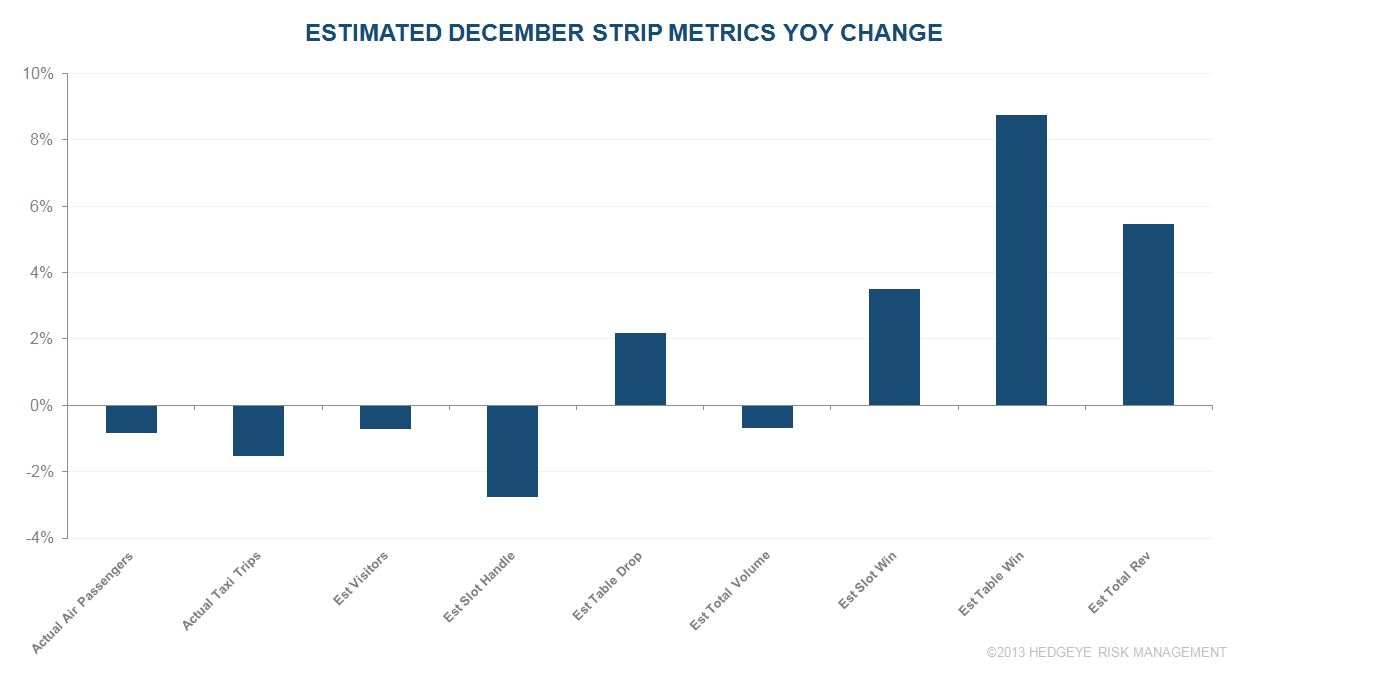

But not as good as we thought as taxi/airport traffic were worse than expected

We had previously indicated that the Strip gaming revenues could be up double digits YoY due to easy hold comparisons, particularly on the slot side. However, with airport traffic down 0.8% and taxi trips down 1.5%, lower volumes are likely to eat into that hold tailwind. We now see YoY growth in the +4-7% range assuming normal hold. December slot hold is always lower than normal as 12/31 revenues do not get counted by the Gaming Board. So for our purposes, we are projecting a December normal of 6.2% slot hold versus a "normal" normal of 7.4%.

More importantly, we are expecting slot handle and table drop ex baccarat to fall YoY. Baccarat volume and hold are always big wild cards so we pay less attention to those metrics on a month to month basis. With volumes like these, the headline print should look better than underlying fundamentals. Sorry folks, but Vegas (and most domestic markets) is not recovering and that's bad for MGM.