TODAY’S S&P 500 SET-UP – January 11, 2013

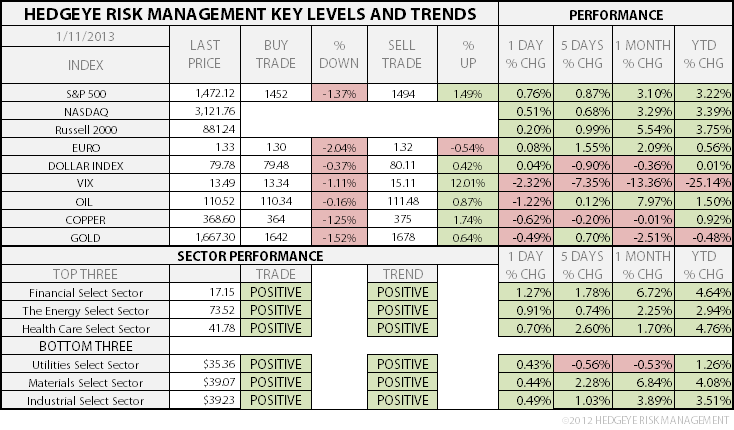

As we look at today's setup for the S&P 500, the range is 42 points or 1.37% downside to 1452 and 1.49% upside to 1494.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.64 from 1.65

- VIX closed at 13.49 1 day percent change of -2.32%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Import price index, Dec., M/m est. 0.1% (prior -0.9%)

- 8:30am: Trade balance, Nov., est. -$41.3b (prior -$42.2b)

- 9:30am: Fed’s Plosser speaks on economic outlook in N.J.

- 11am: Fed to buy $4.75b-$5.75b in 2017-2018 sector

- 12pm: Jan. WASDE report

- 1pm: Monthly budget statement, Dec., est. -$1b (prior -$86b)

GOVERNMENT:

- House, Senate not in session

- Deadline for FERC to respond to Deutsche Bank’s rejection of $1.6m in penalties

- CFTC holds closed meeting on enforcement matters, 10am

- Medicare Payment Advisory Commission meets on long-term care hospital services, competition in Part D, 8:30am

- ITC Judge Thomas Pender may release findings in patent-infringement case by Dover unit against Analog Devices over microphones in digital devices

WHAT TO WATCH

- Best Buy possible holiday sales drop may hurt Schulze buyout bid

- Trade gap in U.S. probably narrowed as fuel costs declined

- China’s inflation accelerates as chill boosts food prices

- Japan’s Abe unveils $116b stimulus package to boost growth

- American Express to cut 5,400 jobs, take $287m charge

- Boeing Dreamliner system said to be focus of FAA inquiry

- Cyprus facing world’s biggest bank bailout as Moody’s cuts 3 steps

- U.S. mortgage overhaul under way with borrower scrutiny measure

- Apple CEO Cook says China will overtake U.S. as biggest mkt

- Bats blaming market rules for mishaps as calls for overhaul grow

- Kocherlakota says Fed policy not easy enough with low inflation

- Citigroup joins Goldman in starting electronic bond-trade system

- Slim’s Sanborns said to seek $1b in share offer

- Li & Fung sees 2012 operating profit down 40% on U.S. costs

- Ex-hedge-fund manager Hochfeld pleads guilty to securities fraud

- Number of Euribor maturities must be halved, EU regulators say

- MF Global creditors file liquidation plan following settlements

- Ford plans 2,200 salaried hires in biggest increase since 2001

- U.S. Retail Sales, China GDP, Goldman: Wk Ahead Jan. 12-19

EARNINGS:

- Wells Fargo (WFC) 8am, $0.90 - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COMMODITIES – CRB Commodities Index has reflexive components (Oil and Copper don’t like the China down move because commodity bulls still think long commodity inflation is a demand story – we think it’s a money and physical commodity supply one); Copper down -0.8% here and Gold just failed at $1678 resistance again; we re-shorted Gold on green yest.

- Brent Oil Set for First Weekly Drop in Three on China Inflation

- Wheat Trade More Bullish Even as Bear Market Begins: Commodities

- Copper Falls as Inflation Fuels Concern China May Curb Stimulus

- Gold Falls as Strengthening Dollar Encourages Investors to Sell

- Soybeans Slide a Fourth Day as Report Might Ease Supply Concern

- Indonesia May Cut Palm Oil Tax to Zero to Counter Malaysia

- Iron Ore at 15-Month High Deters Restocking at China Mills

- Texas Energy Boom Fuels Best Performance Since ’09: Muni Credit

- Thai Sugar Output Seen by Macquarie 12% Down on Dry Weather

- Morgan Stanley Names Tan Head of Asia Commodities in Singapore

- U.S. LNG Profit Seen Elusive as Price Gap Closes: Energy Markets

- China May Increase Gold Holdings in Reserves, Researcher Says

- Chavez’s Food Shortages Bigger Worry Than Venezuela Constitution

- Rebar Tumbles Most Since November as China’s Inflation Quickens

CURRENCIES

FX – USD looks to keep making a series of long-term higher-lows as Commodities (CRB Index) makes a series of long-term lower-highs. The Yen, meanwhile, is a flaming ball of fire (Japan introduced a 10.3 TRILLION Yen Keynesian “stimulus” spending package overnight – that’s about $116B in USD, but who is counting anymore).

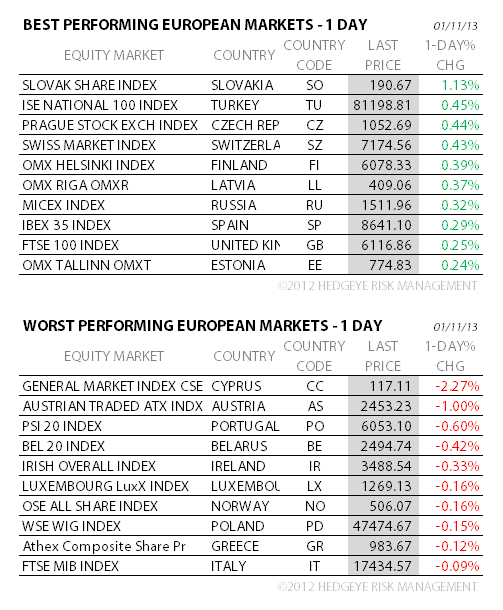

EUROPEAN MARKETS

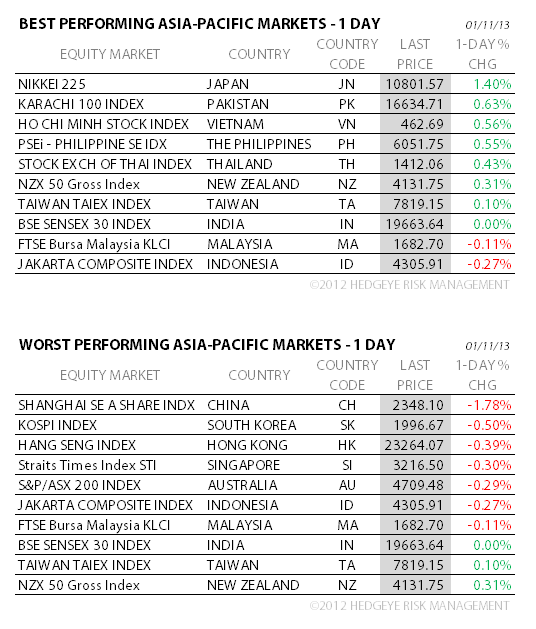

ASIAN MARKETS

CHINA – on the #growthstabilizing side they delivered a big Export print for DEC at +14.1% y/y (vs +2.9% last mth), but on the CPI front the number they made up didn’t deflate enough to keep the Shanghai Comp going higher (-1.8% overnight).

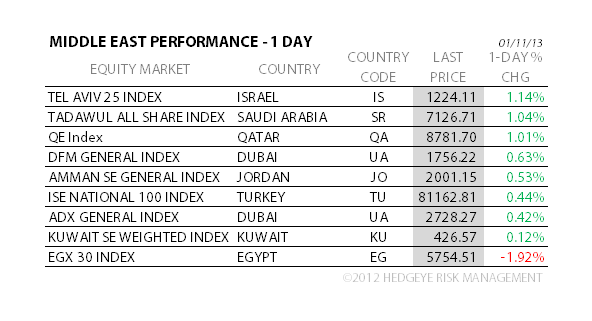

MIDDLE EAST

The Hedgeye Macro Team