This Is Why Cap One Trades at a Discount to Discover

Capital One reported disappointing 4Q12 results that were made worse by issuing 2013 guidance well below expectations. Looking ahead the company said to expect $22.5 billion in 2013 revenue vs. expectations for $23.0 billion. Meanwhile, they said to expect opex of $12.4 billion vs expectations for $12.0 billion. Finally, they dumped a bucket of cold water on capital return expectations when they said they were only requesting an increased dividend through CCAR (no buyback).

The weakness this quarter stemmed principally from a sharp sequential decline in revenue margins attributable to significant revenue suppression. Revenue suppression is sneaky and obviously caught the market flat-footed, not understanding that prior to 4Q it was artificially propping revenue up by benefiting from the SOP 03-3 credit mark on acquired loans. In management's defense, they had indicated last quarter that margins would come down through the first half of 2013 by 35 bps, but clearly that was overly optimistic as margins dropped by 45 bps in one quarter. Moreover, the Street had been steadily conditioned to ignore these warnings as management had been making similar negative margin commentary, off and on, for the last several quarters only to then show stable to rising margins.

Set A Calendar Reminder for 350 Days From Now to Sell Ahead of 4Q13

Capital One seems to have an uncanny knack for disappointing investors with their fourth quarter results. Looking back over the last several years, the stock has had, on average, a -3.5% drop following the 4Q print (closer to -8% if you include 4Q08), a +6.0% rise following the 3Q print and a roughly flat response to the 1Q and 2Q prints. We show this in the first chart below. Interestingly, in the second chart below, we profile the stock following the last three 4Q reports. In all three instances, the stock was under pressure for a few additional days following it's first post-print tick, but then went on to recover, on average, all its losses by 20 days out. We think that poses an interesting opportunity for those thinking about the short-term outlook.

Fundamentally, We Think Estimates May Still Be Too High

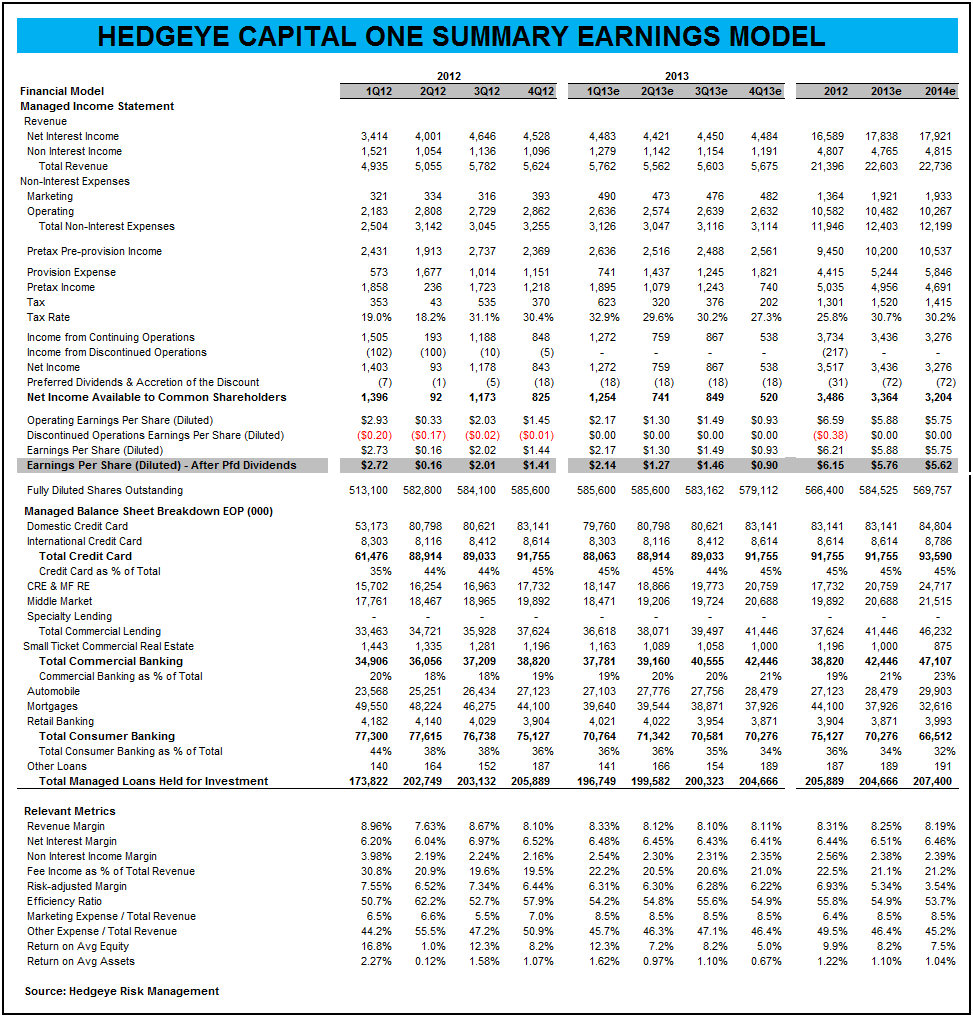

Fundamentally, post the quarter and the new guidance, we're still shaking out below Street numbers. We are now at $5.76 and $5.56 for 2013 and 2014. Prior to this evening, the Street was at $7.00 and $7.31. If we tax effect the $900mn guidance reduction ($500mn revenue cut and $400mn expense boost vs consensus) and divide by a flat YoY sharecount of 585mn, it lowers guidance by $1.08. That should take numbers down to $5.92 and $6.23, but our numbers are still coming in light of that, particularly in 2014. It's also interesting that guidance came down by 15%, effectively, and the stock is off 7% in the after-market. We wouldn't be surprised to see some selling follow-through in the days ahead. Our model is below for reference.

Joshua Steiner, CFA