We have long viewed Brinker as our favorite casual dining company and, heading into the core of earnings season, we maintain that view. Our bearish view on casual dining, as a category, is intact, but Brinker remains the most compelling long at a price.

Here are some thoughts pertaining to Brinker:

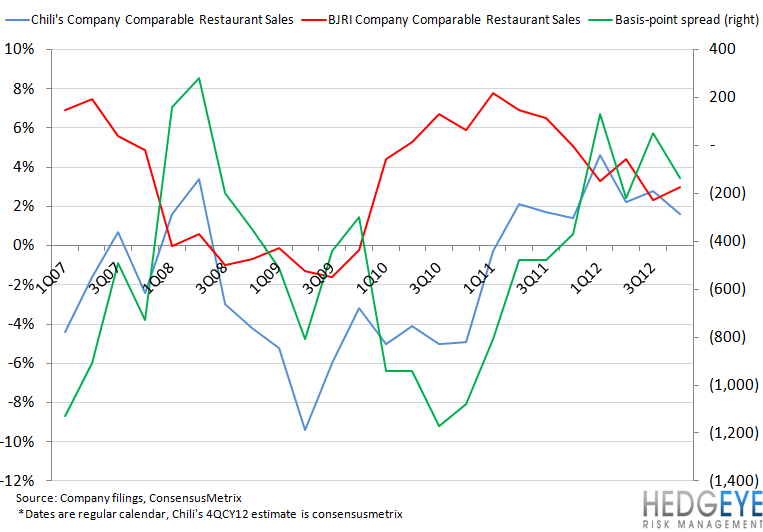

- Two casual dining companies have reported 4Q12 earnings thus far, BJRI and RT, reporting company comparable restaurant sales growth of 3% and 0.3%, respectively

- The bulk of the BJRI stores are located in the Western region of the US, while RT is a East/South East-centric brand. RT, a poorly managed concept, in our view, managed to eke out positive comps

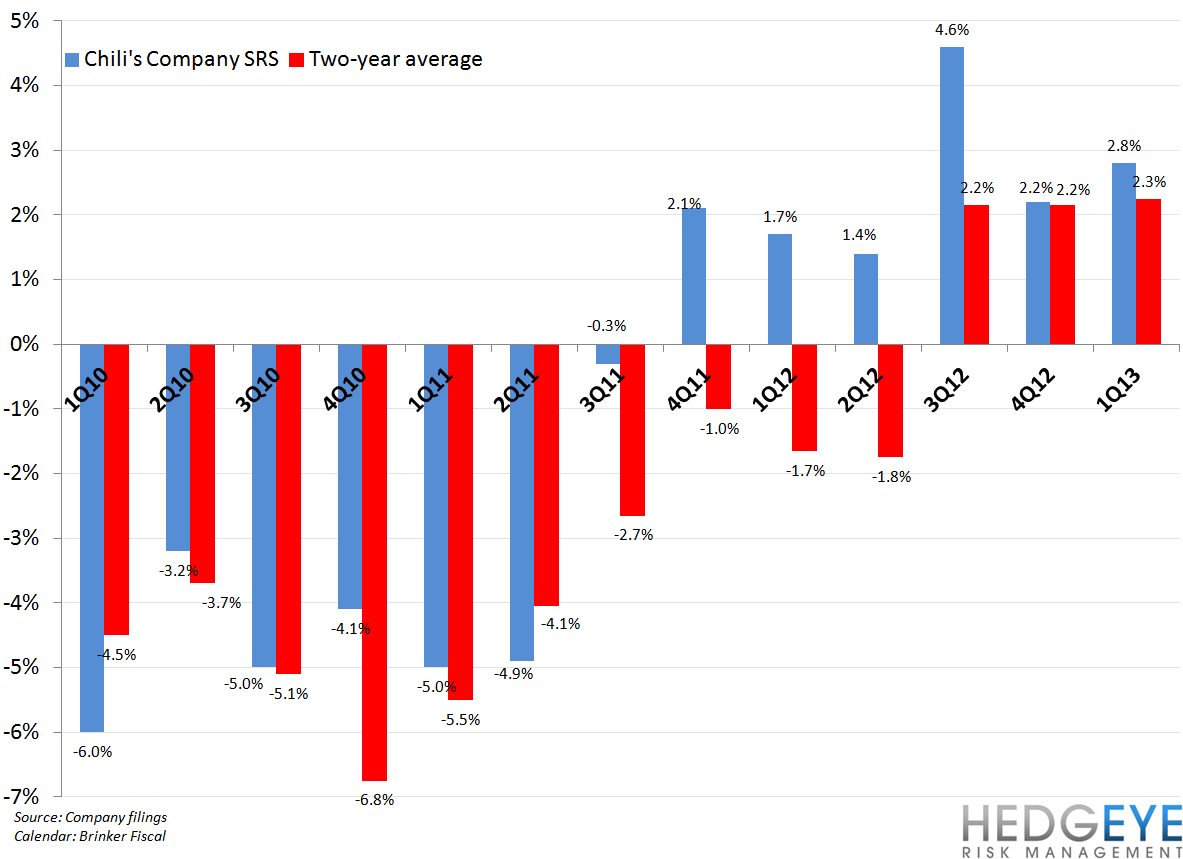

- Chili’s could produce 2% same-restaurant sales growth in 2QFY13 versus consensus of 1.6%. Momentum continues at Chili’s, thanks to kitchen enhancements and remodels. Channel checks and the early read in the competitive set suggest that the negative tone set on the last earnings call could have been overdone

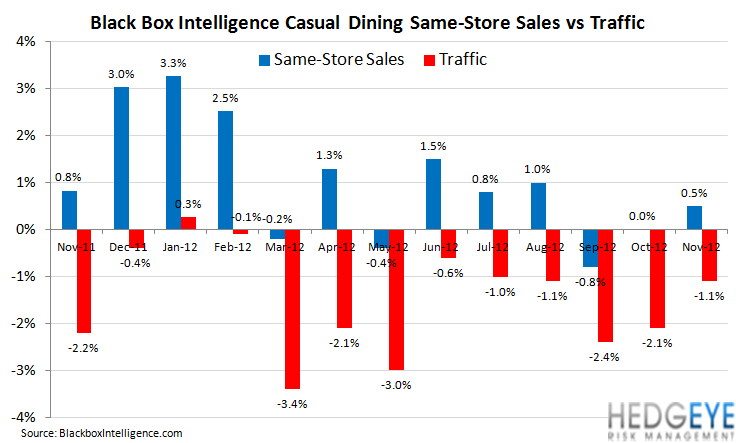

- Comparisons remain very difficult for the entire industry until March 2013

- ICR should offer incremental data points to allow investors a broader idea of how the industry has been performing

Howard Penney

Managing Director

Rory Green

Senior Analyst