Our experience is that consumer staples generally lag a "risk on" market such as we have seen since January 1st. This has not been the case to start 2013 - staples have outperformed the broader market (+6.5% including agricultural services and protein, +5.5% core staples vs. the S&P +5.4%) since January 1st. Admittedly, the world doesn't change when the calendar rolls over, but let's run with it.

Outside of the agricultural service names and protein - likely investors getting positioned for the new crop year, which is consistent with our views - the best performing sectors have been household and personal care (+7.5%, 2.4% of which came from PG's performance on Friday) and packaged food (+6.4% to start the year). We are a bit surprised by packaged food's performance - a highly defensive sector. Part of it may be that people are looking at 2012 laggards and part of it may be investors looking at the possibility of lower input costs (again, consistent with our initiation call back in December).

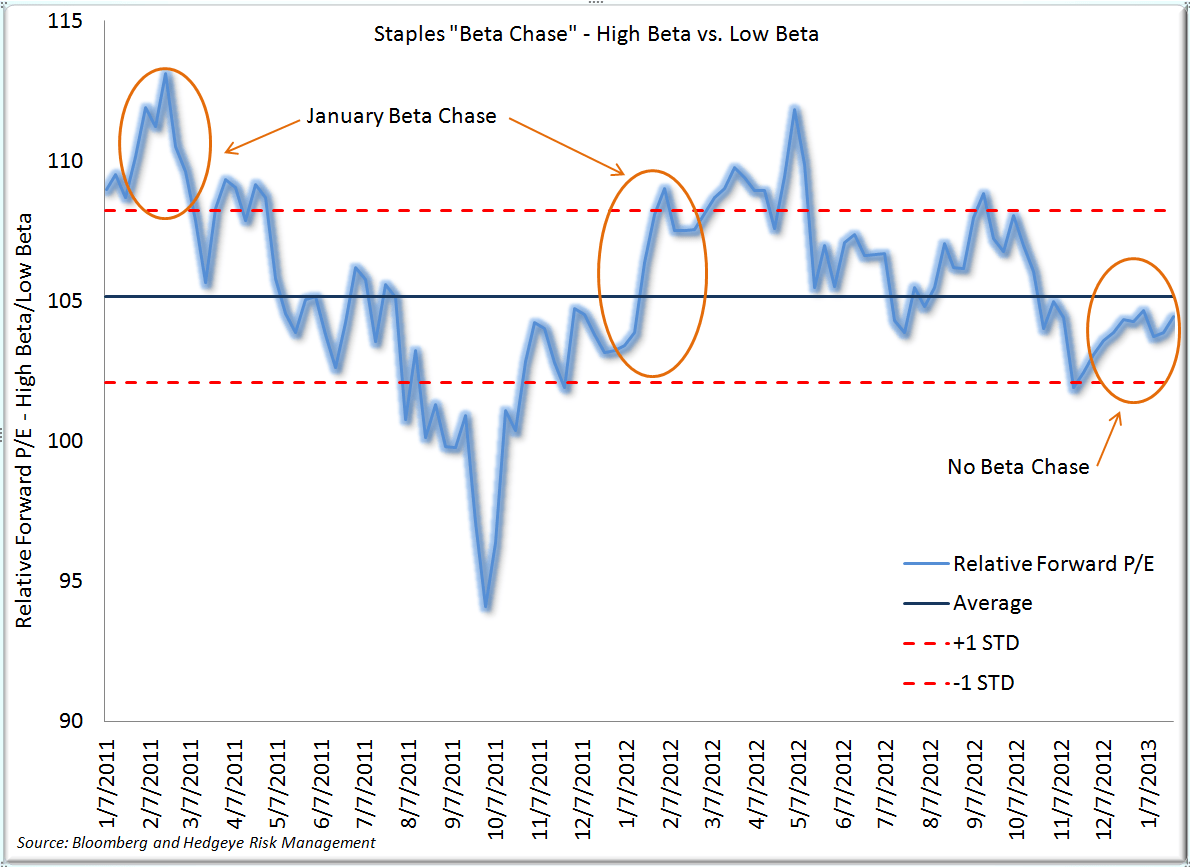

Also somewhat surprisingly, investors have broken the pattern of the last two years and not put risk on within the staples sector to start the year. Generally, we see higher beta names outperform lower beta within consumer staples when the calendar turns. That has not been the case thus far in 2013.

This year to date performance, accomplished absent any significant upward EPS revisions, has left the valuation of the consumer staples sector somewhat stretched versus recent history.

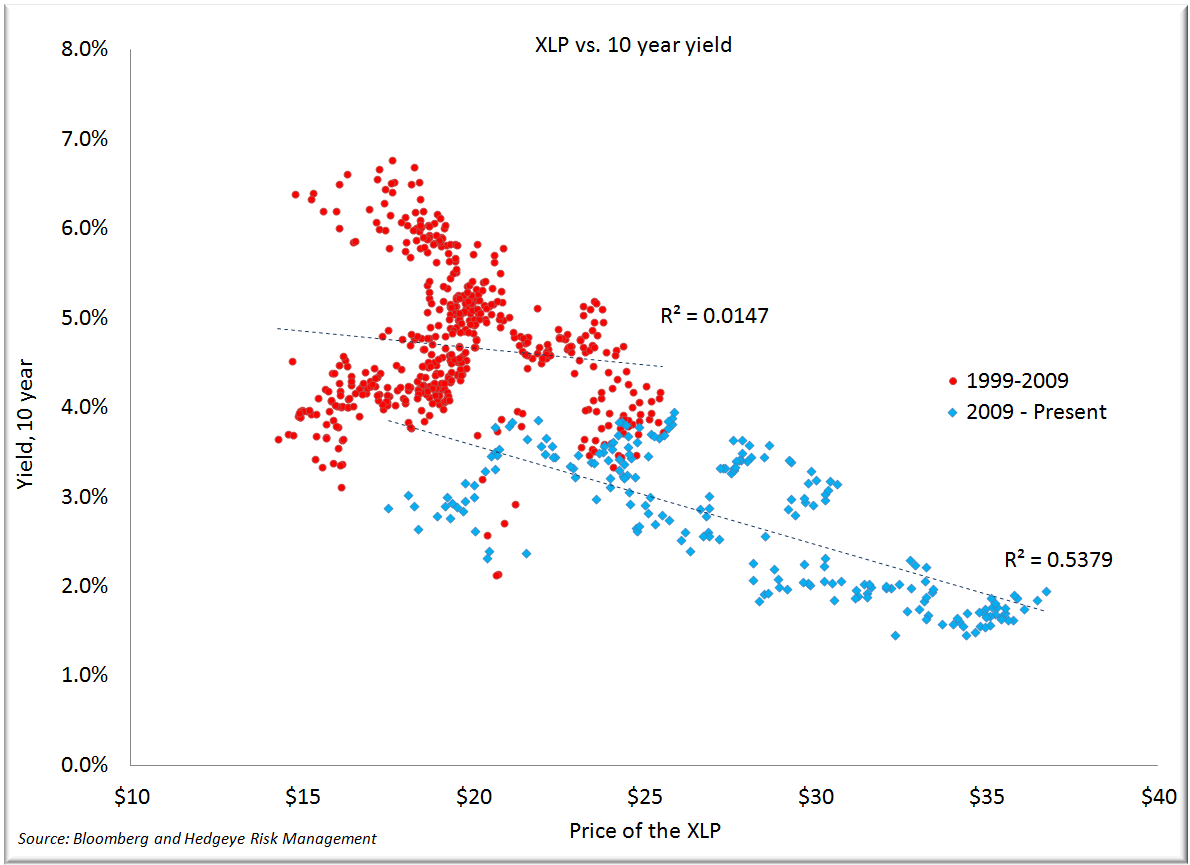

The consumer staples sector performance has been somewhat confounding for another reason - the sector has become increasingly sensitive to changes in yields on government securities in recent years, a theme we discussed at length on our initiation.

In fact, the spread between the yield on the 10 year and the yield of the XLP has decreased 44 bps (from -139 to -95 bps) in just a few weeks. This represents a combination of the price performance of the XLP and the fact that yields have crept higher.

We are left with the relative out-performance of the sector in the face of two potential headwinds - a "risk on" market and a relatively less attractive yield profile. So, we went searching for an answer and tested a few possibilities.

Our first though was short covering. Short covering has been a powerful theme to start the year - just ask the shorts in NFLX. We looked at the short interest ratio for individual stocks as of December 31st and the associated absolute performance to start the year. No dice - R2 of 0.0052.

Next, we looked at names that lagged in 2012, anticipating investors positioning for some regression to the mean in the sector. Again, no luck, as you can see below.

We then asked the question "what if investors simply don't believe this move up in the market?" In that case, the go to move would be to try and participate in as safe a way as possible, with limited downside should the economy stall or negative news flow surrounding the debt ceiling debate increase in intensity. The consumer staples sector makes sense in that context. In fact, we have heard some investors suggest that they were waiting for a better entry point, anticipating broad weakness as the debt ceiling debate looms.

We examined this possibility by looking at the performance of the XLP versus the performance of the Citi Economic Surprise Index (an index that purports to measure the gap between expectations and reality with respect to multiple economic data points). When the index is rising, data is better than expectations, and consumer staples generally lag. When the index is falling (as it is currently), the XLP tends to perform well as expectations are not being met by the reported data. Imperfect, indeed, but directionally and intuitively compelling.

Where does that leave us? A quick summary:

-

Very good performance to start the year across consumer staples

- The trend of risk on within staples to start the year has been broken

- Valuations have become somewhat stretched

- Not seeing short-covering or chasing laggards

- Investors may be playing "offensive defense" by buying staples in the face of a rising market they might not necessarily believe in

If this move up in the market is "real", and to the extent that more investors start to believe that, money should flow from staples. Alternatively, if those investors that are on the sideline are correct, staples will decline, albeit not as significantly as the broader market. So, it follows that we are getting more cautious across the sector. Our preferred shorts remain TAP, KMB, PM and either GIS or CPB in packaged food. We are sticking with our preferred longs:

- STZ - event stock with near-term catalyst

- CAG - valuation remains compelling

- PG - positive bias to EPS estimates (versus KMB short)

- ADM - most compelling way to play new crop year (though no clear view on upcoming EPS)

One more thought - for those investors that can, options are broadly inexpensive and stock replacement strategies might make sense particularly as we are getting more and more cautious on the group given the dynamics outlined in this note. Finally, the upcoming earnings season will be revealing in terms of business momentum and the likely direction of EPS revisions. We prefer to pick our spots (like we did with PG) where we either see risk or opportunity in single stock ideas.

Have a good week,

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst