TODAY’S S&P 500 SET-UP – January 16, 2013

As we look at today's setup for the S&P 500, the range is 12 points or 0.50% downside to 1465 and 0.32% upside to 1477.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

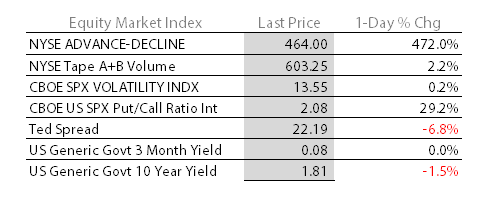

- YIELD CURVE: 1.56 from 1.49

- VIX closed at 13.55 1 day percent change of 0.22%

- BONDS – the 10yr UST yield is bullish TRADE/TREND (1.71-1.81% support) and bearish TAIL (1.84% resistance) right now, which is perfectly confusing the market, as it should – any time we start to whip above/below the big duration lines, people get confused. We say you stay w/ the TREND = buy stocks on red, short t-bonds on green.

MACRO DATA POINTS (Bloomberg Estimates):

- 7:00am: MBA Mortgage Applications, Jan. 11 (prior 11.7%)

- 8:30am: CPI, M/m, Dec., est. 0.0% (prior -0.3%)

- 8:30am: CPI Ex Food/Energy, M/m, Dec., est. 0.2%

- 9am: Net TIC Flows, Nov. (prior -$56.7b)

- 9am: Net L-T TIC Flows, Nov., est. $25.3b (prior $1.3b)

- 9:15am: Industrial Production, Dec., est. 0.3% (prior 1.1%)

- 9:15am: Capacity Utilization, Dec., est. 78.5% (prior 78.4%)

- 10am: NAHB Housing Market Index, Jan., est. 48 (prior 47)

- 10am: Fed’s Kocherlakota speaks in Eden Prairie, Minn.

- 10:30am: DoE inventories

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2042 sector

- 2pm: Fed issues Beige Book business survey

- 7pm: Fed’s Fisher speaks in Washington

- 8pm: Fed’s Kocherlakota speaks in Minneapolis on policy

GOVERNMENT:

- Senate not in session, House in session

- SEC Commissioner Dan Gallagher gives 2013 outlook for agency

- President Obama to unveil proposals to curb gun violence

WHAT TO WATCH

- All Nippon Airways, Japan Airlines grounded entire fleet of Boeing Dreamliners; will cancel all Dreamliner ops tomorrow

- India regulator to check 6 Dreamliners in Air India’s fleet

- World Bank cuts 2013 global growth forecast to 2.4%

- AB InBev said in talks w/ U.S. on concessions for Modelo

- Ford CFO forecasts greater than $1.5b European loss in 2013

- Alibaba said to hire Credit Suisse, Goldman for $3b-$4b IPO

- Apple introduced installment payment plans in China

- Temasek, CPPIB may invest in Dell alongside Silver Lake: FT

- Temasek spokesman declines to comment on report

- TUI Travel in talks with Airbus, Boeing on potential $6b plane order: Reuters

- European Dec. car sales fell 16%, demand at Ford, GM, Renault

- Wausau Paper continuing talks w/ Starboard after co. declined offer to sign non-disclosure

EARNINGS:

- Bank of New York Mellon (BK) 6:30am, $0.53

- Comerica (CMA) 6:40am, $0.65

- US Bancorp (USB) 6:45am, $0.75

- First Republic Bank/CA (FRC) 7am, $0.73

- JPMorgan Chase (JPM) 7am, $1.22 - Preview

- Northern Trust (NTRS) 7:14am, $0.75

- Goldman Sachs (GS) 7:30am, $3.66 - Preview

- M&T Bank (MTB) 8:01am, $2.17

- Charles Schwab (SCHW) 8:45am, $0.15

- Kinder Morgan Energy Partners (KMP) 4:05pm, $0.63

- Kinder Morgan (KMI) 4:05pm, $0.35

- El Paso Pipeline (EPB) 4:07pm, $0.55

- eBay (EBAY) 4:15pm, $0.69

- SLM (SLM) 4:15pm, $0.53

- Clarcor (CLC) 5:21pm, $0.70

- HB Fuller Co (FUL) 5:49pm, $0.56

- Bank of the Ozarks (OZRK) 6pm, $0.56

- CVB Financial (CVBF) 6:45pm, $0.22

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – what we didn’t like about commodity reflation 24hrs ago, we like this morning – Oil, Gold, Copper all stopped going up again at lower-highs (Dollar Up), which is a bullish global #GrowthStabilizing signal. Brent’s TAIL risk line of $111.48 is what matters most.

- Oil Trades Near One-Week Low as U.S. Crude Inventories Increase

- Carrara Marble Peaks as Russians Follow Etruscans: Commodities

- Bundesbank to Repatriate 674 Tons of Gold to Germany by 2020

- Wheat Rises to Three-Week High as Dry Weather Threatens Crops

- OPEC Cuts Oil Output to 14-Month Low Amid Economic Uncertainty

- Copper Declines for Fourth Day Before U.S. Production Figures

- NWR Selling Eurobonds as Yield on Coal Producer’s Debt Hits Low

- Cocoa Slides on Demand as Crop Outlook Improves; Sugar Unchanged

- Platinum Getting More Precious on Tight Supply: Chart of the Day

- Goldman Sachs Prefers Copper, Palladium, Metallurgical Coal

- U.S. Oil-Product Exports Exceed 2009 Imports to Drive Ship Surge

- Icahn’s Transocean Buy Pushes Driller Toward Partnership: Energy

- Louis Dreyfus Joins With Australia’s Namoi Cotton to Boost Sales

- Gold Swings Between Gains and Declines on Debt, Growth Concerns

CURRENCIES

YEN – Currency War is on. After getting lit up like a Christmas tree, the Yen just bounced for 2-days (Nikkei down -2.6% overnight on that as Government Intervention ramps implied market volatility), so we’ll be looking to re-short the Yen inside of $88 (vs USD) if/when we get that signal today. This is just wild to watch.

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team