McDonald’s is set to report December sales, along with 1Q earnings, tomorrow before the market open.

General View

Recently, we’ve been vocal on our view that McDonald’s earnings are likely to disappoint in 2013. We are continuing to advise clients to be patient on the long side of MCD until expectations for next year come down. We believe that, aside from the macro environment and lapping difficult partially-weather-driven comps, self-inflicted wounds, that management has not yet owned up to, are also likely to impede earnings growth over the next twelve months.

Sales Preview

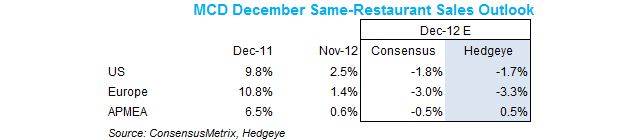

McDonald’s reports December sales, along with 1Q earnings, tomorrow before the market open. Consensus is anticipating a sequential deceleration in two-year average trends for global trends.

Below, we go through what we would view as good, bad, or neutral comparable restaurant sales numbers for McDonald’s three regions in December. For comparison purposes, we have adjusted for historical calendar and trading day impacts (but not weather).

Compared to December 2011, December 2012 had one additional Monday, one additional Sunday, one less Thursday, and one less Friday. In 2012, Christmas fell on a Tuesday versus Sunday in 2011. We expect a modestly positive impact on the headline numbers for December.

United States – facing a compare of 9.8%, including a calendar shift of roughly 0.7%, varying by area of the world:

GOOD: A print higher than -1% would be received as a positive result as it would imply, on a calendar-adjusted basis, an acceleration in two-year average trends versus November’s strong result. November’s same-restaurant sales growth overstated true trends in the US, to a degree, as a sizeable calendar shift boosted the headline numbers. A heavy focus on the Dollar Menu also aided results in November. The question for December will be how much of an impact the McRib will have had. Our expectation is for a print of -1.7%.

NEUTRAL: A result between -1% and -2% would imply calendar-adjusted two-year average trends roughly flat versus November. Decelerating trends would arguably lend credence to our contention that self-inflicted wounds, and not only macro, have been impacting MCD sales in recent quarters.

BAD: Same-restaurant sales growth less than -2% would imply a sequential deceleration in two-year average trends in the United States. We would expect the stock to react negatively to such a result.

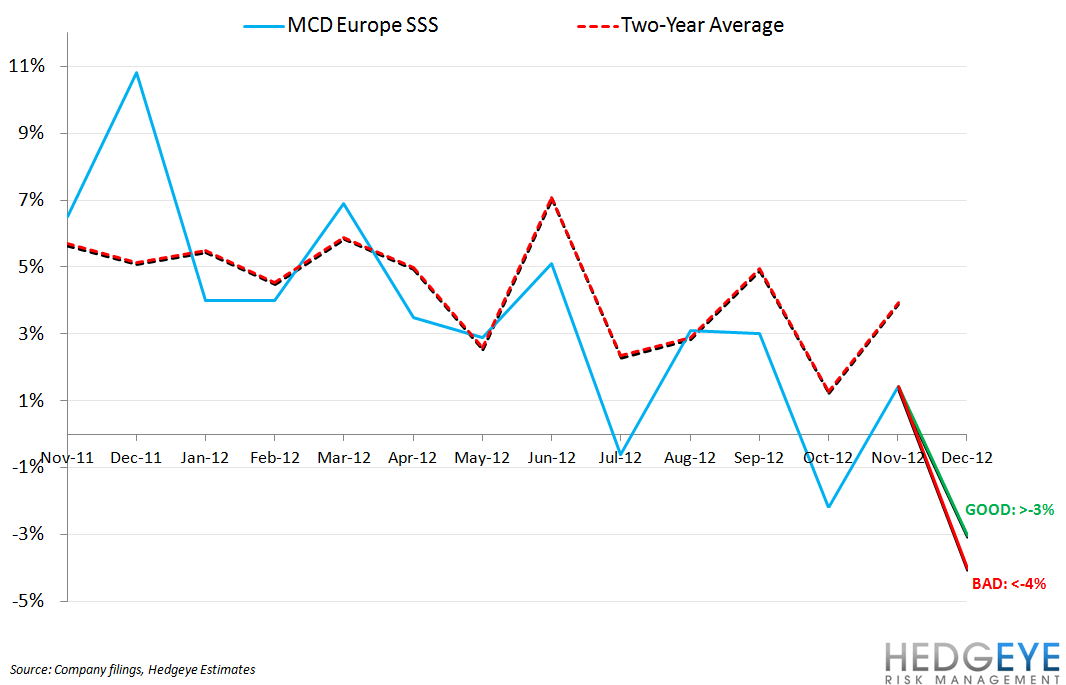

Europe – facing a compare of 10.8%, including a calendar shift of roughly 0.7%, varying by area of the world:

GOOD: Better than -3% would be viewed as a stronger-than-expected result. On a calendar-adjusted basis, such a result would imply a sequential acceleration in two-year average trends. Soft economic conditions persisted in Europe during November with Germany one of the underperforming markets. We would note the sequentially improving “Zew Germany Expectations of Economic Growth” index as being a positive sign for MCD Europe in December, but we continue to expect sluggish trends across the pond. Our expectation is for a print of -3.3%.

NEUTRAL: A print between -3% and -4% would be received as neutral as it would imply calendar-adjusted two year average trends roughly flat versus November.

BAD: Weaker-than- -4% same-restaurant sales growth would imply, on a calendar-adjusted basis, two-year average trends in line with the weakest months of 2012: February and August.

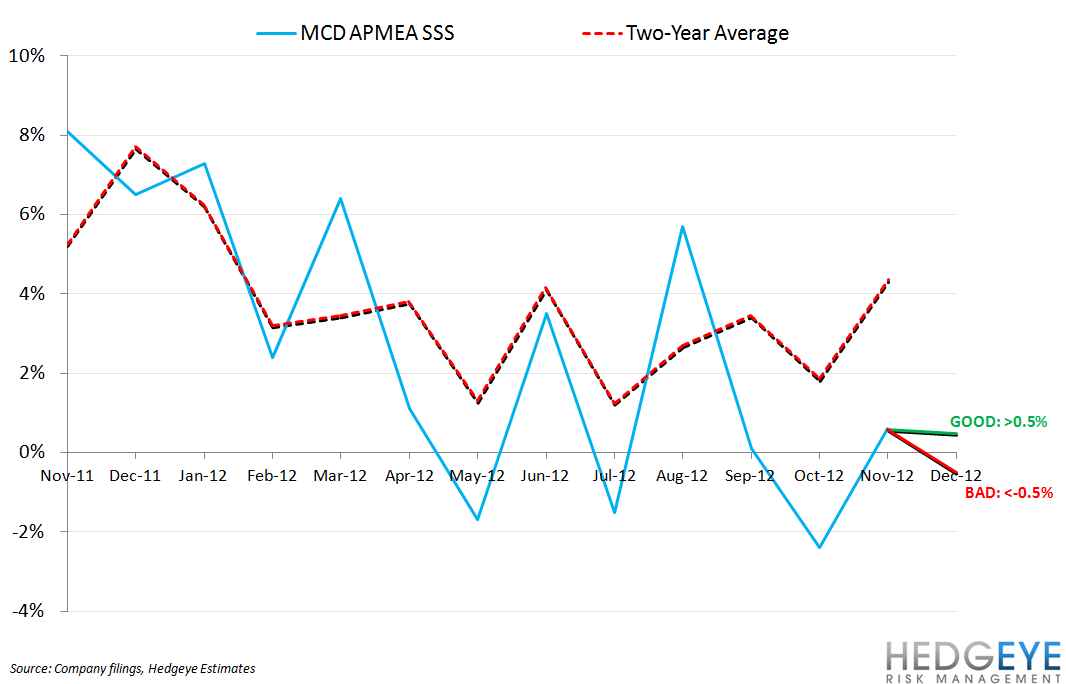

APMEA – facing a compare of 6.5%, including a calendar shift of roughly 0.7%, varying by area of the world:

GOOD: A print of better than 0.5% would be a positive result for MCD APMEA. Weakness in Japan is ongoing and we are not expecting much from this division in December as the fallout continues around the KFC Chicken scandal. While MCD is a competitor of KFC’s, we feel that some impact may follow through to other western chains. Our expectation is for a print of 0.5%.

NEUTRAL: A print between -0.5% and 0.5% would be received as neutral by investors as it would imply calendar-adjusted two year average trends roughly flat versus November.

BAD: Same-restaurant sales growth slower than -0.5% in December would imply sequential deceleration in two-year average trends.

Howard Penney

Managing Director

Rory Green

Senior Analyst