Easing footwear import taxes is probably not at the top of the Obama Administration's agenda, but a bill to do so is gaining support. Payless would be the big winner by a long shot.

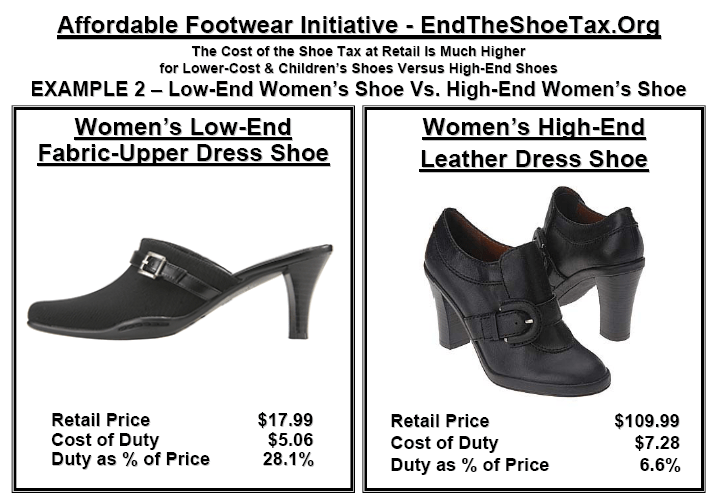

The re-introduction of the Affordable Footwear Act to the Senate is the latest potential tailwind for the footwear supply chain. Originally designed to protect the domestic footwear manufacturing sector in the 1930s, the tax is now obsolete with imports accounting for 99% of all shoes sold in the U.S. In 2008, the government collected over $1.7B in duties on imported shoes. This bill would eliminate nearly $800mm in duties by removing the tariffs on all children's footwear as well as lower cost shoes with fabric uppers. While an attempt to pass the bill in 2007 was unsuccessful, it has stronger bipartisan support in Congress this time around. Since this tariff no longer protects domestic jobs and is responsible for up to 40% of the cost of low-end footwear, we can't ignore the potential for some form of the bill to get passed.

So who benefits from a footwear retail perspective if the bill is passed? You want to look for low margin companies with vertical sourcing, branding and retailing bases. Yes, that pretty much makes the top three beneficiaries Payless, Payless and Payless. Collective Brands (Payless) not only has the greatest exposure to children's footwear (see chart), but it is also has the lowest average price point of the group. Therefore, a greater percentage of its women's and men's footwear sales will also be subject to lower tariffs.

Assuming that that figure is approximately one-third, the company could potentially reduce the cost of half its sales by roughly 30% on average. Now how much of that savings gets passed along to the consumer versus printed in profit is anyone's guess - but in the past such price changes ended up being shared fairly evenly throughout the supply chain to the consumer. While it is far from a done deal, the timing could provide further support for a reacceleration of FCF in late 2H F09/ 1H F10.

Casey Flavin