Keith added EAT to the long side of our Real Time Alerts this morning at $32.42. Brinker is our favorite casual dining name and, despite the many headwinds facing the group, we believe that Chili’s will continue to take share versus its competitors.

We expect Chili’s to produce 2QFY13 same-restaurant sales in the region of 2%. Kitchen enhancements and remodels at Chili’s continue to aid top-line momentum and lead, in our view, to an upside surprise versus the consensus estimate of 1.5% SRS. It will be important for results to continue to demonstrate continuing progress on the restaurant operating margin line as the benefits of the remodel program continue to flow through.

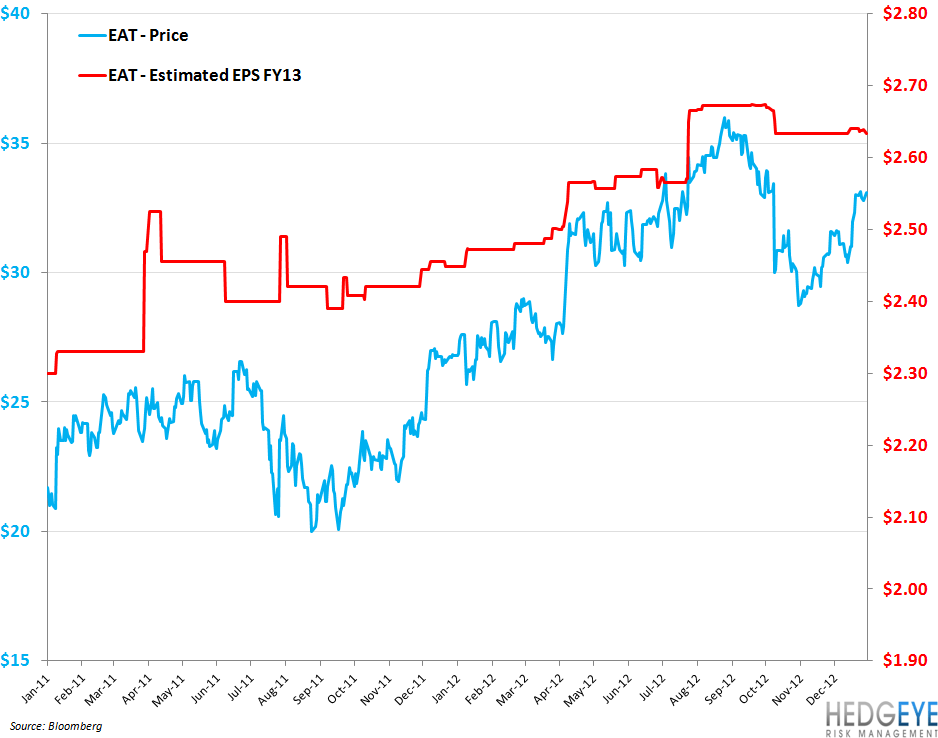

At 7.5x EV/EBITDA, the stock is being valued below the average casual dining stock at 7.7x. As well as the attractive multiple, we believe that there is modest upside to the Street’s EPS estimate, which is currently at $2.32, to $2.38-2.40.

Brinker’s shares represent the best way to play casual dining on the long side, in our view, particularly if macroeconomic growth continues to stabilize. However, competitive dynamics, including the impact of Darden’s explicit desire to sacrifice margin to gain traffic should not be ignored. It's difficult to know how great an impact Darden's "price war" will have on Chili's - particularly Chili's newly remodeled stores - but given the recent declaration from Orlando, we would advise close monitoring of long positions in any casual dining shares.

Quantitative View

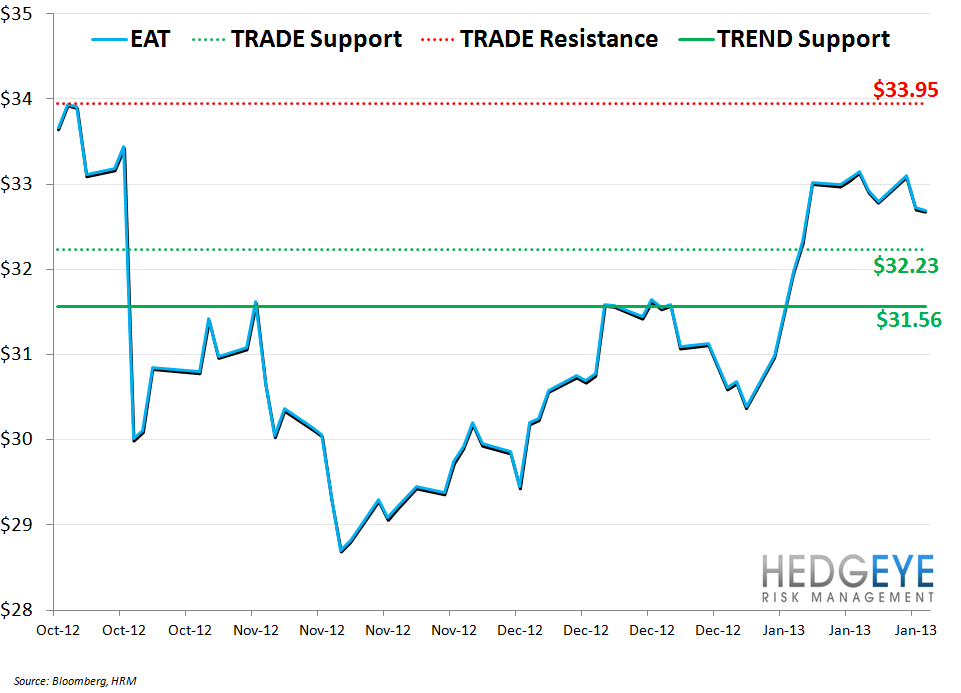

Our Macro Team’s quantitative view of the stock is that near-term TRADE resistance and support lie at $33.95 and $32.23, respectively. Intermediate-term TREND support is at $31.56.

Howard Penney

Managing Director

Rory Green

Senior Analyst