On Sunday, Germans in the state election of Lower Saxony (Niedersachsen) narrowly voted down Chancellor Angela Merkel’s party, the Christian Democratic Union (CDU). Below we explore the implications of the defeat and conclude that although this is a meaningful blow to her party, and will tilt the Bundesrat (upper house of parliament) to the opposition, it will not break the Chancellor’s back in terms of her chances of reelection this September. However, it will likely spell a change in the CDU’s coalition partners, and legislative gridlock until then.

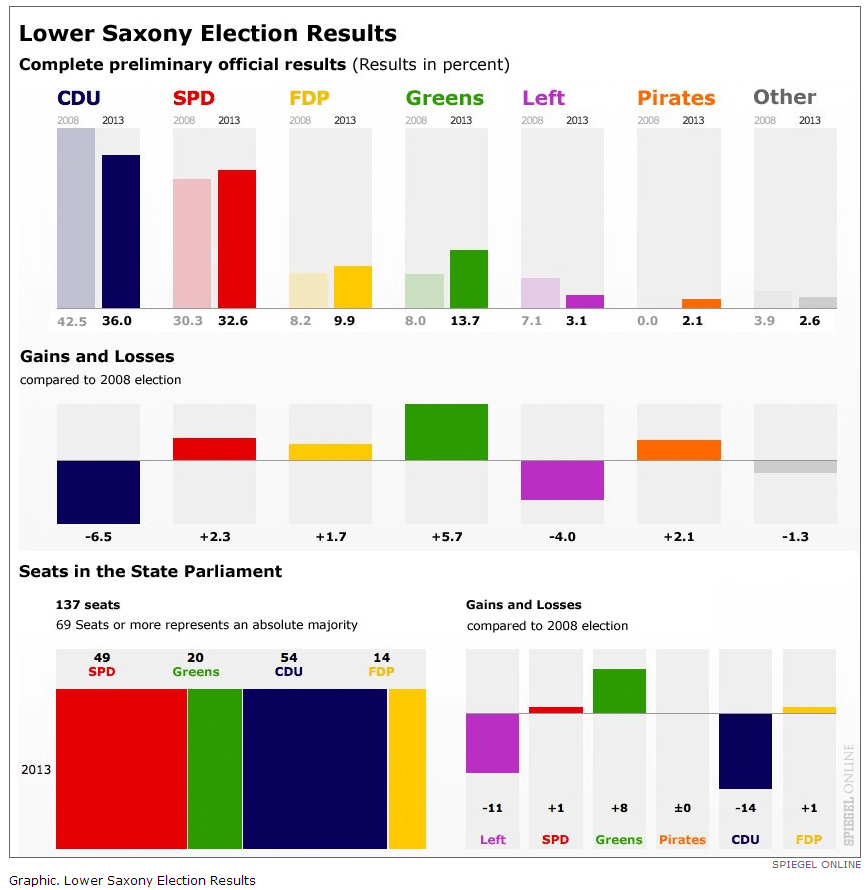

The center-left coalition of the Social Democratic party (SPD) and its allies the Greens party (known as the red-green coalition) won a one-seat majority over the center-right coalition of Merkel’s CDU party and the Free Democratic Party (FDP), or a combined 69 seats vs 68, in the state parliament of Lower Saxony on Sunday.

Despite optimism leading up to the vote from the incumbent Lower Saxony CDU state premier David McAllister (a half-Scot) on a “come-from-behind victory”, the CDU garnered only 36% of the votes cast, or a loss of -6.5% versus its past performance of 42.5% in the previous state election of 2008. Notable share gains came at the hands of the Greens +5.7% to 13.7%; SPD +2.3% to 32.6%; and FDP +1.7% to 9.9%.

It’s important to note that there were fears going into the vote that the FDP would not garner at least 5% of the vote, the minimum needed to win seats in the state parliament, many would-be CDU voters tactically voted for the FDP. This in fact changed the complexion of the state vote enough to favor the red-green coalition and with it tipped the balance of the Bundesrat (upper house of parliament) to an absolute majority in favor of Merkel’s opposition.

The shift in the upper house does have teeth. Essentially it means that the opposition in the Bundesrat can block major legislation that Merkel’s coalition, which has a majority in the Bundestag (or lower house of parliament), tries to pass.

Practically speaking, we expect Merkel’s policy maneuverability to be limited going into federal elections in September, which could result in a much more cautious tone on such international issues as the ongoing Eurozone debt crisis and atomic energy as well as her domestic agenda. In conclusion, we are expecting legislative gridlock into September which will only be perpetuated if Merkel’s center-right coalition manages to retain power in September – a not so unfamiliar set-up for Americans to envision given the disunity across the U.S. houses of congress.

Merkel’s Contender, Steinbrück

The results of the Lower Saxony vote have a few broad implications as we look down the road to September.

First, the inaction or gridlock we expect to see on the policy front across the upper and lower houses should keep Merkel tight lipped which could play into the hands of her main contender, Peer Steinbrück. Steinbrück was nominated to lead the SPD in October and originally proved his worth as Merkel’s finance minister during the 2007-2009 financial crisis.

Second, the win in Lower Saxony for the SPD-Greens will remain a psychological tailwind, if nothing else. A quick refresher on the recent German political scene shows that in the span of a few months Steinbrück made repeated political gaffes, which most speculated would cost his party the election in Lower Saxony.

In particular, Steinbrück proclaimed that German Chancellors were underpaid, a severe misstep given his highly publicized earnings for speaking engagements over the last three years (estimated at €1MM) and especially given the SPD party platform as one representing the working class.

In fact, Steinbrück’s gaffes directly led to an evaporation of the center-left’s approval in the months leading up to the election in Lower Saxony, so much so that state Premier McAllister even suggested that Steinbrück should continue to visit the state more often.

Therefore, it’s the ability of the party to succeed despite him, rather than because of him, that could give him and his party momentum into September. Steinbrück has outlined a campaign platform including a cap on housing rent increases, the introduction of tougher banking rules, a push for a minimum wage, and tracking down wealthy tax evaders. However, his key initiatives have been criticized from members inside and outside of the party as too tax and finance related, which again may also be at odds with the working class ideals of the SPD. Finally, it’s still a toss-up if his sharp and sometimes combative personality (in contrast to Merkel’s more cautious demeanor) will prove an asset or liability into September.

The popular, trusted Chancellor

What is clear is that Merkel still remains a strong favorite to win a third term. A Forsa public opinion survey released last week put the SPD at 23%, its lowest rating since mid-2011, versus 43% for Merkel's conservatives. Further, when asking pollsters who they would vote for if chancellors were elected directly, only 18% of respondents said they would pick Steinbrück, whereas 59% chose Merkel.

Merkel’s support has been largely anchored on German approval of the way in which she has handled the Eurozone crisis, but there’s room for concern that Merkel may be resting too much on her laurels and not pushing a directed campaign. From what has been issued, Merkel supports creating equal opportunities for all, including immigrants; delivering job security and fair wages; and ensuring equitable living standards for seniors and those living in the “depressed” east.

Yet Merkel must be careful to not further alienate party supporters that charge her with a leftward shift in the party in recent years – one aimed at winning more cosmopolitan voters through policies to better support childcare facilities and monetary assistance to child bearing couples.

While Merkel's CDU-FDP has now lost to the SPD and Greens in five states over the past two years, including in the long-time southern stronghold of Baden-Wuerttemberg and in the northern industrial powerhouse of North Rhine-Westphalia, it’s clear Merkel and her CDU party still command a decided rating advantage, which she can likely maintain even without the support of the upper parliament and even if her campaign massaging lacks “teeth”. From today’s vantage point it appears less likely that the CDU can afford to keep its pro-business FDP coalition partners (unless a coalition agreement can be made along with the Greens) and more likely that the CDU returns to a “grand coalition” with the SPD. Although such a coalition arrangement could spell legislative friction, it would be advantageous versus the current gridlock of opposing coalitions across the upper and lower houses of parliament.

Matthew Hedrick

Senior Analyst