TODAY’S S&P 500 SET-UP – January 22, 2013

As we look at today's setup for the S&P 500, the range is 18 points or 1.01% downside to 1471 and 0.20% upside to 1489.

SECTOR AND GLOBAL PERFORMANCE

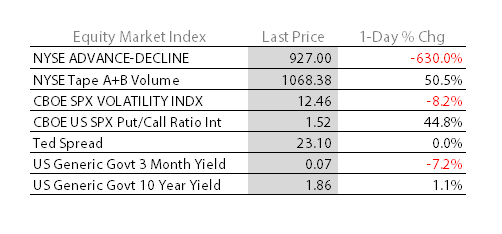

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.61 from 1.59

- VIX closed at 13.42 1 day percent change of -0.96%

- AAPL – “Most Read” article on Bloomberg this morn = “Apple May Face 1st Profit Drop in Decade As iPhone Slows”… so, ahead of AAPL earnings (tomorrow), it’s getting real newsy (UBS cutting price target this morn too) – but the stock isn’t raging oversold on my signal yet (it would be at $482). AAPL’s TAIL risk resistance line = $561.

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed Nat Activity Index, Dec. (prior 0.1)

- 10am: Richmond Fed Manufacturing Index, Jan. (prior 5)

- 10am: Existing Home Sales, Dec., est. 5.10m (prior 5.04m)

- 10am: Existing Home Sales M/m, Dec., est. 1.2% (prior 5.9%)

- 11am: Fed to buy $1b-$1.5b TIPS in 2017-2042 sector

- 11:30am: U.S. Treasury to sell $32b 3-mo notes, $28b 6-mo notes

GOVERNMENT:

- Obama seeks optimism renewal in 2nd inaugural ceremony

- House, Senate meet at 10am

- House Ways and Means holds hearing on debt limit

- Senate debate, vote expected on Hurricane Sandy relief

- Pfizer CEO Ian Read to testify in U.S. District court in jury trial on claim Chantix causes psychiatric disorders

WHAT TO WATCH

- Dell said to hire Evercore to seek higher bids after buyout

- Obama seeks optimism renewal at 2nd inauguration ceremony

- BOJ sets 2% inflation target without adding stimulus in 2013

- Greece’s new loan payment is cleared by euro area

- Eurogroup picks Dutchman Dijsselbloem to succeed Juncker

- Euro area grapples with ESM bank aid rules; set to approve design of financial-transaction tax

- Atari U.S. units file for bankruptcy to break from parent

- Alstom 3Q orders rise 3%, led by demand for trains

- German ZEW investor confidence rises to highest in 2 1/2 yrs

- SABMiller lager volume rises less than analyst ests

- EADS CEO says to meet, beat earnings, sales goals at units

- Israelis vote with Netanyahu probably heading for 3rd term

EARNINGS:

- Dupont (DD) 6am, $0.07

- Verizon (VZ) 6:30am, $0.50 - Preview

- II-VI (IIVI) 6:55am, $0.21

- Regions Financial (RF) 7am, $0.21

- Synovus Financial (SNV) 7am, $(0.11)

- Travelers (TRV) 7am, $0.14

- Waters (WAT) 7am, $1.59

- TD Ameritrade Holding (AMTD) 7:30am, $0.24

- Delta Air Lines (DAL) 7:30am, $0.28

- FirstMerit (FMER) 7:30am, $0.33

- PrivateBancorp (PVTB) 7:30am, $0.26

- Brinker International (EAT) 7:45am, $0.50

- Johnson & Johnson (JNJ) 7:45am, $1.17 - Preview

- Freeport-McMoRan (FCX) 8am, $0.72 - Preview

- Kansas City Southern (KSU) 8:01am, $0.82

- Canadian National Railway (CNR CN) 9am, C$1.41

- Celestica (CLS CN) 4pm, $0.19

- Cree (CREE) 4pm, $0.30

- RF Micro Devices (RFMD) 4pm, $0.06

- Total System Services (TSS) 4pm, $0.33

- Woodward (WWD) 4pm, $0.46

- CSX (CSX) 4:01pm, $0.39

- Google (GOOG) 4:01pm, $10.55

- Ezcorp (EZPW) 4:01pm, $0.58

- Albemarle (ALB) 4:03pm, $0.99

- IBM (IBM) 4:03pm, $5.25

- CA (CA) 4:05pm, $0.61

- Intuitive Surgical (ISRG) 4:05pm, $4.04

- Norfolk Southern (NSC) 4:05pm, $1.19

- Compuware (CPWR) 4:13pm, $0.10

- Advanced Micro Devices (AMD) 4:15pm, $(0.18)

- International Game Technology (IGT) 4:15pm, $0.24

- Trustmark (TRMK) 4:30pm, $0.44

- Texas Instruments (TXN) 4:30pm, $0.07

- Community Bank System (CBU) 4:30pm, $0.54

- UMB Financial (UMBF) 4:30pm, $0.67

- Packaging of America (PKG) 5pm, $0.62

- Rock Tenn (RKT) Post-Mkt, $1.27

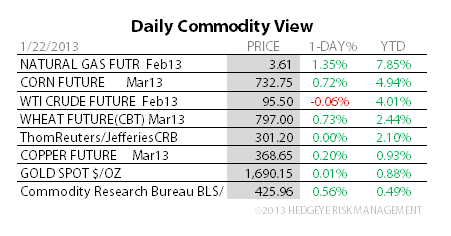

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Commodities Climb to Three-Month High After Japan’s Policy Shift

- Palm Favored by Ospraie Rising as Reserves Retreat: Commodities

- Gold Trades Near One-Month High as BOJ Announces Stimulus Plan

- Copper Reaches One-Week High as Bank of Japan Signals Stimulus

- Brent Oil Rises to One-Week High as Japan Pledges More Stimulus

- Sugar Drops to 2 1/2-Year Low as Stockpiling May End; Cocoa Down

- Freeport Earnings Beat Estimates on Higher-Than-Expected Sales

- EDF Investors at Risk of Losing Record Dividend on Costs: Energy

- Iron-Ore Port Braces for Australian Storm as Apache Shuts Fields

- Inmet Is in Confidentiality Pacts, Talks With Number of Parties

- SovEcon Sees Weather Risks for Winter Crops in Southern Russia

- Worst European Coal Slump in Five Years Not Over: Energy Markets

- Billionaire Fredriksen Winning as LNG Tanker Rates Drop: Freight

- Wheat Climbs to One-Month High as Winter Threatens Russian Crop

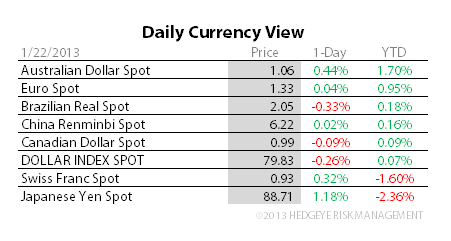

CURRENCIES

EUROPEAN MARKETS

GERMANY – despite the best ZEW print since May of 2010 (31.5 JAN vs 6.9 DEC), the DAX remains under corrective selling pressure this morn after failing to make higher-highs. Was that the ‘as good as it gets’ print for European high freq data? Maybe.

ASIAN MARKETS

JAPAN – Abe called the BOJ’s inflation targeting “epoch making”, and while I am not sure what that’s supposed to mean, the market bought/covered Yen, big time, +1% vs USD on the “news” – Nikkei stopped going up on that and actually broke immediate-term TRADE support (10,733) for the 1st time in mths; Big Government Intervention = amplified market volatility.

MIDDLE EAST

The Hedgeye Macro Team