We are looking into a new format for the Weekly Hot Ideas product and are sharing this with you in order to collect feedback from you. The goal was to simplify the layout and more clearly communicate the action along with the potential upside.

Please send your thoughts to feedback@hedgeye.com

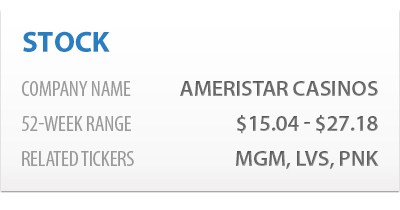

We believe there is a high likelihood that PNK's 26.50 bid for ASCA will be topped. As evidenced by the huge increase in PNK's stock, ASCA left a lot on the table. MGM Resorts International or Penn Resorts could offer a higher bid for ASCA. ASCA would be hugely accretive for MGM, given MGM's large balance of tax loss carry-forwards. They could pay 8.5x ASCA's trailing 12-month EBITDA, which would equate to a $35 bid and still make it de-leveraging and very accretive from an EPS and cash flow perspective. PENN could offer even higher since ASCA's integration with its planned REIT structure would instantly create value. We believe ASCA could be worth up to $40 to PENN.

INTERMEDIATE TERM (the next 3 months or more)

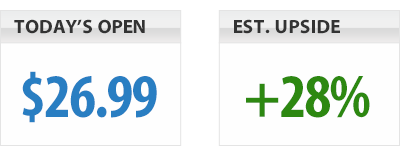

The stock may trade in a tight range for the next month or so. Investors are waiting to see if a higher bid from MGM, PENN, or another operator surfaces. Fundamentally, ASCA remains relatively protected from new competition and, with the top in class assets in virtually all of its jurisdictions, is a defensive play in the space. LONG-TERM (the next 3 years or less) PNK's acquisition of ASCA is expected to close by 3Q 2013. However, we believe ASCA will receive a higher bid before that deadline. A bid of at least $35 (28% premium to current price) seems reasonable and doable given the relatively small breakup fee.

LONG-TERM (the next 3 years or less)

PNK's acquisition of ASCA is expected to close by 3Q 2013. However, we believe ASCA will receive a higher bid before that deadline. A bid of at least $35 (28% premium to current price) seems reasonable and doable given the relatively small breakup fee.

© 2013 Hedgeye Risk Management, LLC. The information contained herein is the property of Hedgeye, which reserves all rights thereto. It is intended for the sole use of Hedgeye and its Subscribers, and redistribution of any part of this information is prohibited without the express written consent of Hedgeye. This is presented for information purposes only and does not constitute an offer to sell, or a solicitation of an offer to buy any security. This information is presented without regard to individual investment objectives, risk parameters or suitability. This information is from sources believed to be reliable; Hedgeye is not responsible for errors, inaccuracies or omissions with regard to this information, or for any consequences that may arise from use of this information. For full Terms of Use of this information, please go to www.hedgeye.com