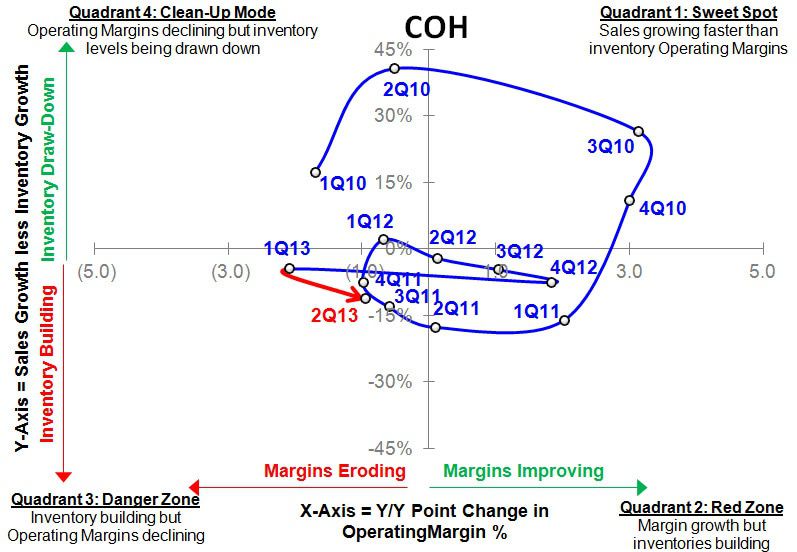

- Coach is hardly flying in on the wings of glory with its 2Q13 results and a $1.23 print versus consensus of $1.29. No surprises here, as this is in-line with our model, and has been on our short list for a while given our concerns over the levels of spending needed to maintain market share. But the question to ask here is whether this miss is an event to buy into, or one to press. Our sense is that it is the latter.

- Our rationale is that we’re hearing Coach talk about the promotional cadence and competitive landscape for the first time in – well, ever. Ever is a long time. We get it that China and Men both represent sizable opportunities, but the US Handbag market is one that represents 70% of Coach’s business. If it can’t grow profitably, then nor can Coach.

- The reality is that when we see a miss like this – for the reasons we’re seeing – it is usually not the last miss. We think that it’s more likely than not that COH is locked in a multi-year period where it grows its top line at the expense of a draw-down in EBIT margin, or it holds margins steady with top line remaining stagnant. We’d bet on the former.

- Either way, it suggests that FY13 is not the last ‘investment year’ that Coach will see. We think that value investors risk getting stuck in a value trap on this one. This name is cheap, built to stay that way, and lacking earnings growth to move the stock higher.