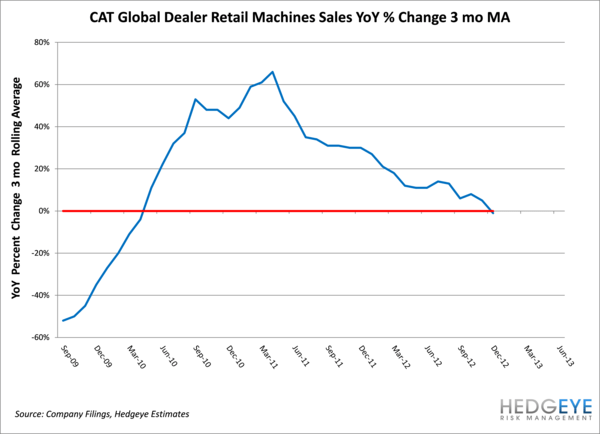

Caterpillar’s (CAT) dealer sales mirror that of durable goods in that both have been steadily weakening since Q2 of 2011. We don’t expect a rebound in CAT’s sales in the near-term as dealers and various corporations focus on reducing inventory and shift away from resource industries. Combined with a decline in mining capital expenditures over the last few quarters, CAT has its work cut out for the first half of 2013.