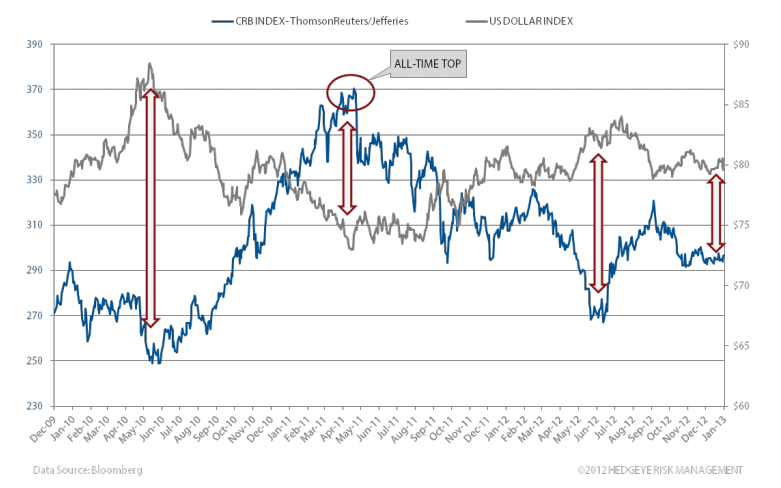

The continued burn-off in USD-Equity correlations we saw yesterday with Dollar Up, Stocks Up, & Oil Down remains the bullish factor cocktail we’d like to see persist for us to successfully bridge the inflection gap between #growthstabilzing & real growth accelerating.

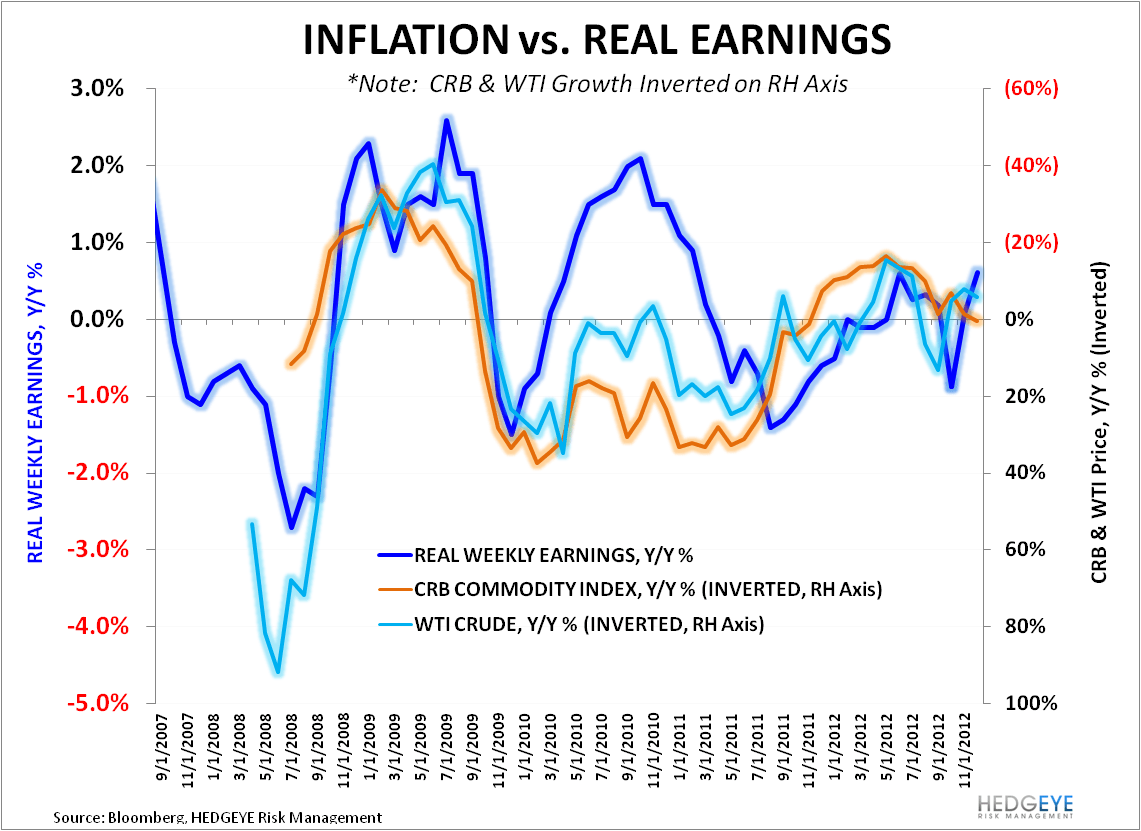

The inverse relationship between USD appreciation and energy and commodity deflation remains pronounced across durations. Similarly, the inverse relationship between real earnings growth & commodity inflation over the last 5 years has been distinct – in addition to inflations’ direct drag on the calculation of real earnings growth, it’s likely that as input costs rise and/or real consumption growth slows, employer’s look towards managing the SWB line as a margin supportive offset.

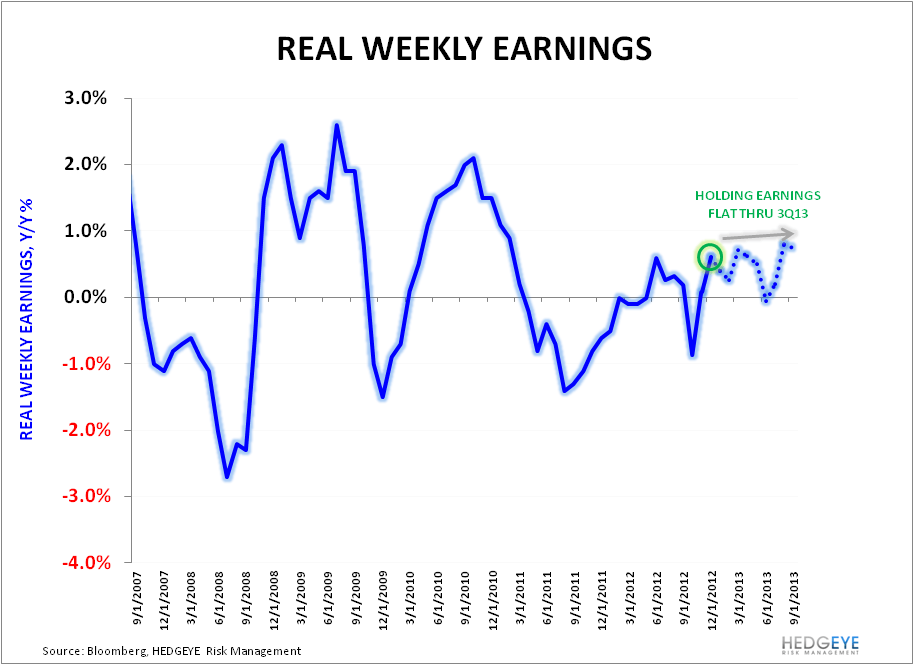

Below we show the trend in Real Earnings Growth (updated for this morning’s release) along with a long duration view of the relationship between Commodities Price Growth, the US Dollar, and Real Earnings Growth (note that commodity prices are inverted in the charts). The takeaway from the chart series below is really very simple with the data implying:

USD Higher --> Energy/Commodities lower --> Real Earnings/Real Growth Higher

As simplistic as this Dollar based flow model is, it remains the outstanding, untried policy transmission mechanism most capable of catalyzing sustainable real growth both domestically & globally, in our view.

The Real Earnings update for December showed Real Weekly Earnings growth accelerating to +0.6% - a new multi-year high and an obvious positive in the wake of the elimination of the 2% payroll tax holiday to start calendar 2013. The USD remains bullish on TRADE & TAIL durations and, alongside an easy comp setup through mid-year, should support further positive growth in real earnings should the USD bid continue.

Will legislators & policy makers make a genuine go at sustainable fiscal consolidation domestically, or even just stay out of the way? Will the phase transition in Japanese monetary policy promised by Taro Aso et al. continue to provide a relative bid to the dollar? We don’t know either - but so long as prices continue to confirm and the Dollar Up, Stocks Up dynamic can perpetuate itself, the immediate term game plan on the equities side remains to buy the Dips.

Christian B. Drake

Senior Analyst