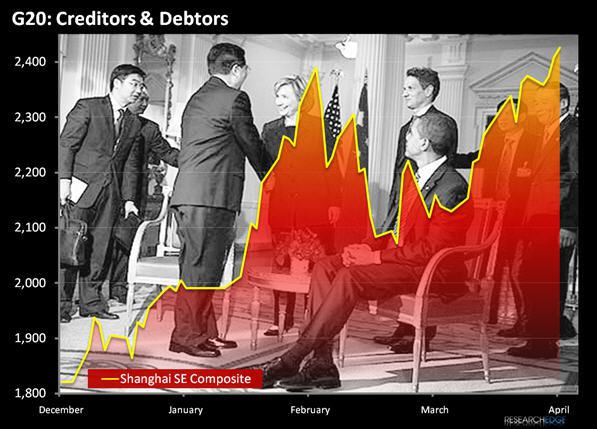

On this morning's 830AM Macro Client call, I was asked what my #1 takeaway was from this past week's G-20 meetings. Rather than hash up some of my prose, there is nothing more powerful that can summarize my thoughts than the picture Andrew Barber and I put together below.

China has the cash. China is America's Creditor. China remains The Client. The US Dollar is going to be the intermediate term loser born out of this economic crisis. That's the marked-to-market price America has to pay for the malfeasance of those who are, unfortunately, part of the American Financial System team.

In a perverse way, and in the immediate term, Breaking The Buck remains bullish for anything that Main Street Americans would like to see REFLATE. From their 401ks to their homes, that's really all that matters.

Let's start hoping that this country's handshake starts to matter again, and soon...

Keith R. McCullough

Chief Executive Officer