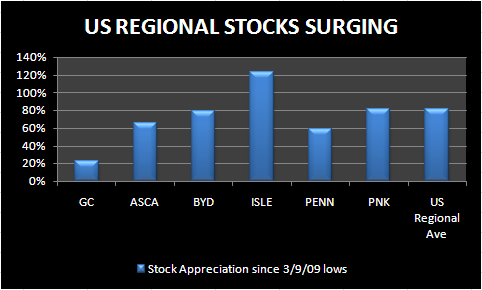

Trivia question: What regional gaming stock has not had a monster run? ASCA, ISLE, PNK, PENN, BYD? All of these are up huge, +81% on average since the March 9th low while Great Canadian is up only 23%. Hey, Great Canadian Gaming is a regional too. Where's the love? Sure they're Canadian. Some of my best friends are Canadian. Don't hold that against them.

THESIS

GC is a valuation story with catalysts. It's not without hair, but the overhangs appear to be behind the company with the exception of the economy. Historically, GC has traded at a higher multiple than its regional counterparts south of the border and rightfully so. GC has a better business model as Capex is generally reimbursed by the Canadian provinces. Right now, GC trades at 4x 2010 EBITDA versus the US regional operators at about 6x. That disparity shouldn't exist.

So is this a value trap? I don't think so. There are some real catalysts:

- The Winter Olympics will be held in Vancouver in February, 2010. GC generates 80% of its EBITDA in Vancouver.

- In advance of the Olympics, The Canada Rail Line, opening later in 2009, will include a stop right in front of River Rock, GC's largest property. River Rock is only 8 miles from the airport on the Canada Line and will be the only gaming facility with a stop. The incremental traffic flow from the Olympics should be huge, albeit temporary. However, the rail stop is permanent.

- Cash flows should stabilize as comparisons ease from lapping the smoking ban in April of 2008, and the opening of two competing properties, Starlight and Burnaby (opened 12/07 and 12/08, respectively). There won't be any new supply for years.

- GC's largest competitor in Vancouver is Gateway Casinos which is a high probability bankruptcy candidate. This can only help GC's competitive positioning.

RISKS

The consumer economy is difficult and GC is facing more competition. However, the consensus numbers actually look reasonable. If GC can hit those numbers the stock can only go higher given the low valuation. Here are some of the negatives:

- - Small cap: Equity cap only $240MM

- - Canadian stock

- - Investors don't trust Ross McLeod - the Chairman & CEO and also the largest shareholder (25% of the float) - although he does have great governmental relations

- - Company has a history of low ROI investments since the money is "free". However the new COO & CFO seem to be more disciplined

- - Stock is illiquid

CONCLUSION

We may be early on this one. It wouldn't be the first time. However, considering the low relative and absolute valuation, and the recent surge in the US regional gaming stocks, the timing might be right as we get closer to the aforementioned catalysts.