-- For specific questions on anything Europe, please contact me at to set up a call.

Position in Europe: Short Italy (EWI)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed down -0.3% week-over-week vs +3.2% in the week prior. Bottom performers: Cyprus -6.9%; Poland -0.9%; Czech Republic -0.8%; Germany -0.8%; Slovakia -0.8%; Belgium -0.8%. Top performers: Portugal +4.6%; Italy +3.2%; Spain +2.7%; Romania +2.4%; Russia (MICEX) +2.2%; Denmark +2.0%; Turkey +1.8%; Switzerland +1.8%; Hungary +1.8%; Greece +1.6%. [Other: France -0.6%; UK +0.5%].

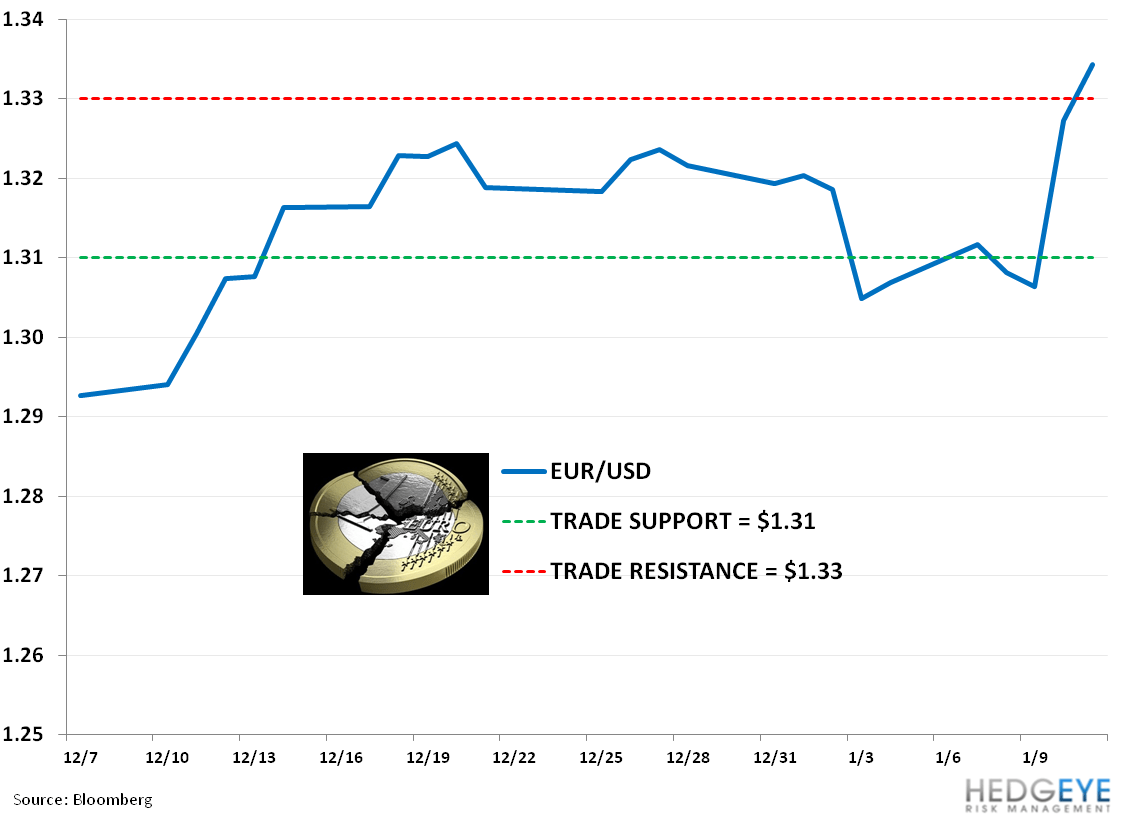

- FX: The EUR/USD traded up +2.13% week-over-week. W/W Divergences:RON/EUR +0.93%; PLN/EUR +0.02%; DKK/EUR -0.04%; NOK/EUR -0.76%; CHF/EUR -0.78%; CZK/EUR -0.83%; SEK/EUR -1.09%; ISK/EUR -1.19%; TRY/EUR -1.40%; GBP/EUR -1.71%; RUB/EUR -1.91%; HUF/EUR -1.92%.

- Fixed Income: The 10YR yield for sovereigns across the periphery were mixed week-on-week. Greece gained +49bps to 11.75% and Germany rose +5bps to 1.58%, while Spain fell the most at -17bps to 4.89%, Italy fell -13bps to 4.13%, and Portugal declined -12bps to 6.21%. France was basically flat and the UK lost -4bps to 2.08 on the week. The major call-out is that Spanish 10YR fell below the 5% line this week, the first time since March 2012!

EUR/USD: Our TRADE range is $1.30 – 1.32

- Our call - the EUR/USD will trade within our quantitative levels and reflect much of the daily headline risk (from Spain and Italy in particular). We think that ECB President Mario Draghi’s September announcement that “the ECB is ready to do whatever it takes to preserve the euro”; the resolve of Eurocrats to maintain the Union at all costs; and the January ECB meeting in which there was unanimous decision to not changing rates will all keep a heavy line of support in the cross.

- Yet we expect a long road towards a fiscal union as states will be reluctant to give their sovereignty up to an external entity, which should limit the cross’ upside.

- A bullish data point comes from CFTC data for net non-commercial positions in the EUR/USD that shows an improving trend since May 2012 and even turned positive on 1/1/2013, the first time since August 2011.

Shorting Berlusconi’s Hair Plugs:

It was a week of waiting and watching to see if the ECB would make any changes to its base rates. Consensus was firmly against a cut, which turned out to be correct. Draghi was particularly optimistic about the performance of Eurozone financial markets and conditions over the last six months in his press conference remarks, but had a much more somber tone in describing the economic outlook for the region.

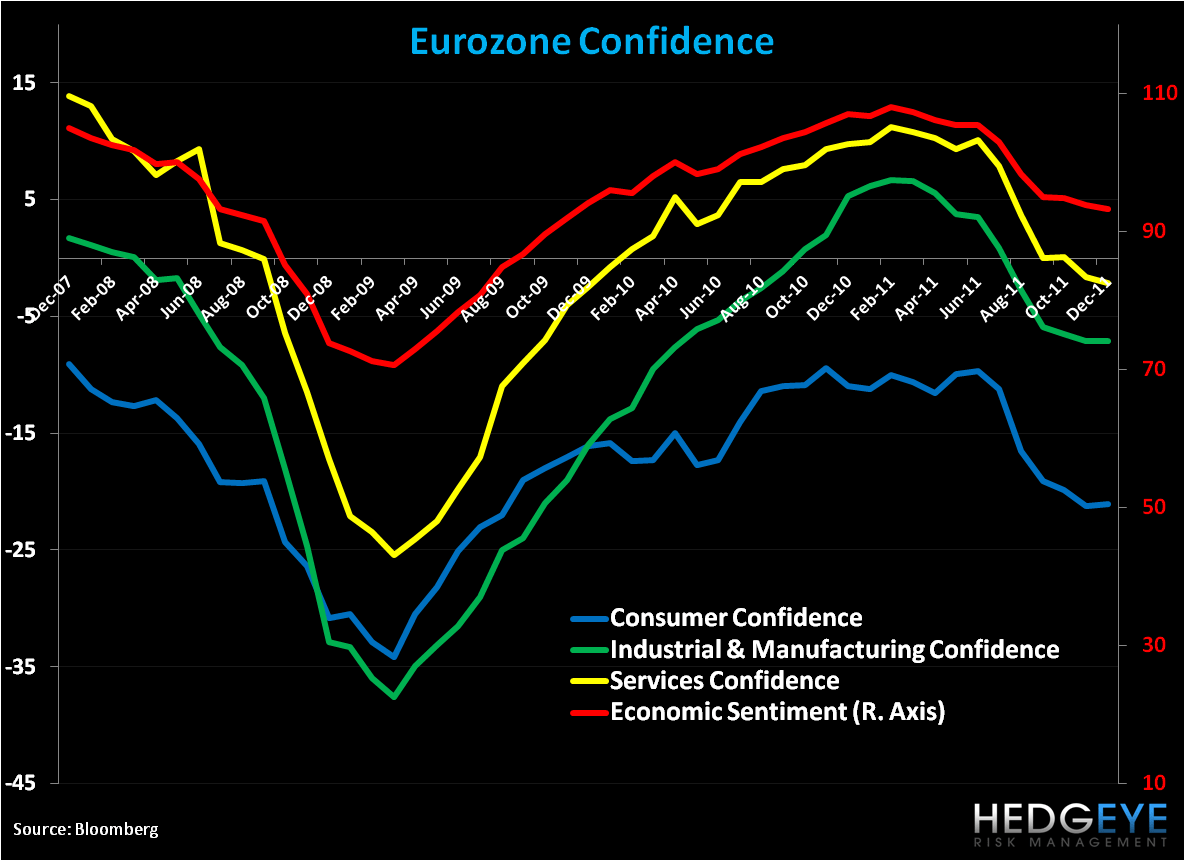

We too wrestle with the mismatch between the broader economy and market conditions. This week we got Eurozone confidence figures that showed signs of flattening to slight improvement. Conversely, ECB loans to households and non-financial corporations have yet to arrest their decline/show a meaningful inflection, the unemployment rate for the Eurozone ticked up to 11.8%, and CPI and PPI remain elevated and situate the region in stagflation. For more on the ECB decision see our note titled January ECB Presser: Draghi’s Optimism in No Real Recovery.

We added Italy via the etf EWI to our Real-time positions on the short side on 1/10/13 at $14.23. We think there is a significant amount of pain on the short side of Italy with the eff immediate term TRADE overbought. The high level of uncertainty on the future coalition government in Italy is one development we’re following closely. Former PM Berlusconi continues to be a wedge across parties and it’s unclear how the market will react should Monti not stand in a key position to assure adherence to austerity measures enacted under his watch. For more on Italy please see our note titled Italy’s Uneven Footing.

The European Week Ahead:

Monday: Nov. Eurozone Industrial Production; Dec. Germany Wholesale Price Index (Jan. 14-18); Dec. UK RICS House Price Balance; Nov. Spain House Transactions; Nov. Italy Industrial Production; General Government Debt

Tuesday: Nov. Eurozone Trade Balance; 2012 Germany GDP, Budget; Dec. Germany CPI – Final; Dec. UK PPI Input, PPI Output, CPI, RPI; Nov. Germany ONS House Price; Nov. France Central Government Balance; Dec. Spain CPI – Final; Dec. Italy CPI - Final

Wednesday: Dec. Eurozone EU27 New Car Registrations, CPI; Germany Economy Minister Roesler Presents New Economic Outlook; Nov. Italy Trade Balance

Thursday: ECB Publishes Monthly Report; Jan. Eurozone Bloomberg Economic Survey; Nov. Eurozone Construction Output; Jan. Germany Bloomberg Economic Survey; Jan. UK Bloomberg Economic Survey; Jan. France Bloomberg Economic Survey; Jan. Spain Bloomberg Economic Survey; Jan. Italy Bloomberg Economic Survey; Jan. Greece Bloomberg Economic Survey

Friday: Dec. UK Retail Sales; Nov. Italy Industrial Orders, Industrial Sales

Call Outs:

Basel Committee - Banks won a four-year delay to fully meet international liquidity requirements and will be able to pick from a longer list of assets, including stocks and mortgage debt, following a deal struck by regulatory chiefs meeting yesterday in Basel

France - French Budget Minister Jerome Cahuzac said on Sunday that the Hollande government is not planning any tax increases for the next few years in an effort to offer stability and visibility to both individuals and companies. The highly controversial 75% tax on people making more than €1M a year was recently rejected by the French Constitutional Court. However, the government is preparing a new bill to maintain the key components of the tax hike.

Cyprus - Moody’s downgrades Cyprus 3 notches to Caa3 from B3.

Ireland - S&P said on Friday that Ireland is expected to retain its investment grade credit rating from the agency in 2013, despite its negative outlook.

ESM - held its first debt auction and sold €1.927B of 3M T-bills, average yield (0.0324%), bid to cover 3.2x.

ESM Investment - Japanese Finance Minister Taro Aso said that his country will buy bonds issued by the ESM, along with euro-denominated sovereign debt.

Eurogroup – Reuters, citing officials, reported that Dutch Finance Minister Jeroen Dijsselbloem is likely to be named the next chairman of Eurozone finance ministers (succeeding Luxembourg's Prime Minister Jean-Claude Juncker), when it is set decide on 21-Jan. There’s speculation that German Finance Minister Schaeuble wouldn’t get the job over concerns that he may have alienated too many colleagues in southern Europe.

Italy - Bank of Italy data noted that Italian banks held a total of €271.8B from the ECB at the end of December, down from €273.3B at the end of November.

Spain - the Spanish Treasury said that its gross bond issuance target for 2013 was €121.3B, a 7.6% increase from total 2012 debt sales.

Cyprus - the German newspaper Handelsblatt, citing sources close to the negotiations, reported on Wednesday that Cyprus can only expect a bailout in early March after its presidential election next month. The paper said that Cyprus holds presidential elections on 17-Feb and 24-Feb, and Eurozone finance ministers want to wait to work with the successor to outgoing communist President Dimitris Christofias. It noted that Christofias, who is not seeking reelection, has rejected the sale of state companies that would generate the privatization revenues needed for reform. The article also discussed some of the potential backlash in the German Bundestag when it comes to approving a rescue for Cyprus, highlighting the increasingly hard-line stance by the SPD on the issue of tax evasion.

Data Dump:

Eurozone Retail Sales -2.6% NOV Y/Y vs -3.2% OCT

Eurozone Unemployment Rate 11.8% NOV vs 11.7% OCT

Eurozone Sentix Investor Confidence -7.0% JAN Y/Y vs -16.8% DEC

Eurozone PPI 2.1% NOV Y/Y vs 2.6% OCT

Eurozone Consumer Confidence -26.5 DEC Final vs initial -26.6

Eurozone Business Climate Indicator -1.12 DEC vs -1.17 NOV

Eurozone Economic Confidence 87.0 DEC vs 85.7 NOV

Eurozone Industrial Confidence -14.4 DEC vs -15.0 NOV

Eurozone Services Confidence -9.8 DEC vs -11.9 NOV

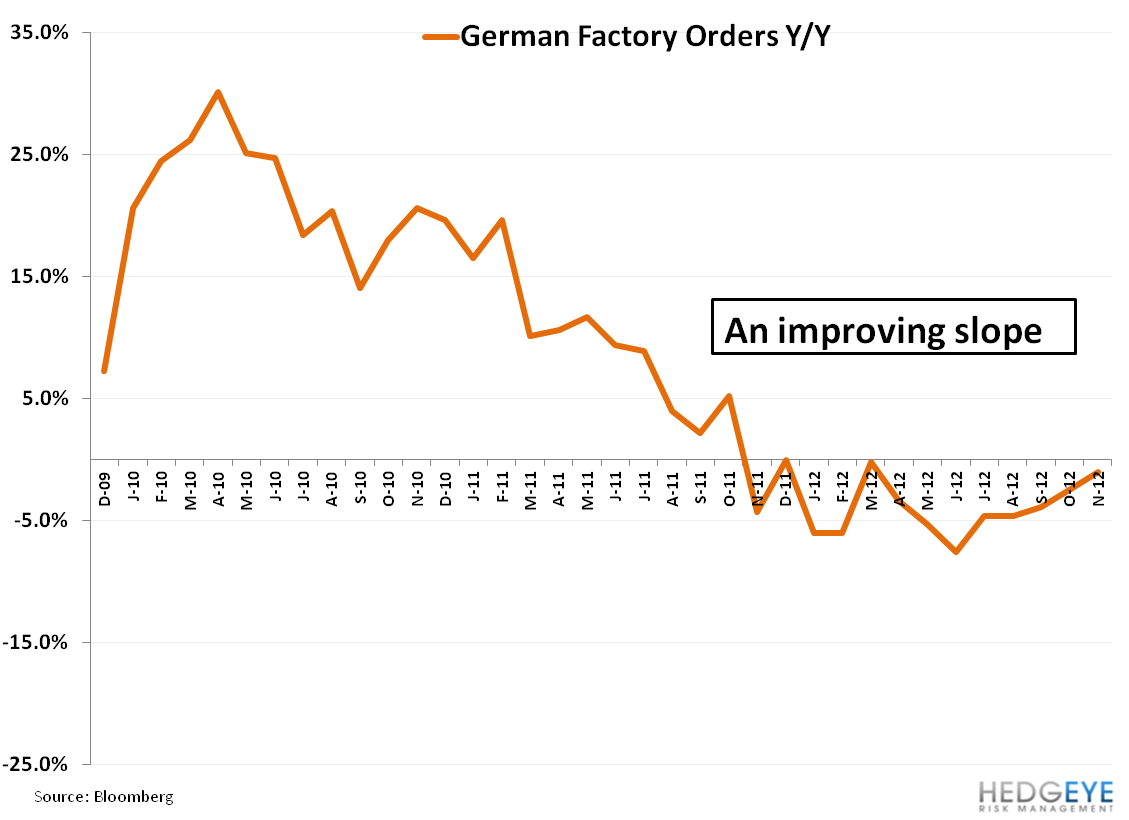

Germany Factory Orders -1.0% NOV Y/Y vs -2.5% OCT

Germany Imports -3.7% NOV M/M vs 2.9% OCT

Germany Exports -3.4% NOV M/M vs 0.2% OCT

Germany Trade Balance 17.0B EUR NOV vs 15.7B EUR OCT

Germany Industrial Production -2.9% NOV Y/Y vs -3.0% OCT

France Bank of France Business Sentiment 95 DEC vs 91 NOV

France CPI 1.5% DEC Y/Y vs 1.6% NOV

France Industrial Production -3.6% NOV Y/Y vs -3.4% OCT

France Manufacturing Production -4.6% NOV Y/Y vs -3.7% OCT

UK Halifax House Prices -0.3% DEC Y/Y vs -1.3% NOV

UK Car Registration 3.7% DEC Y/Y vs 11.3% NOV

UK Industrial Production -2.4% NOV Y/Y vs -3.0% OCT

UK Manufacturing Production -2.1% NOV Y/Y vs -2.0% OCT

Italy Unemployment Rate 11.1% NOV vs 11.1% OCT (youth unemployment 37.1%)

Italy Deficit to GDP (YTD) 3.7% in Q3 vs 4.7% in Q2

Spain Industrial Output -7.3% NOV Y/Y vs 0.9% OCT

Portugal Consumer Confidence -59.8 DEC vs -59.0 NOV

Portugal Economic Climate Indicator -4.4 DEC vs -4.3 NOV

Portugal Industrial Sales -5.9% NOV Y/Y vs 0.4% OCT

Portugal Construction Works Index 53.6 NOV vs 55.2 OCT

Portugal CPI 2.1% DEC Y/Y vs 1.9% NOV

Norway Credit Indicator Growth 7.1% NOV Y/Y vs 6.9% OCT

Norway Industrial Production -3.5% NOV Y/Y vs 2.5% OCT

Norway Industrial Production Manufacturing 2.4% NOV Y/Y vs 2.7% OCT

Norway CPI 1.4% DEC Y/Y vs 1.1% NOV

Sweden CPI -0.1% DEC Y/Y vs -0.1% NOV

Sweden Industrial Production -4.3% NOV Y/Y vs -4.3% OCT

Netherlands CPI 3.4% DEC Y/Y vs 3.2% NOV

Netherlands Industrial Production 0.7% NOV Y/Y vs -1.7% OCT

Finland Industrial Production -1.9% NOV Y/Y vs -0.3% OCT

Switzerland CPI -0.3% DEC Y/Y vs -0.1% NOV

Switzerland Unemployment Rate 3.3% DEC vs 3.1% NOV

Ireland Industrial Production -6.2% NOV Y/Y vs -16.6% OCT

Austria Wholesale Price Index 2.7% DEC Y/Y vs 2.8% NOV

Belgium Unemployment Rate 7.4% NOV vs 7.4% OCT

Greece Industrial Production -2.9% NOV Y/Y vs 2.0% OCT

Greece Unemployment Rate 26.8% OCT Y/Y vs 26.2% September

Greece CPI 0.3% DEC Y/Y vs 0.4% NOV

Russia Consumer Confidence -8 in Q4 vs -6 in Q3

Russia CPI 6.6% DEC Y/Y Final [unch vs initial]

Czech Republic CPI 2.4% DEC Y/Y vs 2.7% NOV

Czech Republic Unemployment Rate 9.4% DEC vs 8.7% NOV

Czech Republic Retail Sales -1.8% NOV Y/Y vs 2.2% OCT

Romania Q3 GDP Final -0.5% Y/Y [vs initial -0.6%] [-0.4% Q/Q [vs initial -0.5%]

Romania Retail Sales 3.0% NOV Y/Y vs 0.7% OCT

Romania Industrial Sales 4.6% NOV Y/Y vs 9.4% OCT

Romania CPI 5.0% DEC Y/Y vs 4.6% NOV

Estonia CPI 3.5% DEC Y/Y vs 3.6% NOV

Estonia Exports 9% NOV Y/Y vs 10% OCT

Estonia Imports 3% NOV Y/Y vs 21% OCT

Hungary Producer Prices -2.9% NOV Y/Y vs 0.2% OCT

Hungary Industrial Production -6.9% NOV Y/Y vs -3.8% OCT

Slovenia Industrial Production -3.6% NOV Y/Y vs 2.0% OCT

Slovakia Industrial Production 5.2% NOV Y/Y vs 8.1% OCT

Slovakia Avg Monthly Wage 0.1% NOV Y/Y vs 1.3% OCT

Turkey Industrial Production NSA 11.3% NOV Y/Y vs -5.7% OCT

Interest Rate Decisions:

(1/7) Romania Interest Rate UNCH at 5.25%

(1/9) Poland Base Interest Rate CUT 25bps to 4.00%

(1/10) BOE Main Interest Rate UNCH at 0.50% and QE unchanged at £375B

(1/10) ECB Main Interest Rate UNCH at 0.75%

(1/10) ECB Deposit Facility Rate UNCH at 0.00%

Matthew Hedrick

Senior Analyst