We have a bullish bias on Germany within Europe. This week we received three pieces of data from Germany that we think are worth calling out:

- Germany PMI Manufacturing 48.8 JAN Prelim (exp. 46.) vs 46.0 DEC; PMI Services 55.3 JAN Prelim (exp. 52.0) vs 52.0 DEC

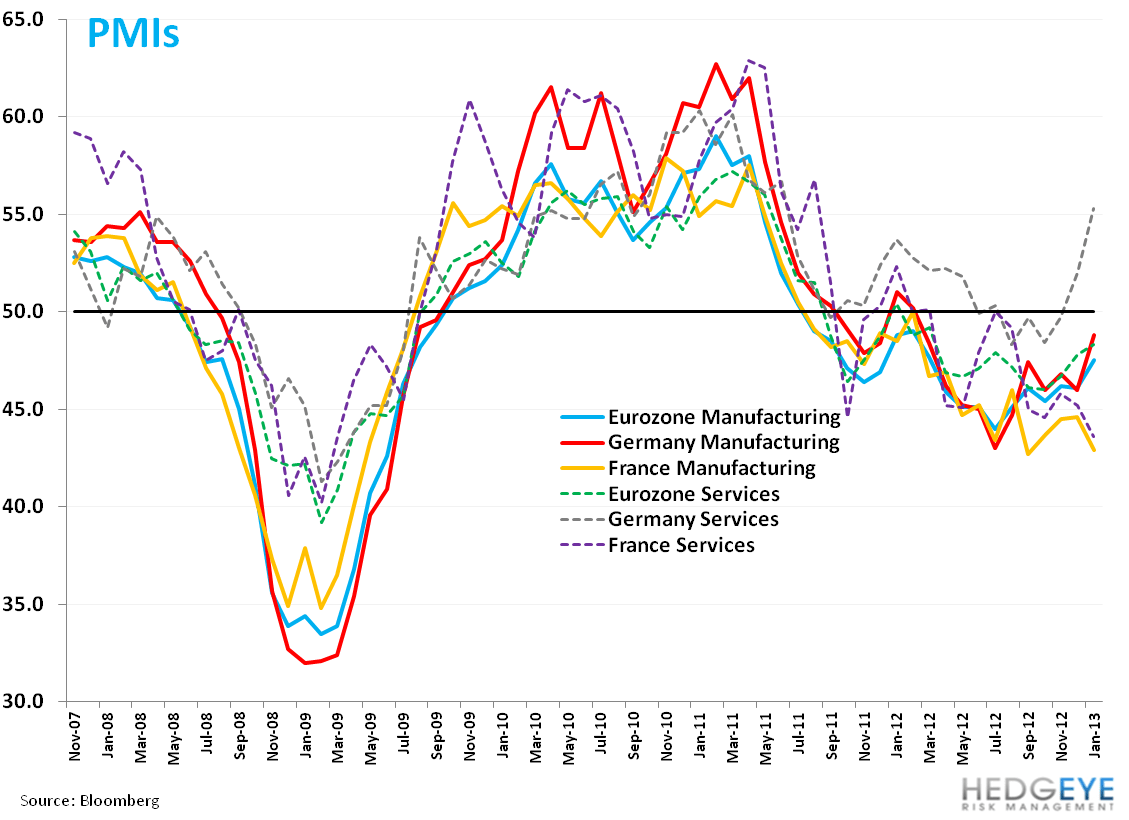

Germany is leading the charge in the Eurozone according to its PMI readings. Services are comfortably above the 50 line dividing expansion (above) and contraction (below). Here we caution that the numbers could be ahead of themselves as the underlying economic climate of the region is still working off a sluggish base. While Germany can lead in economic performance, the German economy cannot materially inflect without underlying improvement from the region given its dependence on its neighbors as export buyers. To this end, French PMIs looked abysmal for the region’s second largest economy. France’s Manufacturing slowed to 42.9 in JAN vs 44.6 DEC and Services fell to 43.6 in JAN (exp. 45.5) vs 45.2 DEC. The Eurozone PMI Composite figure gained to 48.2 in JAN vs 47.2 DEC but still stands in contraction.

- Germany ZEW Economic Sentiment 31.5 JAN (exp. 12.0) vs 6.9 DEC

The huge bounce in the 6-month forward looking economic ZEW sentiment survey month-over-month (a three-year high) may be overdone and we caution against slower, and even lower, numbers from this survey as we move further into 2013. Interestingly, we also saw a huge bounce in the Eurozone survey, 31.2 JAN vs 7.6 DEC.

- Germany IFO Expectations 100.5 JAN (exp. 98.5) vs 98.0 DEC

The IFO survey confirmed the move in the ZEW earlier in the week, which gave investors more powder to be optimistic. Consensus estimates for German GDP in 2013 are in a range of +0.5% to 0.7%. If this is as good as it gets for the Eurozone’s largest economy, it’s not that great, which could limit the run in these high-frequency surveys.

Matthew Hedrick

Senior Analyst