This morning, privately held Cargill reported fiscal 2013 second quarter results – net earnings of $409 million versus $100 million a year ago. The earnings gains appeared to be broad-based across the company’s operating segments. Cargill’s business is broadly comparable to ADM’s in a number of segments and can provide some directional guidance with respect to business trends.

For example, the company called out North American farm services where Cargill was helped by large grain shipments in Canada but continued to feel the lingering effects of the drought and reduced crops in the Midwest (known issue for ADM). Cargill also did call out excess capacity in the North American ethanol market (again, known for ADM) but did mention the “return of profits in some product lines to more normalized levels” in the company’s food ingredient business. Finally, the company mentioned that an “improved margin environment in oilseed processing in several regions boosted earnings well above the year-ago level.”

While it is difficult to make specific comparisons given the lack of visibility in Cargill’s business, the magnitude of the earnings increase reported today is, at least, marginally comforting with respect to ADM’s upcoming earnings report (February 5th).

The issues highlighted by Cargill are well documented with respect to ADM. Both segments for ADM could be in a position to rebound as we move into 2013 and a new crop goes into the ground. With corn prices remaining at elevated levels, the incentive to plant corn certainly exists, and we expect that we will see corn planted fencepost to fencepost.

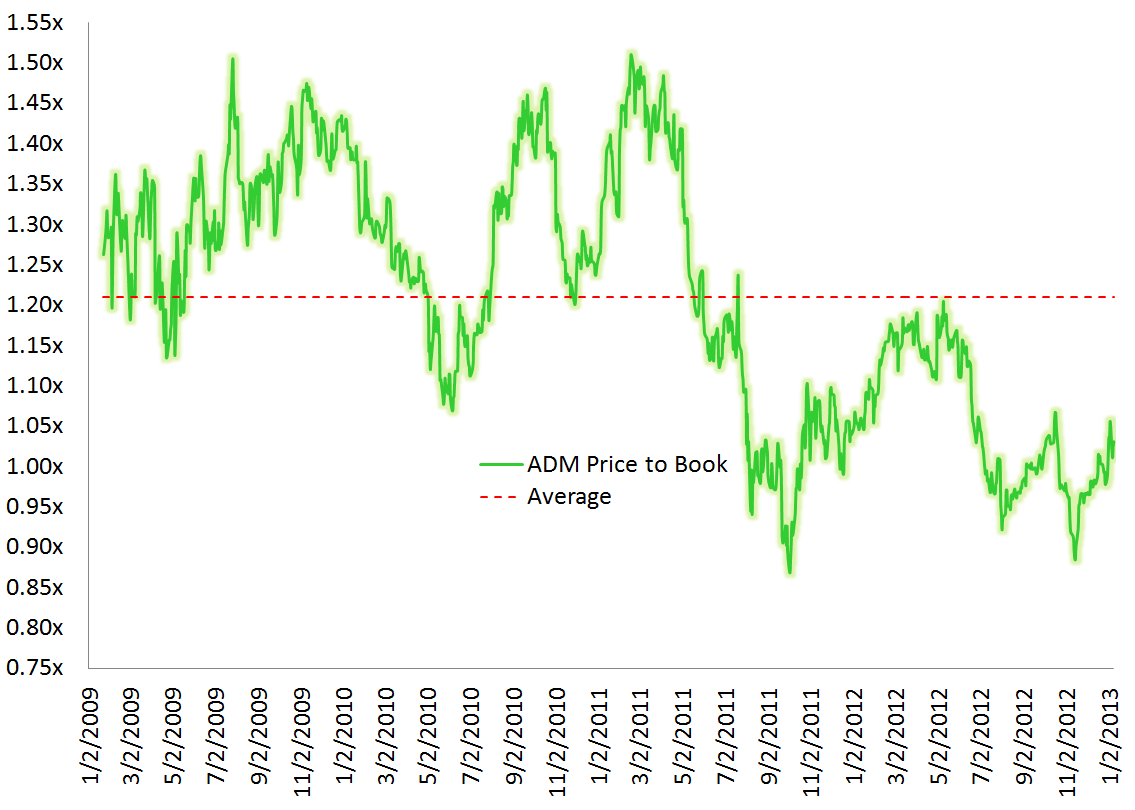

Given the valuation relative to historical norms, the risk/reward makes sense to us as we look out over the prospects for the 2013 crop year and likely planting decisions by farmers.

-Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC