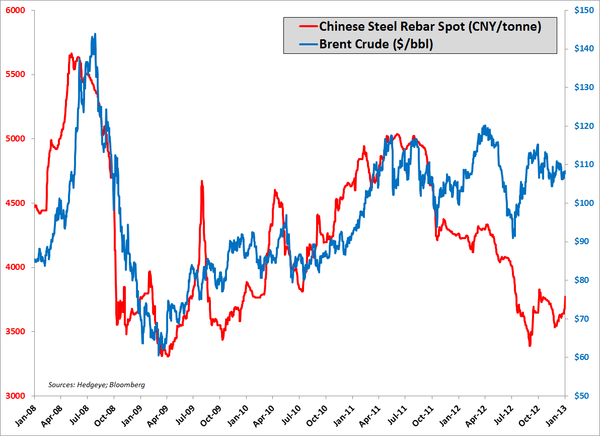

Here at Hedgeye, we like to observe the price of Chinese steel rebar. It’s a decent barometer of Chinese construction activity and subsequently, growth. The spot price for Chinese rebar jumped 3% day-over-day and is now back to the highest price since November. Combined with our macro team’s research that signals growth accelerating throughout Asia, rebar is another catalyst that shows that the growth slowing days are over.