The much heralded 11th hour solution to the fiscal cliff really does very little other than kick the can down the road. While on one hand, a permanent fix of the Bush Tax Cuts for those making less than $400K, an extension of Unemployment and Extended Benefits and a two month stay on cuts to federal discretionary outlays under sequestration are supportive of growth in the very near-term. Longer term, the Expiration of the 2% payroll tax deduction, higher capital gains and marginal tax rates on those earning >$400K, and the 3.8% tax increase on investment income legislated under ACA will still serve as a drag on growth, probably to the tune of ~1%.

Notably, the larger goal of enacting structural policy reforms necessary for driving fiscal sustainability once again went unmet. The half-measures and patchwork policy enacted as part of the 11th hour accord simply perpetuate the fiscal policy uncertainty that has predominated for the better part of the last few years and served as a negative influence on corporate hiring and capital investment decisions. Both the debt ceiling issue and a larger agreement over a sequestration alternative remain uresolved and will both come to a head on March 1st. So similar to last year, we can again look forward to a re-crescendo in congressional discord, brinksmanship and last minute “heroics” over the next couple months.

Below we highlight the main provisions from the American Taxpayer Relief Act of 2012 (ATRA 2012), or the fiscal cliff agreement. The facts of the accord have been fully discussed elsewhere but we would highlight a number of the key dates and prospective growth impacts of the deal:

Summary of Main ATRA Provisions:

- Tax Rates: Permanent extension of current income tax rates for all incomes below $400K. Marginal Tax rates increase to 39.6% from 35% for individuals making over $400K and couples making over $450K

- AMT: Permanently patched.

- Unemployment Benefits: extended for another year – expected 2Y cost of ~$30B

- Payroll Tax Holiday: The 2% payroll tax holiday enacted in 2010 as a stimulus measure expired for all workers.

- Capital Gains: Capital gains & dividends would be taxed at 20% for those earning over 400K. Those earning <$400K continue to pay current rate of 15% on LT gains.

- Health Law Capital Gains Tax: ATRA does not change the slated 3.8% tax on investment income imposed by ACA for individuals making $200K or couples making $250K

- Sequestration: Provides a stay of 2 months before legislated cuts again take effect.

- Extenders: Some 100 general, individual, Business, Energy & Health related (tax) provisions were passed as part of ATRA 2012. Some represent permanent fixes but most are 1Y extensions that will need to be re-addressed come year end 2013.

As is outlined in the table below, the impact of the ATRA is decidedly negative on the long run deficit. According to the CBO’s projections, ATRA will lead to a net increase in the deficit of $3.9 trillion through 2022. So much for fiscal reform.

KEY DATES & IMPACTS

Growth Impact - CBO Analysis: Late Friday afternoon, the CBO released a follow-on analysis of the expected impacts of the ATRA legislation as enacted (Here). According to the CBO’s analysis, while the fiscal cliff deal had the net effect of reducing the magnitude of fiscal tightening by 1.5 – 1.75%, the “components of tightening that are still in place and that we estimated will damp GDP growth in 2013 by roughly 1¼ percentage point.”

Payroll Tax Holiday Impact: The CBO estimated the combined impact of extending the payroll tax reduction and the Emergency Unemployment benefits at ~$108B for 2013 (Here, p. 7, Table 1.). Separately, the CBO’s final scoring of the ATRA estimated the cost of extending Emergency Unemployment Benefits at ~$22.4B in 2013, implying an ~$86B drag from the 2% increase in payroll taxes in 2013. This $86B along with the net impact from the 3.8% tax increase on investment income legislated under ACA and reduced consumption stemming from higher capital gains and marginal tax rates on those earning >$400K comprise the principal direct drag to growth for 2013.

Sequestration: Sequestration, the across the board reductions to Federal Discretionary Outlays as legislated under the Budget Control Act (BCA), were given a two month stay. The cuts will take effect beginning March 1st if congress does not reach an agreement on an alternative route for fiscal consolidation.

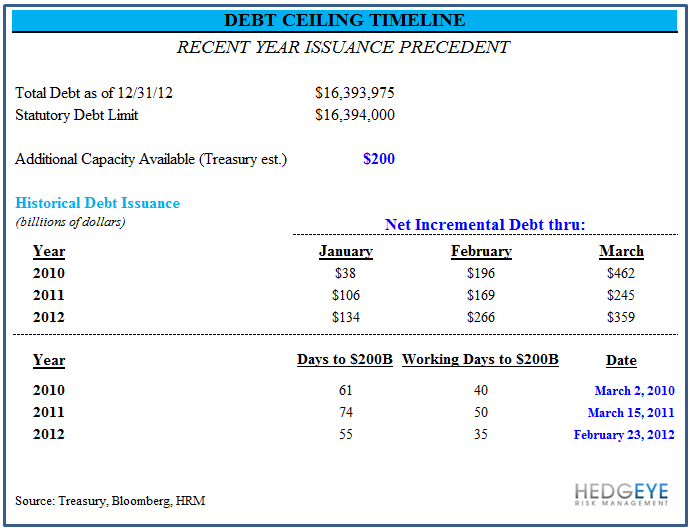

The DEBT CEILING: ATRA carries no explicit provisions related to the Debt Ceiling and no discernable progress was made towards reaching a bipartisan resolution on the issue. The Treasury has estimated they have enough accounting maneuverability to extend the debt ceiling timeline for approximately two months. Geithner provided a hard dollar estimate of $200B in available capacity. Assuming similar funding requirements, the mid-point of the issuance precedent over the last three years would suggest we have until ~March 1st to reach a debt ceiling accord. Note that this march 1st date corresponds with the march 1st deadline date for reaching a deal on a sequestration alternative.

Bottom Line: By delaying the implementation of sequestration cuts and permanently fixing lower tax rates for all those earning less than $400K, we avoided the full brunt of the fiscal cliff to the start the year. However, outside of the tax rate fix we made no substantial progress towards solving the larger outstanding budget issues or in bridging the Dem-GOP divide over spending, Entitlement reform, or large scale Tax Code reformation. By simply extending tens of general, individual, & business tax provisions - amounting to hundreds of billions of dollars (you can find the itemized cost, estimated by the Joint Committee on Taxation, for the extension of each tax provision Here) - for one year, we managed yet another can kick and ensured ourselves yet another replay of the same debate come year-end 2013. The Debt Ceiling and impending cuts slated under BCA are part and parcel of the same issue of unsustainable profligacy at the federal level. These issues remain unresolved, will both come to head on March 1st, and ensure the policy uncertainty and political dynamics that characterized December 2013 and the summer months preceding resolution of Debt Ceiling 1.0 in 2011 will likely characterize February 2013 as well.

Investment Considerations: We got the relief rally, now what?

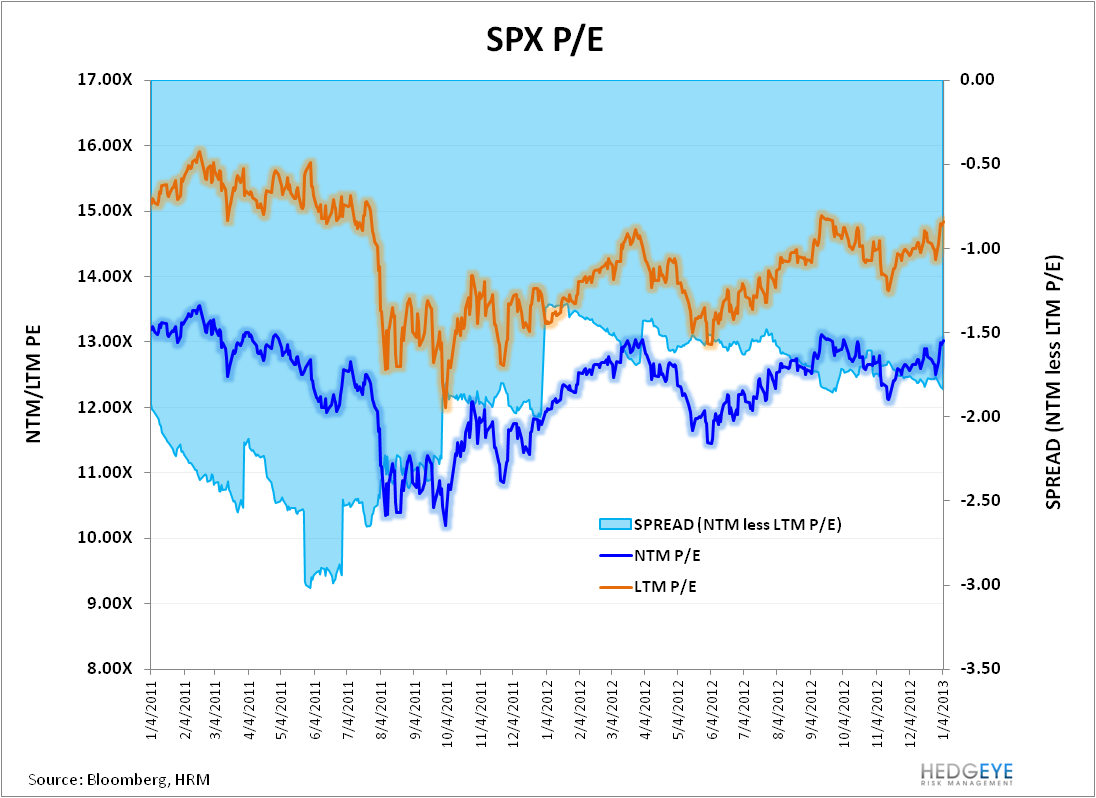

Outside of an expectation for a clean, non-draconian resolution, it’s hard to make a compelling case for being long the uncertainty of the Debt Ceiling event catalyst in isolation. We’ve already seen the post-event run-up, the SPX is trading at higher cycle highs, and forward multiples are near the top end of the multi-year range. Independent of the Debt Ceiling, however, global growth and price signals continue to support a bullish bias towards equities. Below are a number of the factors we’d like to continue to see trend positively for us to maintain our bullish tilt.

- Price Confirmation: SPX currently sits Bullish TRADE & Bullish TREND in the Hedgeye Quant model with TREND support down at 1419. With all nine sectors bullish and the SPX in Bullish Formation, price remains supportive of net long positioning in equities

- #GrowthStabilization: The slope of growth, activity, and employment measures across the EU & APAC regions continues to improve. From a price, the transition from growth slowing to growth stabilizing represents a buying opportunity within a positive growth inflection.

- Commodity Deflation: Energy and Commodity deflation represents a real-time tax cut for consumer’s, globally. A burning Yen, dissention among the ranks at the fed, Geithners departure, and some measure of American fiscal sobriety could all play positively for the dollar and, by extension, augur lower commodity prices for consumers and input costs for business.

- Housing & employment: Employment growth remains tepid but positive, jobless claims continue to track <385K level necessary for seeing tangible improvement in unemployment, and the positive, reflexive, price ßà demand dynamic continues to drive a parabolic recovery in housing.

- Asset Rotation: Bond yields have backed up, fund flows to bonds have slowed, and the major move in high yield is now likely rearview with the earnings yield in the SPX now running at a positive spread to the yield on high yield. If bond investors begin to sniff out 6+% unemployment and look to front run Bernanke, we could begin to see the rotation to equities panglossian stock bulls have been looking for for the past four years.

- Seasonal Adjustments: Seasonal Adjustments will remain a tailwind to the reported employment & economic data thru February.

- Growth Estimates: Consensus growth estimates for 2013 have tracked the data steadily lower over 2H12 and currently sit at 2% for full year 2013. While estimates may hold some further downside, a material drawdown in expectations from here may provide a favorable sentiment backdrop provided the above dynamics continue to trend positively.

Christian B. Drake

Senior Analyst