Swiss National Bank intervenes to prevent appreciation of the Franc yet the negative economic fundamentals and weighting of the ETF will outstrip the positives of currency devaluation…

Position: Short Switzerland via the etf EWL

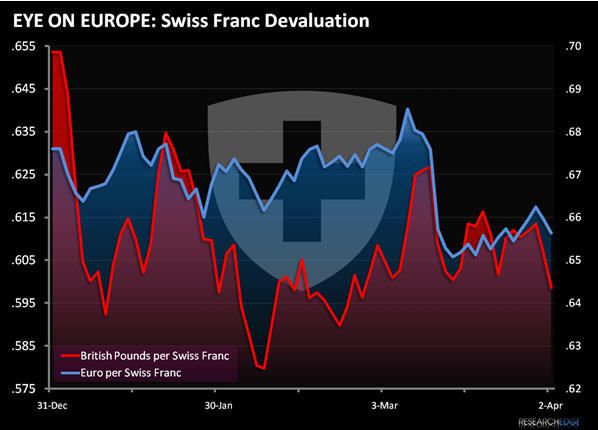

SNB started buying foreign currencies on March 12th to encourage devaluation of the Franc versus the Euro and Pound and reduced its benchmark interest rate to 0.25% to improve liquidity by lowering borrowing costs. The SNB is now continuing to devalue the Franc by buying foreign currencies and corporate bonds.

On the margin, Swiss monetary policy is positive. A weaker Swiss Franc will benefit exports to its largest trading partner, the Euro zone, and better match deflating prices and waning demand that are pushing down GDP. Since 3/09 the Franc has depreciated 3.7% versus the Euro and Pound.

The Swiss Market Index is down -9.7% YTD, but up +6.9% in the last four weeks. We shorted the Swiss etf EWL on 3/25 at an intermediate top.

Yet our negative outlook on the country is confirmed by Switzerland’s fundamentals. Despite the positive “spirit” coming from G20 along with the $1Tillion increase to the IMF’s balance sheet, Western Europe has a ways to go before it recovers from its recession, especially Switzerland, which is levered to European financials.

From a monetary standpoint the SNB has run out of room to cut interest rates, and deflationary pressure is a real concern. Swiss CPI declined 0.4% in March Y/Y, the biggest decline since 1959. Economists predicted a drop of 0.1% after a 0.2% gain in February.

While deflated prices (led by a y/y drop in oil costs) will benefit consumers in the short term, unemployment is rising and a weaker Franc will put downward pressure on wages and increase the price of imports. Cooling prices may have the opposite intended effect and prolong the recession, especially if consumers pull back spending and increase personal savings or wait for lower prices, a trend we’re seeing throughout Europe. The economy is forecast to contract as much as 3.5% this year and the SNB expects inflation to remain close to zero in 2010 and 2011. This is a bearish forecast for recovery in the intermediate term.

See the chart below - the Swiss eft EWL is heavily concentrated in healthcare (36.33%), consumer staples (22.47%), and financials (17.18%), sectors we’re bearish on. Our Healthcare analyst Tom Tobin is decidedly bearish on Swiss healthcare companies (Roche and Novartis each make up 13.5% of the etf) because they sell primary to the Europe, where profit margins are heavily reduced due to fixed pricing. Nestle makes up 20.2% of consumer staples. We’re bearish US Financials and believe European Financials will lag the US’s recovery by at least 3 Months. Again, Switzerland is heavily levered to financials and EWL’s financial composition includes: Credit Suisse 4.9%; UBS 4.4%; and Zurich Financial 4.2%.

The country’s negative fundamentals coupled with the weighting of the etf in underperforming sectors leaves us confident in our bearish thesis despite the intermediate gains that might result from the central bank’s devaluation of the Franc.

Matthew Hedrick

Analyst