We're booking the gain in our #Real-Time Alerts on $FNP, which we added last week on the long side into ICR as TRADE factors were aligning nicely. We remain big bulls on FNP across our TREND and TAIL durations, and think that this stock should approach $20 over 12-18 months.

Following a checkered history of guiding Street expectations, it looks like FNP is off to a constructive start to fiscal 2013. The company’s preliminary results for Q4 and initial 2013 outlook out this morning are in-line and appear conservative respectively. The biggest delta relative to 2013 expectations is at Juicy – little surprise there. Kate and Lucky are right on track in terms of growing both revenues and expanding profitability. This is the core consideration driving FNP’s value as we remain confident that Juicy will divested at some point in 2013 uncovering the underlying value of these brands in the process.

Here are a few highlights from the morning’s release:

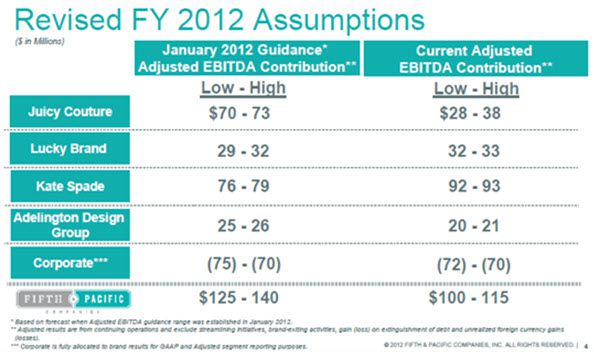

- Q4/F12 update – check. Results came in towards the lower-end of previously revised guidance on 10/1 including a $3mm hit from Sandy. FY12 adj. EBITDA of $100-$105mm at the low-end of prior $100-$115mm outlook; Q4 update of $63-$68mm at the low-end of implied $64-$79mm. Given largely disappointing results out of peers driven by weak holiday sales, we view these results a net positive.

- Kate Spade – check. Comp growth outlook in the low-teens is consistent with how management has approached prior years. In F11 & F12, management has admittedly outperformed their initial targets for the brand by a wide margin. We expect this year to be no different. We’re modeling 16% comp growth this year, which does not require a heroic performance in order to achieve.

- Lucky – check. Looks solid and 2013 profitability is coming in higher than we expected.

- Juicy – fail. Revenues remain challenged significantly impacting profitability for the foreseeable future. While Kate and Lucky adjusted EBTIDA each came in $1-$3mm above previously revised expectations for the quarter, Juicy contributed $5-$15mm less than expected as performance deteriorated across all business channels (DTC, wholesale, and outlet). This is not a cost issue, it’s about strategy/execution. We’re sure that new CEO of the brand Paul Blum has some great ideas about how to turn the brand around in 2013, but time is running out with the brand not only not keeping pace with Kate and Lucky, but generating a negative incremental $20-$30mm hit to EBITDA in 2013.

- It's also worth highlighting CEO Bill McComb's closing remarks in the release which underscore the potentail for a divestiture:

"The management team and Board of Directors of Fifth & Pacific are committed to delivering value to our shareholders. This includes making resource allocation decisions today that support strong long term growth within our current strategy as well as being thoughtful regarding alternatives to our current multi-brand portfolio approach that unlock value."

- Hosting FNP Dinner Jan 16th: We will be hosting a dinner with the management (CEO Bill McComb, CFO/COO George Carrara, and SVP of Finance Bob Vill) on the night of Wednesday the 16th. Clients who are interested can contact .

All in, initial guidance is roughly $25mm below our expectations. We expected management to set guidance near the Street’s $160mm view and it came in lower at $120-$150mm reflecting Juicy’s $20-$30mm delta compared to our base-line expectations (we expect Kate Spade to generate at least $160mm in EBITDA alone). The implied EPS range is $0.00-$0.15 in FY13 EPS compared to our $0.35 number (we also assumed lower interest expense). While we think upside at both Kate and Lucky will ultimately account for that differential at year-end, the bigger call here is that there is little question that Juicy is impacting FNP’s value – investors know this and our sense is that if the Board/management isn’t willing to accelerate action here, investors likely will.

(1/14/13 F12 Update):

(10/1/12 revision announcement):

Initial 2013 Outlook:

FNP Quantitative Risk Management Levels: