As global macro data continues to confirm that growth is stabilizing, we’ve been discussing the possibility of seeing a 6-handle in the unemployment rate in 2013. With Bernanke offering an explicit employment target of 6.5% for a cessation in QE initiatives, a significant decline in unemployment over the NTM may augur higher yields as the bond market attempts to front-run a prospective Fed exit.

With market expectations for rates likely to follow the slope in unemployment rather than the actual realization of a 6.5% unemployment rate, we attempted to put some math around how the principal variables driving the Unemployment rate would have to trend for Unemployment to breach the 7% threshold over the next twelve months. Below we include a quick review of the variables driving the unemployment rate, the summary conclusions, and some other considerations as it relates to the go forward dynamics likely to directionally impact unemployment.

Of course, Bernanke could effectively hold the exit timeline hostage by again changing the rules mid-game and attaching conditions that a the sub-6.5% unemployment rate be accompanied by a “normalized Labor Force Participation Rate” or a “sustained, negligible output gap”. We’ve ignored this potentiality here as its largely unmodelable and because the bond market could well move ahead of the Federal Reserve realizing their growth forecast batting average isn’t going to improve from 0%.

Note that rather than attempting to provide an explicit year-end or 7% unemployment target date, the broader goal of this risk management exercise is to frame up the variable dynamics and quantify the magnitude of change in the relevant unemployment rate drivers necessary to take unemployment below 7.0% and towards 6.5% over the NTM. Certainly, any number of variable assumptions and scenario iterations can be contemplated. If you’d like to observe the impact of your own growth and participation rate assumptions on the unemployment rate timeline you can link to the associated model here >> Unemployment Rate Variable Analysis_HEDGEYE

UNEMPLOYMENT 101 - THE VARIABLES: Below is a summary review of the variables that drive the unemployment rate. Here, we’ve broken them down into the Input and the Dependent variables based on how we model them.

Independent/Input Variable Description:

- Civilian Non-institutional Population Growth (CNP): The CNP represents persons 16 years of age and older residing in the 50 States and the District of Columbia who are not inmates of institutions, such as penal and mental facilities, and homes for the aged, and who are not on active duty in the Armed Forces.

- Employment Growth: Growth in Employed workers as measured by the BLS Household (CPS) Survey.

- Labor Force Participation Rate (LFPR): Represents the Civilian labor Force as a percentage of the Civilian Non-institutional Population. Equal to the sum of employed & unemployed workers.

Dependent Variables:

4. Total Labor Force: The Civilian Labor force is a product of the Civilian Non-institutional Population & the labor force participation rate

5. Unemployed Workers: The total number of unemployed workers is the difference between the Labor Force and total employed workers.

Unemployment Rate = the number of unemployed workers as a % of the Total Labor Force (i.e. the sum of employed and unemployed workers)

So, assumptions need to be made for the growth in the Civilian Non-institutional Population (CNP), growth in the number of Employed Workers and the Labor Force Participation Rate (LFPR). The Total Labor Force and the Total Number of Unemployed become a function of the three input variables and the direction in the unemployment rate is determined by the participation rate and the delta between CNP growth and growth in the employed.

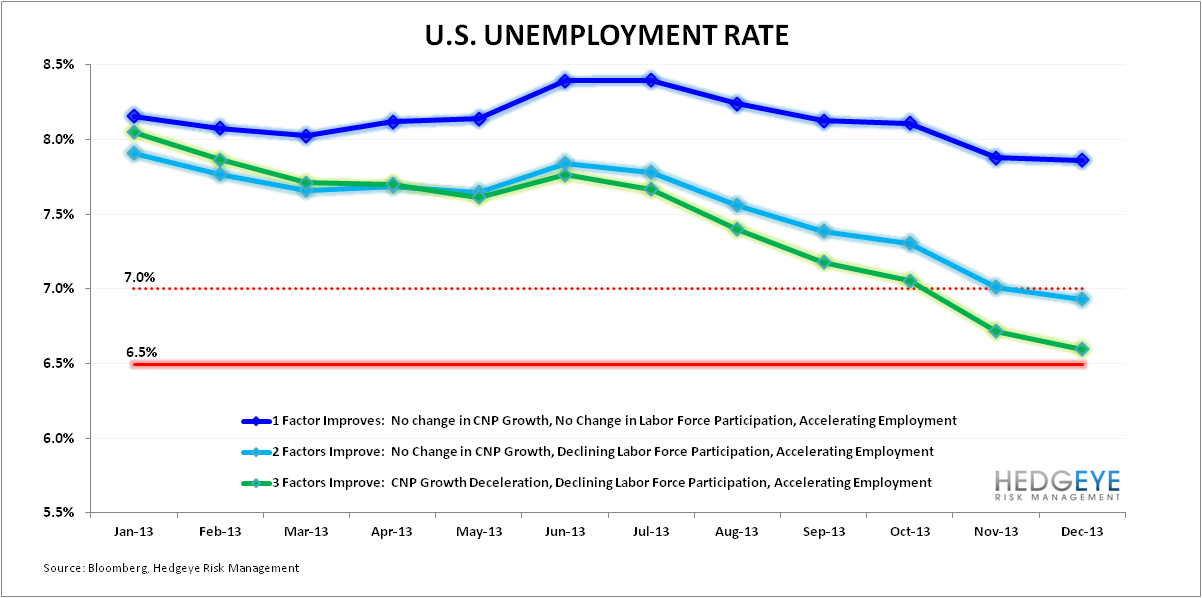

The CONCLUSION: Can we get 2 out of 3?

In the chart below we provide a timeline view of the 2013 Unemployment Rate under a selection of scenarios. Obviously, any number of iterations can be envisaged with respect to growth rates and interaction between the principle drivers of the unemployment rate but, in general, 2 of the 3 variables need to trend positively with respect to the unemployment rate for a move to 7% and below to be a 2013 event.

It’s notable that the NTM moves don’t have to be extraordinary for this to occur. For example, scenarios in which Employment growth accelerates 30bps (2Y basis) on average in 2013 and CNP growth declines linearly to the historical average over the NTM or the Labor Force Participation rate continues to decline at the 3Y CAGR both result in a move to/below the 7% unemployment level in 4Q13.

If, however, positive acceleration occurs in just a single variable while the other two flat-line or trend negatively, the timeline for <7.0% unemployment extends significantly. For example, if employment accelerates 50bps (2Y basis) on average in 2013 while Labor force participation remains static at the current level and CNP growth holds at the current rate, the implied unemployment rate would reach a 2013 low of 7.3% in December.

In terms of thinking about the directional trend in the relevant variables – with housing continuing to accelerate, the domestic jobs data continuing to trend positively and our #growthstabilzing theme extending itself, we could make a credible case for seeing a modest acceleration in employment growth. Given that growth in the civilian non-institutional population generally tracks population growth in the 16YOA+ cohort over the longer term and that volatility in active duty military status should be more subdued going forward, the assumption that CNP growth decelerates towards population growth probably represents the baseline case.

The Labor Force participation rate, and the structural and behavorial psychology dynamics underpinning it, remains the largest wildcard. The consensus logic goes that in a typical recovery, economic growth and employment growth drive renewed worker interest in employment in a reflexive fashion. Discouraged workers, who are not currently seeking employment and are not included in the Labor force totals, again begin to actively seek employment. To the extent that growth in workers coming back to actively look for work outpaces actual employment gains, the unemployment rate is negatively impacted despite the improved economic conditions/outlook. Here, the transient increase in the unemployment rate would belie a positive economic inflection.

The current situation is complicated by the fact that despite the ongoing, albeit tepid employment recovery, the resurgence in job seeking, which typifies the back end of business cycle slowdowns, has yet to materialize and the LFPR continues to slide. Whether this behavioral dynamic continues and to the extent that structural unemployment/length of unemployment is a contributing factor remains an unknown. Also unknown is the extent to which protracted fiscal policy uncertainty (Health Law, Fiscal Cliff, Budget Control Act/Sequestration, etc) has dragged on employer hiring decisions. Regardless of the outstanding questions, labor force participation will continue as the real wild-card variable to watch relative to its impact on the unemployment rate.

Other Considerations:

- Annual Benchmark Revision: the Census Bureau applies an annual population control adjustment to the Civilian Non-institutional Population alongside the January release every year. Historically, the magnitude of the January adjustment has ranged from tens to hundreds of thousands or even millions of individuals. An outsized revision to the January 2013 data could shift the unemployment variable dynamics from their current trend.

- Employment – Growth Connection: The historical frequency distribution for Employment and growth suggests we’d need to see #growthstabilizing transition to growth accelerating for a concurrent acceleration in employment to manifest. While employment growth could run ahead of economic growth at the onset of a recovery, historically, employment growth >2% is typically associated with real GDP growth north of 3%. We show the historical relationship between real GDP Growth and y/y employment growth as measured by the BLS’s Household Survey below.

- Energy/Commodity Inflation: In our 1Q13 themes call we highlighted the top 3 risks to #growthstabilizing as 1. Rising Oil Prices 2. Japan & 3. Earnings Slowing. As it relates to risk #1 - as of this morning, both Brent and WTIC have re-captured their respective long-term TAIL risk lines of $92.04 and $111.48 support. A continued reflation in oil and commodity prices broadly represents a real time tax on consumers, an input cost related margin drag on business, and a material headwind to growth accelerating from here.

Christian B. Drake

Senior Analyst