This note was originally published at 8am on December 27, 2012 for Hedgeye subscribers.

“Affairs are easier of entrance than exit; and it is but common prudence to see our way out before we venture in.”

-Aesop

Yesterday morning I was in the Canadian ski town of Banff, Alberta and today I found myself in Park City, Utah. Since this is my first trip to Park City, I must admit it is a very picturesque town. In fact, the beauty here almost offsets the fact the beers and cocktails are all watered down. Almost being the key word. But enough beating around the bush, today I’m going to jump right into it.

Yesterday morning in the Early Look I noted that violating the debt ceiling was imminent. Coincidentally or not, later in the day yesterday Treasury Secretary Geithner issued a press release stating that the statutory debt limit would be violated by December 31st but that the Treasury department could take extraordinary measures to extend the ceiling by an additional $200 billion. In the press release, it was also noted that:

1.) The extraordinary measures can create approximately $200B in headroom under the debt limit; and

2.) Under normal circumstances, that amount of headroom would last approximately two months. However, given the significant uncertainty that now exists with regard to unresolved tax and spending policies for 2013, it is not possible to predict the effective duration of these measures.

To summarize: while there may be two more months of flexibility, the uncertain policy environment makes it difficult to project. So, just as he is preparing to exit stage door left, Geithner sticks the markets with more uncertainty.

Managing through the fiscal and monetary crises that is looming over the next couple of months would actually require some discipline and willpower. Unfortunately, both of those attributes are currently in short supply in the hallowed halls of Congress. Yesterday, I referenced the book “Willpower” by Roy Baumeister and John Tierney. The authors actually provide some advice as to how to build willpower. They write:

“Religious people are less likely than others to develop unhealthy habits, like getting drunk, engaging in risky sex, taking illicit drugs, and smoking cigarettes. They’re more likely to wear seat belts, visit a dentist, and take vitamins … And they have better self-control, as McCullough and his colleague at the University of Miami, Brian Willoughby, recently concluded after analyzing hundreds of studies of religion and self control over eight decades.”

There you have it, a key way to build will power it to become religious. Sadly absent a mass baptism, I think it is unlikely that Congress gets fiscal religion in the coming weeks.

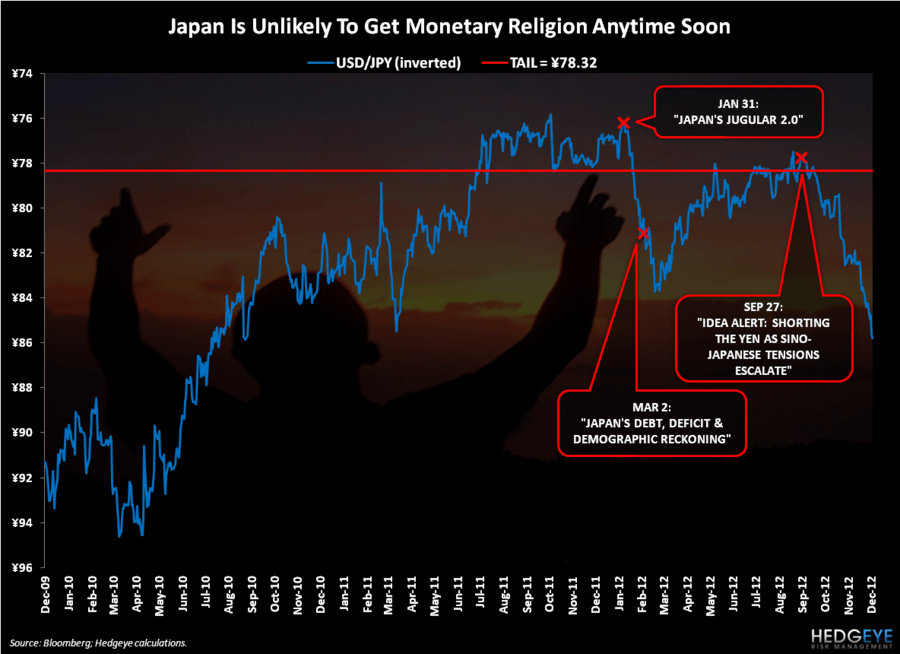

Speaking of getting monetary religion, or lack thereof, probably the most noteworthy move in global macro markets over the last month has been the utter collapse of the Japanese Yen. Shorting the Yen was actually our top Macro idea in our Best Ideas Call back on November 15th. The flip side of this trade has been an inflation of Japanese equities. The Nikkei 225 is now up 9% for the month of December and 22% for 2012. On one hand, an inflating stock market benefits those that own Japanese equities, but the longer term issue is that this flagrant printing of money actually leads to a loss of confidence in the Japanese currency with the second derivative being a loss of confidence in Japanese government debt.

The more looming concern in Japan may actually be the yet to be implemented fiscal policy of the new administration. As Darius Dale wrote yesterday in a macro note intraday:

“Abe and Aso will craft a “large-scale” supplementary budget for the FY12 year (likely > ¥10 trillion), as well as a FY13 federal budget. Regarding the latter, the previously-imposed ¥71 trillion spending cap for FY13 was recently disregarded by the LDP, suggesting Abe is poised to take public expenditures to new heights. In short, we think Japan’s pending fiscal and monetary POLICY mix risks igniting a backup in JGB yields that could threaten Japan’s fiscal sustainability, potentially triggering a European-style sovereign debt crisis.”

Now, clearly shorting Japanese government bonds has been called the “Widow Maker” trade for a reason. The reason being it has been an utter failure of a trade, but Japanese yields and CDS are starting to back up as the Japanese appear to be on the verge of entering a new era of indulgent Keynesian policy.

The truly scary fact about Japan is that almost 50% of the public budget is financed by debt issuance. Further, almost a quarter of the annual budget is actually used for debt service. Astoundingly this is occurring at a time when Japan’s weighted average cost of debt is as low as it has ever been. Clearly, any sustained back up in rates would be catastrophic for a country that already has a debt-to-GDP of 229%.

In positive news, yesterday we had more confirmation of the emerging housing market recovery in the United States. On a year-over-year basis, the Case-Shiller national home price index was up 4.3% in October, up from a 3.0% increase in September. On one hand, this is no surprise since Case-Shiller reflects Corelogic data on a lag. Regardless, as our Financials Sector Head Josh Steiner has been noting, the market, media and Main Street focus on Case-Shiller and the nature of the housing market recovery is that good news will feed on itself.

Could the housing recovering reach escape velocity in 2013? It is likely too early to tell, but our models continue to suggest home price recovery will come sooner than the consensus expects.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1634-1671, $108.95-111.58, $3.51-3.61, $79.06-79.92, $1.31-1.33, 1.70-1.85%, and 1412-1450, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research