TODAY’S S&P 500 SET-UP – January 24, 2013

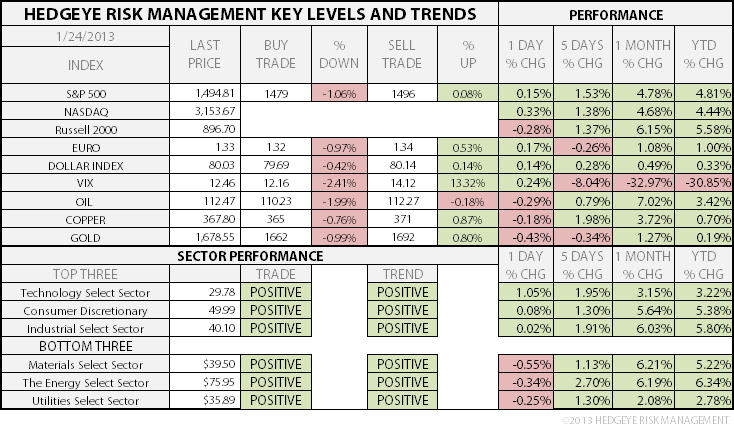

As we look at today's setup for the S&P 500, the range is 17 points or 1.06% downside to 1479 and 0.08% upside to 1496.

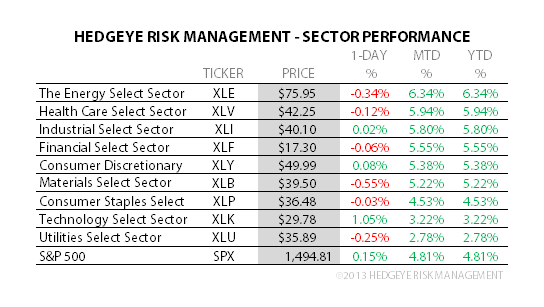

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.58 from 1.59

- VIX closed at 12.46 1 day percent change of 0.24%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Initial Jobless Claims, Jan. 19, est. 355k (prior 335k)

- 8:30am: Continuing Claims, Jan. 12, est. 3.2m (prior 3.214m)

- 8:58am: Markit US PMI, Jan. preliminary, est. 53 (prior 54)

- 9:45am: Bloomberg Consumer Comfort, Jan. 20 (prior -35.5)

- 10am: Leading Indicators, Dec., est. 0.4% (prior -0.2%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural gas storage change

- 11am: DOE inventories

- 11am: Kansas City Fed Manufacturing, Jan., est. 1 (prior -2)

- 11am: Fed to buy $2.75b-$3.5b debt in 2020-2022 sector

- 11am: U.S. Treasury to announce plans for sale of 2Y notes, 5Y notes, 7Y notes

- 1pm: U.S. Treasury to sell $15b 10Y TIPS

GOVERNMENT:

- Senate in session, House not in session

- Nom. hearing for Sen. John Kerry, D-Mass., as Sec of State

- Sen. Dianne Feinstein, D-Calif., to introduce gun legislation

- U.S., Japan to sign amendment to bilateral income tax treaty

- HHS, FDA meeting on public health benefits, risks of drugs containing hydrocodone, 8am

- HHS, NIH meeting on H1N1/bird flu transmission and data management, 9am

- Senate Health, Education, Labor and Pensions Cmte hearing on mental health system in America, 10am

WHAT TO WATCH

- Apple plunges after sales forecast trails est.

- Asian suppliers fall after Apple’s sales outlook

- Commerzbank plans to cut as many as 6,000 jobs worldwide, Barclays said to plan 15% job cuts at Asian investment bank

- Citigroup’s Corbat says pay environment to remain challenging

- World Economic Forum in Davos continues

- Delta Air Lines is talking to Airbus, Boeing on buying jets

- Euro-area composite PMI contracts at slower pace than est.

- Delphi considers ‘bolt-on’ acquisitions against paying dividend

- North Korea threatens to conduct nuclear test

- Three-month suspension of U.S. debt ceiling passed by House

- FDA approves Roche’s Avastin with chemo for colorectal cancer

EARNINGS:

- Cash America International (CSH) 6am, $1.20

- Keycorp (KEY) 6am, $0.21

- Stanley Black & Decker (SWK) 6am, $1.28

- Knight Capital (KCG) 6am, $0.03

- McCormick & Co (MKC) 6:30am, $1.14

- Southwest Airlines Co (LUV) 6:45am, $0.07

- Xerox (XRX) 6:51am, $0.29

- AO Smith (AOS) 7am, $0.81

- Colonial Properties Trust (CLP) 7am, $0.33

- Hubbell (HUB/B) 7am, $1.20

- International Speedway (ISCA) 7am, $0.56

- National Penn Bancshares (NPBC) 7am, $0.17

- Teledyne Technologies (TDY) 7am, $1.08

- AmerisourceBergen (ABC) 7am, $0.67

- Ametek (AME) 7am, $0.48

- Baxter International (BAX) 7am, $1.26 - Preview

- Celgene (CELG) 7am, $1.32

- Dover (DOV) 7am, $1.07

- EQT (EQT) 7am, $0.42

- Raytheon (RTN) 7am, $1.31

- EQT Midstream Partners (EQM) 7:05am, $0.40

- Brunswick (BC) 7:30am, $(0.08)

- Fairchild Semiconductor (FCS) 7:30am, $0.10

- 3M Co (MMM) 7:30am, $1.41 - Preview

- Timken Co (TKR) 7:30am, $0.62

- Airgas (ARG) 7:30am, $1.07

- Bristol-Myers Squibb Co (BMY) 7:30am, $0.42 - Preview

- Kennametal (KMT) 7:30am, $0.64

- Lockheed Martin (LMT) 7:30am, $1.82

- United Continental Holdings (UAL) 7:30am, $(0.61)

- Alaska Air Group (ALK) 8am, $0.71

- Avnet (AVT) 8am, $0.83

- Cypress Semiconductor (CY) 8am, $0.04

- Meredith (MDP) 8am, $0.87

- WW Grainger (GWW) 8am, $2.61

- Janus Capital Group (JNS) 8am, $0.14

- Precision Castparts (PCP) 8am, $2.47

- Rayonier (RYN) 8am, $0.57

- Union Pacific (UNP) 8am, $2.16

- Coherent (COHR) 8:02am, $0.72

- AVX (AVX) 8:30am, $0.15

- Deluxe (DLX) 8:30am, $0.88

- GATX (GMT) 8:30am, $0.54

- OSI Systems (OSIS) 8:30am, $0.68

- Old Republic International (ORI) 9am, $(0.05)

- Informatica (INFA) 4pm, $0.37

- Microsemi (MSCC) 4pm, $0.52

- AT&T (T) 4:02pm, $0.45

- Sterling Financial (STSA) 4pm, $0.52

- Cirrus Logic (CRUS) 4pm, $1.41

- JB Hunt (JBHT) 4pm, $0.70

- Maxim Integrated (MXIM) 4pm, $0.41

- Select Comfort (SCSS) 4:01pm, $0.32

- Federated Investors (FII) 4:01pm, $0.40

- Open Text (OTC CN) 4:01pm, $1.38

- Flextronics (FLEX) 4:01pm, $0.20

- Micros Systems (MCRS) 4:02pm, $0.58

- Covance (CVD) 4:02pm, $0.71

- Microsoft (MSFT) 4:02pm, $0.74

- Starbucks (SBUX) 4:03pm, $0.57

- VeriSign (VRSN) 4:04pm, $0.51

- Cepheid (CPHD) 4:05pm, $(0.01)

- E*Trade Financial (ETFC) 4:05pm, $(0.54)

- Juniper Networks (JNPR) 4:05pm, $0.22

- ResMed (RMD) 4:05pm, $0.52

- Tempur-Pedic International (TPX) 4:05pm, $0.55

- SVB Financial Group (SIVB) 4:14pm, $0.88

- City National (CYN) 4:15pm, $1.00

- Glacier Bancorp (GBCI) 4:15pm, $0.28

- Synaptics (SYNA) 4:15pm, $0.45

- KLA-Tencor (KLAC) 4:15pm, $0.56

- QLogic (QLGC) 4:15pm, $0.17

- Energen (EGN) 4:49pm, $0.74

- Hancock Holding (HBHC) 5pm, $0.63

- Iberiabank (IBKC) Late, $0.79

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – both Apple and Gold bulls will be as quiet as NFLX bears this morn; some serious pin action in names where consensus has very strong views; Our AAPL TAIL risk line of $561 remains intact (no position); Gold failed, fast, at $1692 TREND resistance yesterday, and Netflix, well, just look at it if you want to feel like it’s 1999.

- Gold Seen Extending Rally as Fed’s QE3 to Last Through 2014

- Sugar Rush Leaves U.S. With Biggest Glut in Decade: Commodities

- Copper Declines as Codelco Adds to Indications of Ample Supply

- Oil Trades Near One-Week Low on U.S. Supplies, Seaway Pipeline

- Gold Drops to One-Week Low as Growth Outlook Curbs Haven Demand

- Economist Gartman Sells Some WTI Oil and May Get Out Entirely

- Iron Ore Seen Falling in Second Quarter as China Restocking Ends

- Robusta Coffee Advances on Stockpiles, Vietnam Crop; Cocoa Gains

- Brazil Sugar at Ports Rises 23% as Ships Head to Algeria, India

- China Tracks Errol Flynn to Tasmania in Quest for Wind: Energy

- HSBC Cuts Gold Allocation on 3-Year and Six-Month View

- China Zinc Output May Peak in 2015 as Project Pipeline Thins

- Rubber May Extend Rally After Golden Cross: Technical Analysis

- Zinc Mine Supply Growth May Slow During Next Eight Years

CURRENCIES

EUROPEAN MARKETS

FRANCE – let’s not talk about Spain’s unemployment going up again (even though they make up the numbers, they still see unemployment rising to 26% in Q4 vs 25% prior); lets talk about the country everyone wants to be: France – French PMI for JAN gets spanked to 42.9 vs 44.6 in DEC (Services PMI down too, 43.6 vs 45.2 last mth), French #GrowthSlowing.

ASIAN MARKETS

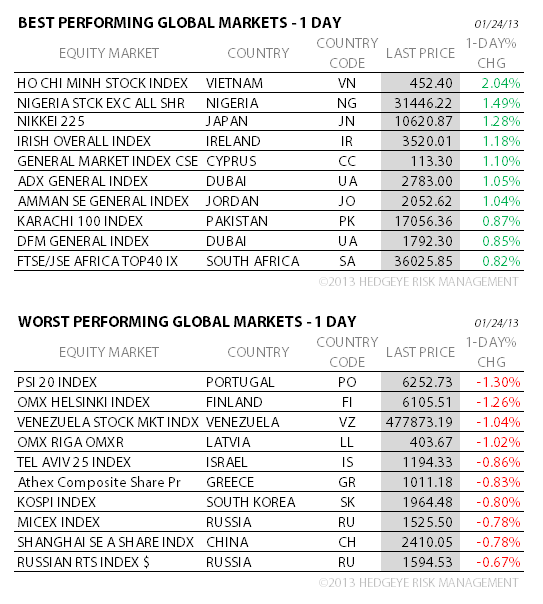

ASIA – KOSPI down another -0.8% after snapping its TRADE line of support 2-days ago, taking the correction to -3.3% from the JAN high; something to watch alongside the Hang Seng (2 days of lower-highs) and Shanghai Comp that was also -0.8% overnight and also broke its TRADE line of 2308 support into the close.

MIDDLE EAST

The Hedgeye Macro Team