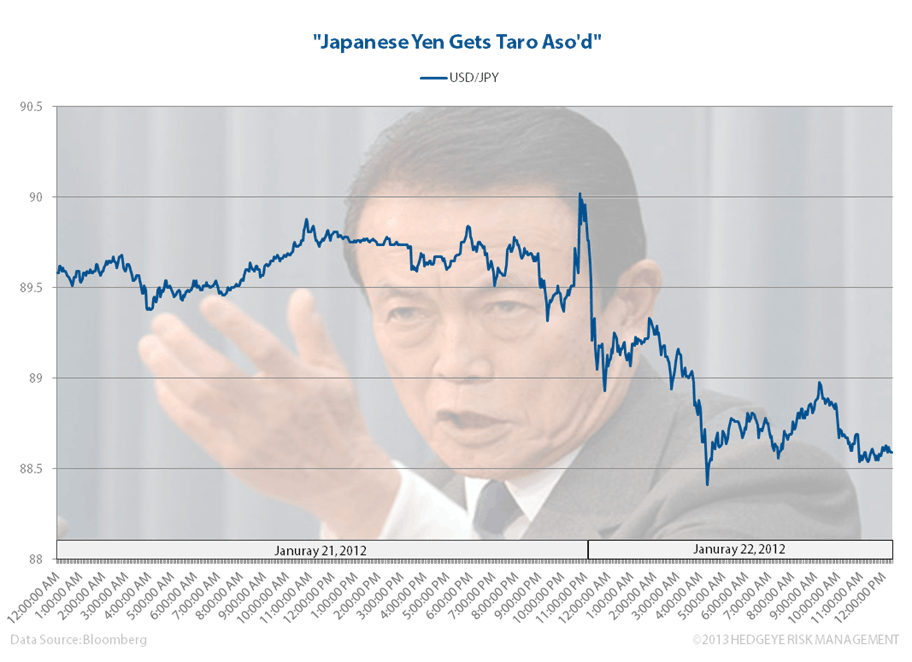

Early this morning, the Bank of Japan announced it would enter into an "open ended" asset purchase program and would "firmly" target 2% inflation. As a result, the Japanese Yen spiked over 1% on the news, much to the chagrin of those who were short the currency. Japan's Finance Minister Taro Aso and Prime Minister Shinzo Abe are determined to fight deflation, calling the move ""...a bold review of monetary policy, an epoch-making document." Timing is everything in this market. Our Global Macro Theme of #QuadrillYen rings truer than ever today.