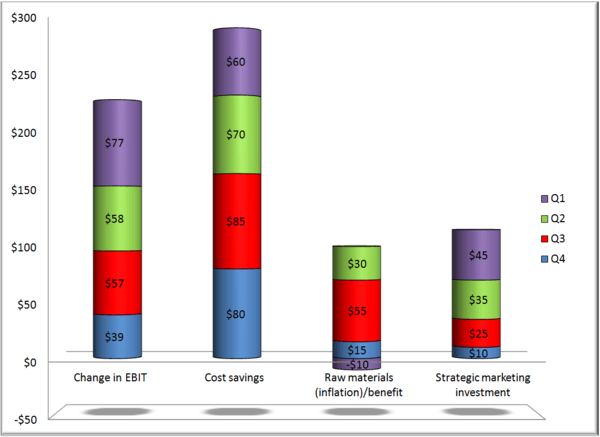

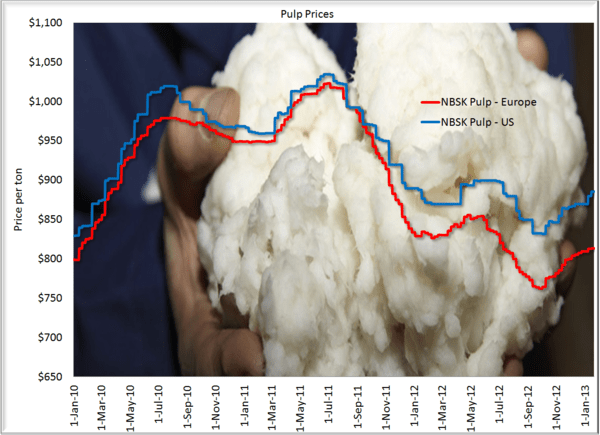

After shorting Kimberly Clark (KMB) in our Real-Time Alerts yesterday, we covered our position this morning. Though the company was essentially in-line with expectations for its earnings, there’s a lot more pressure on KMB than investors think. Commodity prices like oil and raw pulp are moving against the company, which reinforces our bearish bias on the stock. We don’t think people should pay up for 3-4% top line growth and EBIT growth that’s largely derived from restructuring savings.

We outlined earlier this week how the long PG/short KMB trade could be an idea worth considering...when the timing is right, of course.