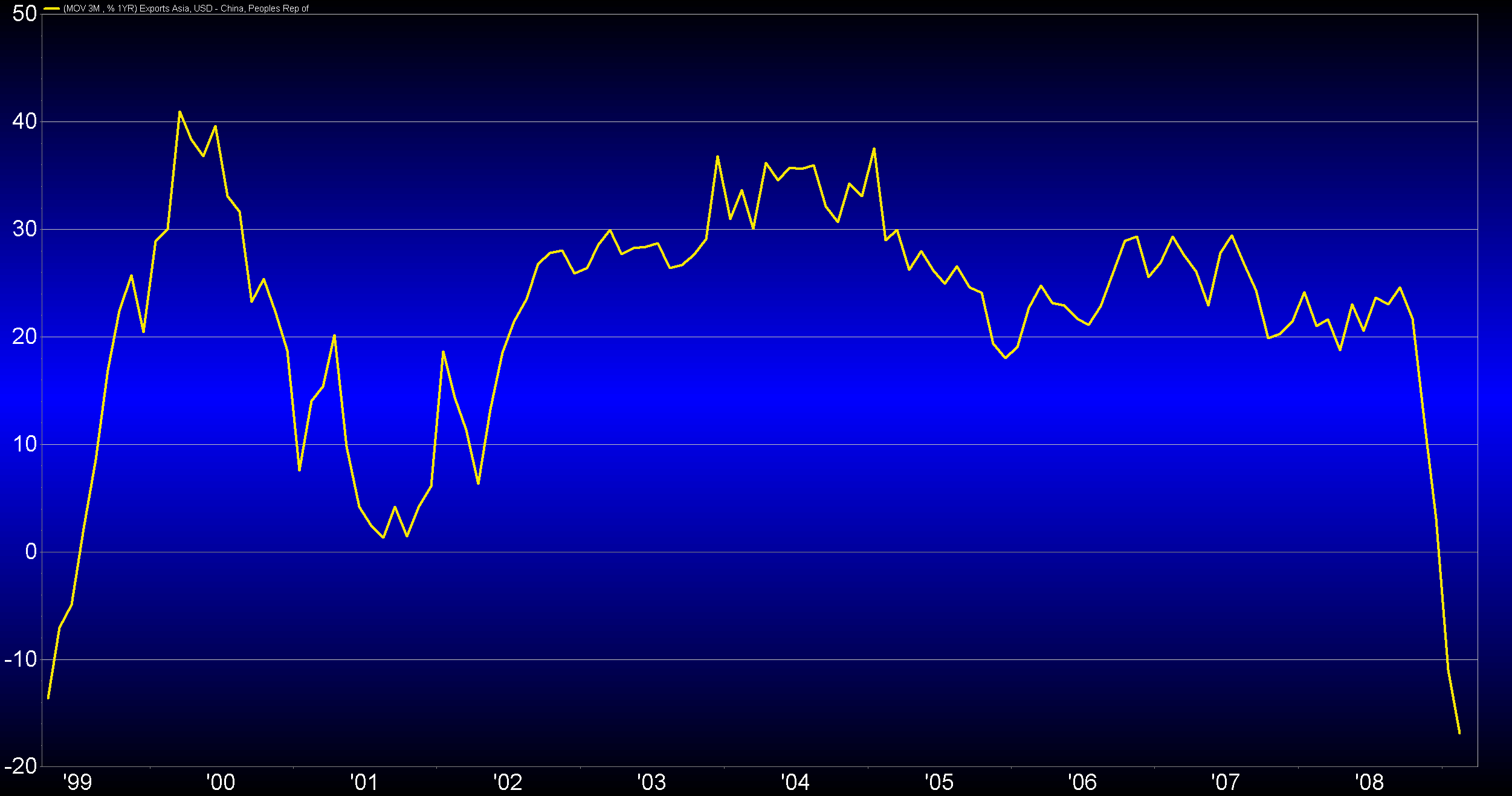

Check out the 17% decline in exports out of China for the month of March – the fifth month in a row of export erosion. The chart below showing the 3-month moving average is ominous, showing the sharpest drop in, well…ever.

Even if you’re in the camp that China makes up these numbers, the trend here is pretty tough to ignore. This plays right into my theme that China’s efforts to relax VAT taxes and other price restrictions will swing the margin pendulum back into the hands of the US apparel/footwear supply chain. Add that to SG&A cuts, capex cuts, the delta on sales and gross margins getting ‘less bad,’ and what I think are estimates that have largely bottomed. That makes it tough for me to NOT be exposed to US retail. Check out my 3/31 post entitled ‘Retail Narratives Don’t Get More Powerful Than This’ for full detail as well as my favorite names.