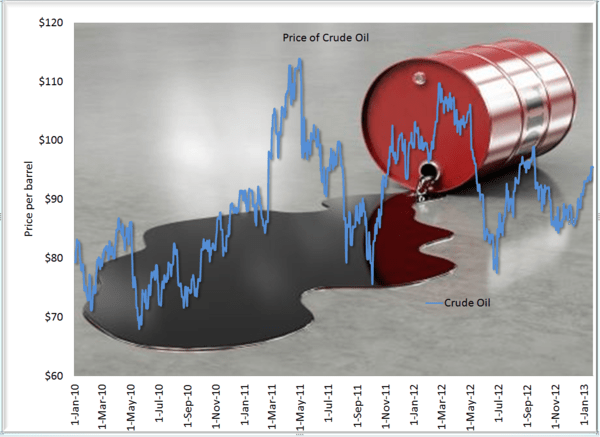

Kimberly-Clark (KMB) is reporting Q4 2012 earnings on January 25 along with Procter & Gamble (PG). We think there’s an interesting setup here for a long PG/short KMB trade. Commodity prices including oil and pulp have moved against the company over the last quarter of 2012, which will put the squeeze on earnings along with strategic marketing expenditures.

As for PG, we estimate Q2 EPS of $1.13 versus a guidance range of $1.07 to $1.13. In our experience, we see PG beating estimates and raising guidance, which will drive the stock higher.