TODAY’S S&P 500 SET-UP – January 7, 2013

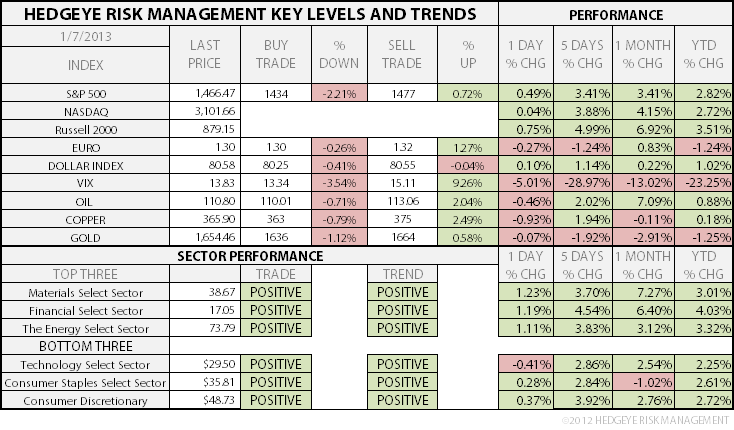

As we look at today's setup for the S&P 500, the range is 43 points or 2.21% downside to 1434 and 0.72% upside to 1477.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.63 from 1.64

- VIX closed at 13.83 1 day percent change of -5.01%

- BONDS – if Treasury yields backed off for real (below our TAIL risk line of 1.84%), we’d stop harping on this – but that’s not happening this morning; for the 1st time in a year fund flows are marginally tilting away from fixed income towards equities – maybe that’s a sign of a short-term equity market top; maybe it means we’ll keep making higher-highs; we don’t know – but its new.

MACRO DATA POINTS (Bloomberg Estimates):

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2042 sector

- 11:30am: U.S. to sell $32b 3M, $28b 6M bills

- U.S. Rates Weekly Agenda

GOVERNMENT:

- ITC to announce final decision in patent-infringement case by Vitec unit over television, movie-studio lighting, 5pm

WHAT TO WATCH

- Banks win watered-down liquidity rule after Basel Grp deal

- Celgene, Onyx, others to give updates at JPMorgan conf.

- Citigroup said to seek stock buybacks in capital plan: WSJ

- Sikorsky poised to win $6.8b U.S. helicoper contract

- Hulu CEO Jason Kilar says he plans to leave co. by April

- Google patent offers probably won’t end Microsoft, Apple suits

- Nvidia unveils Tegra 4 mobile processor to spur smartphone push

- Cerberus plans to sell most of Aozora stake valued at $1.7b

- Flowers Foods, Bimbo said bidding for Hostess Brands: WSJ

- Terra Firma to sell Odeon theater chain: FT

- Sony, BMG to bid for Parlophone, other EMI labels: FT

- Deal in foreclosure case may come as early as today: NYT

- US Air pilot leaders back interim labor deal on AMR merger

- “Texas Chainsaw” in #1 at wknd box office, “Django” #2

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Real Estate, Transports

- Canada Weekly Agendas: Energy, Mining

- ECB, China Trade, Chavez, Oscar Noms: Week Ahead Jan. 5-12

EARNINGS:

- Commercial Metals (CMC) 8am, $0.17

- Team (TISI) 4:01pm, $0.60

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – they tried to bounce it into Friday’s close, then again this morning – failed at both our TRADE and TREND lines of resistance; watching that TAIL line of $1671 closely as the downside gap opens up in our model (ie lower intermediate-term lows are signaling as probable).

- Oil Declines a Third Day; Morgan Stanley Sees Supply Recovery

- Bulls Add to Wagers for First Time Since November: Commodities

- LBMA’s Best Gold Forecaster Hochreiter Says Bull Market Is Over

- Gold Swings Between Gains and Drops in London on Stronger Dollar

- Copper Falls as Report May Show Weaker German Factory Orders

- Asia Naphtha Crack Rebounds; BP Sells Gasoil, Fuel: Oil Products

- Sugar, Coffee Gain in New York on Index Rebalancing; Cocoa Rises

- Hedge Funds Raise Brent Crude Net-Longs to Nine-Month High

- U.K. Natural Gas Jumps Most Since August as Statoil Cuts Output

- Shell Leads S. Africa on Record Oil Rush as Coal Falters: Energy

- Iron Ore-Import Wave Seen by Morgan Stanley Boosting Shipping

- European Oil Demand Outside CIS Declines Along With Production

- U.S. Corn, Soy Reserves on Dec. 1 Seen Dropping to Nine-Year Low

- Corn Climbs From Six-Month Low as Rains Threaten Argentine Crop

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

TAIWAN – never mind growth stabilizing, Taiwanese export growth just accelerated, big time, from 0.9% NOV to +9.0% in DEC on Chinese demand; mostly every Asian market (equities, bonds, FX) is signaling the same thing that it has for a month; growth isn’t slowing anymore – couldn’t have said that 6 months ago.

MIDDLE EAST

The Hedgeye Macro Team