There's a lot of reasons to get on the 'short Ackman' train and be negative on JCP. In light of today's downgrade by one of the big brokers, we want to make our current position clear. Specifically, there are a lot of reasons to eliminate the thought of going long JCP for someone that cares about fundamentals. But we think that a short beyond a near-term trade could prove outright reckless -- at least without considering the factors we outlined in our 12/13/12 note (JCP: Reasons To Reconsider Your JCP Short).

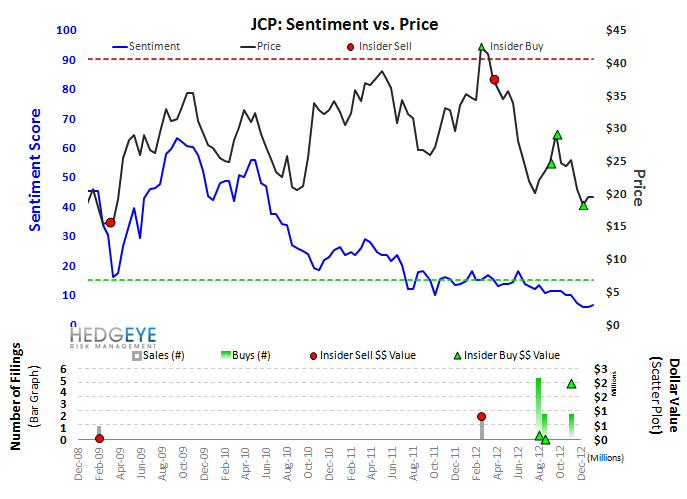

An added factor is our Sentiment Monitor. Currently, JCP is the only retailer that has a Sentiment Score below 10 (on a scale of 100). Mind you, this was calculated before today's downgrade, so the real score is likely 1-2 points lower. The point is that this extreme bearish sentiment is a very bullish signal -- as proven statistically by our models. It's important to note that this sentiment is present as the stock is en route to retesting 12-month lows of $16.28. Mind you, that's also the level where we started to see the largest inside Buy cluster in years.

JCP: Reasons To Reconsider Your Short (12/13/12)

We’ve thought from Day 1 that there’s no shortage of reasons to be bearish on JCP. Structurally, we still think that’s the case. But stocks don’t trade in a vacuum, and on the short side, we would not touch this one with a 20-foot pole in the high teens. Our purpose here is not to convince anyone to buy JCP. But rather to explore as many factors as possible that could prove a short position painfully wrong.

Details

We recently spent two weeks on the road, and JCP name was a topic of discussion in 8 out of 10 meetings. The only one that rivals it in terms of controversy is Nike. The irony here is that despite the overwhelming bearishness – 40% of float short and bulls capitulating with less than 30% recommending JCP as a Buy – the topic we encountered most on the road was “why not buy JCP here, as it seemingly has all the bad news we’re likely to see in the stock, and is discounting zero positive developments?” Out of all the people who raised that question, we could find maybe one who followed through and actually bought the stock here.

We think the reason is that if you buy it here and you’re wrong, it’s an offense that probably poses career risk for some. Buying JCP here is really taking a flier on Johnson getting ANYTHING right next year – even if by accident. Let’s face it, after so many self inflicted black eyes, the guy is due for a win. That blind assumption is hardly a sound investment process in our book. But if you want to stay bearish in the high teens, you should remember the following.

1) The ‘JCP is a Zero’ argument has been made about SHLD since that marriage was formed in the fall of 2004. And since then, the stock has underperformed with a -10% CAGR, but it has been flat for the better part of five years, and has been far from insolvent. We could make a good TAIL call about how JCP will prove to be a failure in 8 years – even sooner than that. But it has no bearing on how the stock trades next year. Initially we feel short sighted in saying that, but the facts are what they are, and we won’t ignore them.

2) Let’s look at the specific stock trading patterns from the week before the Sears/K-Mart deal was announced vs the week before Ron Johnson’s appointment as JCP CEO. They’re different types of events, but we put them both in the ‘hail Mary’ category and therefore comparable. For 10 months, the stocks followed almost the same EXACT trading pattern, until JCP’s egregiously low comp level pushed it down to new cyclical lows. JCP is now down 45% from the announcement, while SHLD was UP 45% at the same corresponding point in time (i.e. 1.5 yrs after announcement). The point is that there was ‘reason to believe’ 2-3 years into the SHLD story. It turned out to be unjustified, as SHLD is sitting at a mere $42 today, down 56% from the announcement of the deal. But if you were a ‘perma-short’ throughout the past 8 years, the early part of it was probably less than comforting. The chart below is self explanatory.

(note: This was published before by Lampert's subsequent decision to push out his CEO and assume the role himself)

3) Why does this ultra-long duration matter? Because that’s how Ron Johnson gets paid. Keep in mind that his warrants don’t vest until 2017. We can’t imagine that he did not get the Board’s full support before accepting the job to live through major jolts to the company’s financial nerve center. Without that, there’s no way he’d have taken the risk. Currently, his 50mm warrants are worthless. Above $29, he starts to see the fruits of his labor. His big mistake was not in trying to radically change the store. It was bowing to storytellers in the investment community and issuing near-term guidance around a story that would not play out until the intermediate-term had long passed.

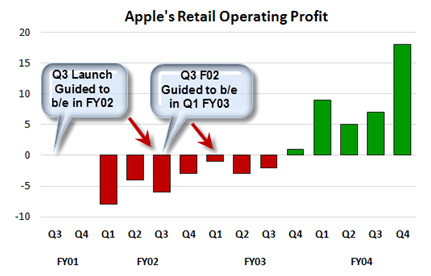

4) One thing to keep in mind is that Johnson is not afraid to miss near-term targets for long-term value creation. That’s painfully apparent to the bulls who suffered through the past three quarters of financial results. But his investments ultimately paid off. We’re the first to highlight how his toolbox at JCP pales in comparison to what he had at Apple. But the guy is not used to losing, and likely won’t go another year wearing that tattoo. Check out his performance at Apple. The retail business missed its guidance to hit break-even target twice in the early days. We’re currently seeing the miss, though obviously on a much greater scale. But he will likely tweak the equation in whatever way he needs in order to keep morale heading higher and fend off share loss.

5) Speaking of share loss, we don’t think its clear exactly how much share JCP has hemorrhaged in year 1. For the first three quarters of this year we’re talking over $2.7bn in share. When 4Q – the seasonally strongest quarter – comes out, we’ll be looking at something closer to $4bn in annual share. This is coming off a base of only $17bn in revenue. Our sense is that the M’s, GPS’, KSS’ and TJX’s of the world are underestimating how much share JCP is handing them. This is not a permanent share shift by any stretch. And given that these other retailers pretty much don’t have a clue as to how much share they are gaining, it’s tough for them to have a clear plan as to how to avoid giving it back.

6) The argument for comp improvement is tough to refute mathematically. Not only is JCP coming off –mid20% comp declines, but it is happening at the same time that an incremental 2-3% of its store base is being remodeled every month. With current sales per square foot sitting at a paltry $112 – yes, you read that right, $112 – and the new stores likely to clock in 30-40% above that level, it is tough for us to not get to a 20%+ positive swing in comps next year. One may wonder (as we do) how much the comp will cost them in terms of higher technology and deferred maintenance costs, we think that it will trade with the comp, not necessarily with profitability. We don’t think that’s appropriate, but we think it’s reality.

7) We think that the big risk here on the long side is simply cash flow. In other words, to be short the stock here, we think that you have to prove the company will run out of cash to fund its growth. That might happen, but not until 2-3 years down the road at the earliest. Before that, we’ll see the comp delta improve.

In the event that cash runs dry the company can follow in the footsteps of Dillards and most recently Loblaw, a Canadian food retailer that is spinning-out 80% its of its property assets and reinvesting the $7bn into its operating business. Yes, JCP would have to pay market rent on this property that is currently largely fully amortized. But again, for the first few years this would not matter. It would have the liquidity for Johnson to evolve the store base according to his plan.

With cash flow from operations YTD down -$655mm and net debt-to-equity at historical highs at 0.67x, the probability of JCP pursuing this option is still low, but increasing on the margin, and most importantly, the optionality is there.

JCP currently owns approximately 39% of its real estate, or 44.6 million sq. ft. Based on current rent and cap rates, we estimate JCP’s potential REIT value at $1.85Bn-$2.55Bn, or $8.25-$11.50 per share. Since the formation of a REIT provides the greatest benefit for retailers that own a substantial percent of their real estate, we’ve looked at the likely candidates (see chart below). Both Macy’s (55%) and Nordstrom (46%) own a greater portion of their store base compared to JCP, but even with 39% of its real estate owned, this is an option for Penney’s to consider.

While forming a REIT is not likely, one thing to keep in mind that Steven Roth is on JCP’s board. While Loblaw’s announcement may have roused speculation in the start of a potential trend, recall that Roth was one of the first to execute such a strategy when he bought Alexander’s out of bankruptcy in 1993 and converted it to a REIT. Roth has “been there and done that” before.