Starbucks has two, potentially major, tailwinds in FY13 that could push the stock higher. Sentiment is a cause for concern but at this price we are positive on the stock.

Key Levels

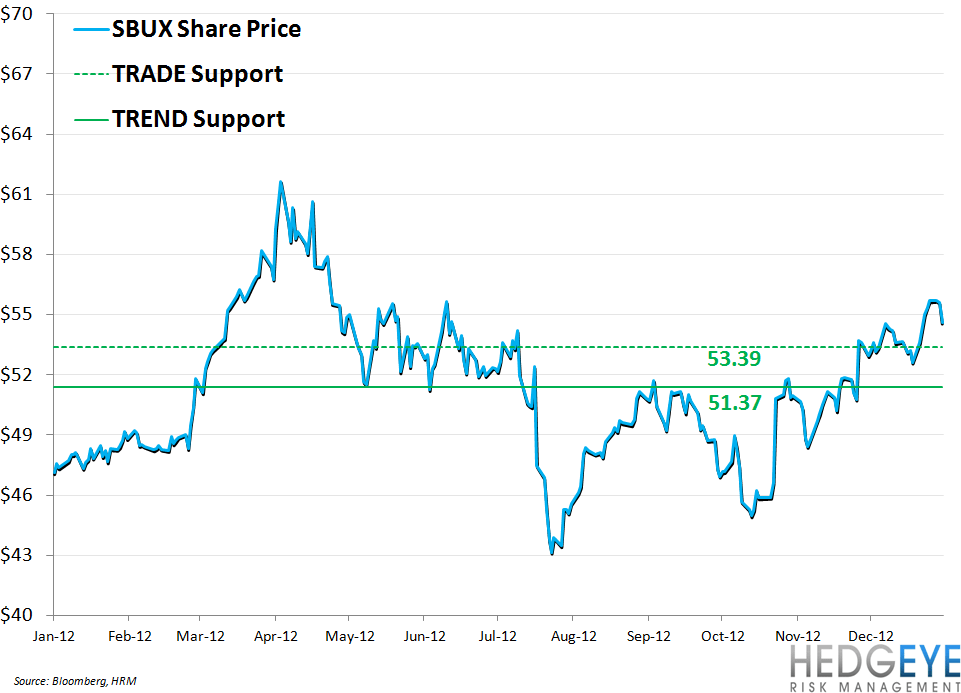

From a trading perspective, our macro team’s quant model is indicating that SBUX is in a bullish formation, with immediate-term TRADE and intermediate-term TREND support at $53.39 and $51.37, respectively.

Fundamental View

We believe that Starbucks is set to post another strong year in FY13 with its revenue drivers firing on all cylinders, coffee prices down ~40% year-over-year, and a macro outlook that suggests that the company’s high degree of leverage to the US economy could prove to be a benefit.

Revenues are expected to grow 12.7% in FY13, versus FY12, by the Street. We believe that this is possibly conservative given continuing momentum in CPG, including single serve, and the core retail business.

We believe that the flow of positive news regarding Starbucks, to which we have become accustomed, will continue in 2013:

- CPG could surprise to the upside as the availability of Evolution Fresh is expanded and the company continues to take share in single serve.

- International growth, particularly in China, was a key focus of the investor conference at the beginning of December and we expect management to continue to underline this potential throughout FY13

- Coffee costs constitute a significant tailwind and we expect incremental positive commentary on input costs to continue in FY13. Coffee needs are locked through 1HFY14 but, given the price decline since the company's most recent guidance, more positive news seems likely

Leverage in the P&L

Starbucks is part of a small group within the restaurant space that it is likely to see significant leverage in its P&L over the next 12 months. We believe, especially in casual dining, that consensus is overly optimistic about companies’ ability to grow earnings significantly faster than sales over the next year.

With strong momentum, effective sales initiatives, a fully-loaded CPG division, and impressive unit growth both domestically and internationally, we believe that top- and bottom-line estimates for Starbucks are likely to rise over the next three months.

Howard Penney

Managing Director

Rory Green

Senior Analyst