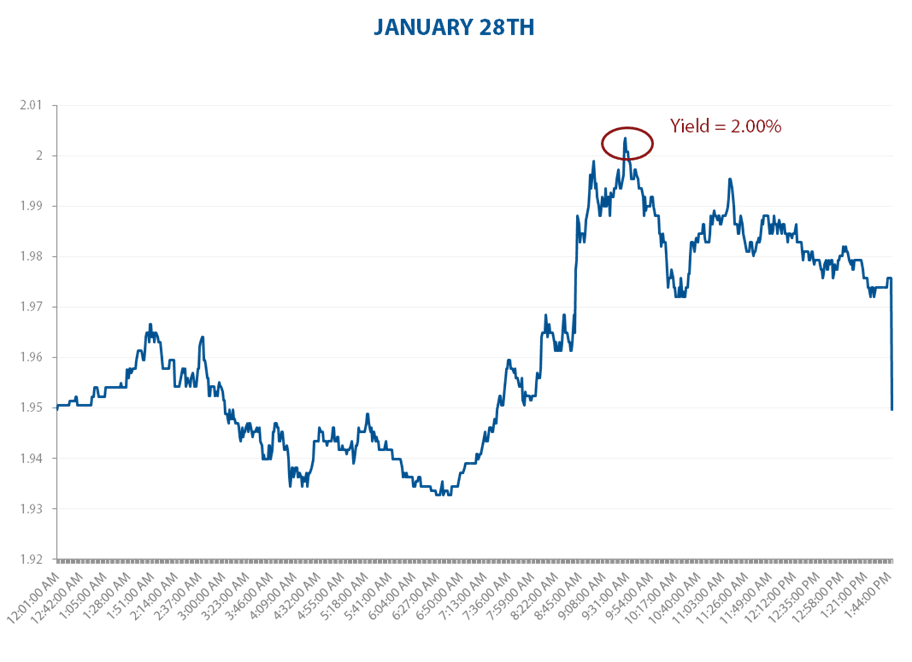

This morning, the yield on the 10-year Treasury Note hit 2.0%, a level not seen since April of 2012. Despite moving back down to 1.95% shortly after, the 10-year continues to hold above our TAIL risk line of support at 1.84%. We could soon see the 10-year yield flirting with 2.4% over the next three months, particularly if our call on US unemployment stabilizing continues to take hold. #GrowthStabilizing is good for stocks, bad for bonds. Friday's jobs report should play a role in determining if a yield above 2.0% is here for good.