Here is some more detail on the final December numbers from Macau:

Y-O-Y TABLE OBSERVATIONS

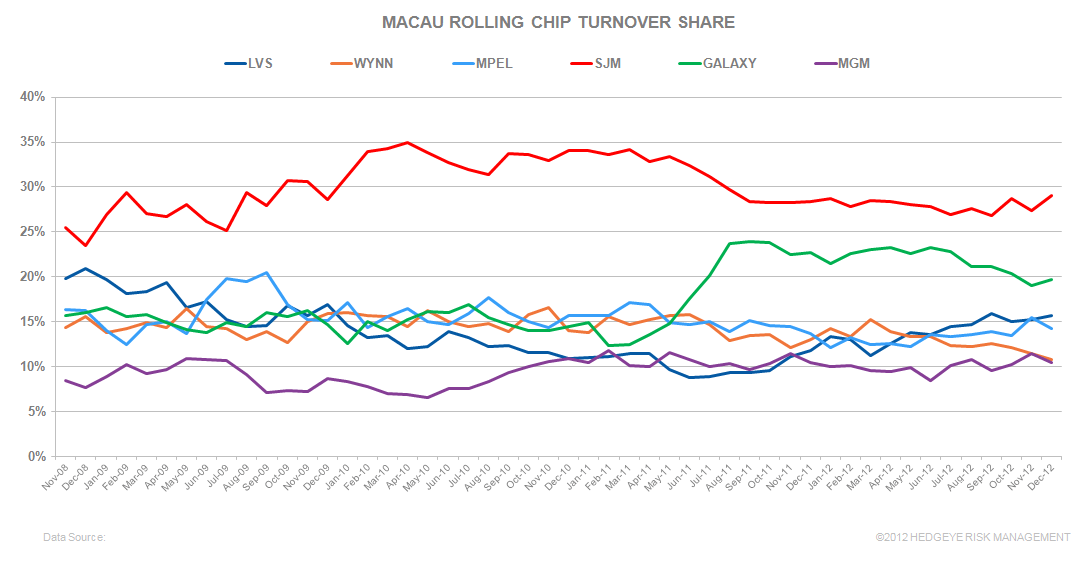

Total table revenues grew 21% in December. Mass revenue growth was strong at 32%, just a little above the 6-month trailing average of 31%. VIP revenues grew 16% - the best growth in 9 months. Junket RC volume grew 9% YoY. We expect that January’s growth rate will slow to 7-12% growth, due to the smoking restrictions and unfavorable calendary.

LVS

Table revenues grew 52% YoY (Mass +48%; VIP+55%), garnering the best growth in the market for the 6th straight month. We estimate that Sands China held at 3.14% vs 2.86% last year, adjusted for direct play of 19%.

- Sands table revenue fell 9% YoY, aided by high hold but hurt by an even tough comparison.

- Mass grew 12%

- VIP was down 20%. We estimate that Sands held at 3.70% in December compared to 4.01% in the same period last year. We assume 9% direct play in December vs 11% in December 2011.

- Junket RC declined 11% YoY, aside from September; 12 of the 13 trailing months have seen YoY declines in RC volume.

- Venetian table grew 19% YoY, negatively impacted by low hold but offset by an easy comparison.

- Mass increased 15%

- VIP was grew 24%

- Junket VIP RC increased 14%, breaking 10th consecutive months of declines at Venetian

- Assuming 30% direct play, hold was 2.70% compared to 2.59% in December 2011, assuming 27% direct play (in-line with 4Q11)

- Four Seasons continued to perform well, growing 43% YoY, driven by high hold and an easy comparison

- Mass revenues were flat YoY

- VIP grew 52% and Junket VIP RC rose 16% YoY

- If we assume direct play of 16%, in-line with the first 3Q of 2012, hold in December was 3.19% vs. 2.42% in December 2011 when direct play was ~16%

- Sands Cotai Central produced $169MM in December

- Mass revenue of $62MM, $1MM lower MoM

- VIP revenue of $107MM

- Junket RC volume of $2.83 BN, up 2% MoM

- If we assume that direct play was 9%, hold would have been 3.46%

WYNN

Wynn table revenues fell 10% YoY in December. Hold was high but last year’s comparison was more difficult.

- Mass was up 4% YoY– the worst performance of the 6 concessionaires for the 4th consecutive month

- Wynn was the only concessionaire to record a decline in VIP revenues this month, which fell 13%. With the exception of September, Wynn has had YoY declines in VIP revenues for the last 8 of 9 months.

- Junket RC fell 9%, the worst performance of the group. Aside from a 1% gain in November, 7 of the last 8 consecutive months have been in the red.

- Assuming 10% of total VIP play was direct (in-line with 3Q12), we estimate that hold was 3.10% compared to 3.21% last year (assuming 11% direct play – in-line with 4Q11).

MPEL

MPEL table revenue grew 14%, negatively impacted by low hold and a difficult YoY comparison. Hold across MPEL’s two properties was 2.84% vs. 3.16% last year.

- Altira revenues grew 11%, with a 21% increase in Mass and a 10% increase in VIP

- VIP RC increased 13%, breaking its 12th month consecutive streak of losses

- We estimate that hold was 3.11%, compared to 3.30% in the prior year

- CoD table revenues grew 15% YoY, despite low hold

- Mass revenue grew an impressive 62%, offset by a 2% drop in VIP revenue

- RC grew 13%

- Assuming a 15% direct play level, hold was 2.70% in December compared to 3.08% last year (assuming 16% direct play)

SJM

Table revenue grew 20%

- Mass revenue was up 9% and VIP revenue grew 25%

- Junket RC grew 12%

- Hold was 3.03%, compared with 2.70% last December

GALAXY

Galaxy table revenues grew 14%. Mass growth took the top spot with 59% growth. VIP revenues only grew 3%YoY, despite high hold. Across its two owned properties, Galaxy held at 3.39% vs. 3.04% in December 2011.

- StarWorld table revenues fell 2%, marking the 7thconsecutive month of declines

- Mass grew 57%, offset by a 9% drop in VIP

- Junket RC fell 11%, marking the 7th month of consecutive declines

- Hold was normal at 2.84% vs. an easy comparison of 2.76% last December

- Galaxy Macau's table revenues grew 33%

- Mass grew 63%

- VIP grew 25%, while RC grew 8%, breaking a 4 consecutive month streak of declines

- Hold was high in December at 3.86% vs. 3.34% last year

MGM

MGM table revenue grew 38% in December, aided by high hold.

- Mass revenue grew 51%

- VIP revenue grew 35% on a 10% increase in VIP RC.

- If direct play was 8%, then December hold was 3.55% compared to 2.90% last year

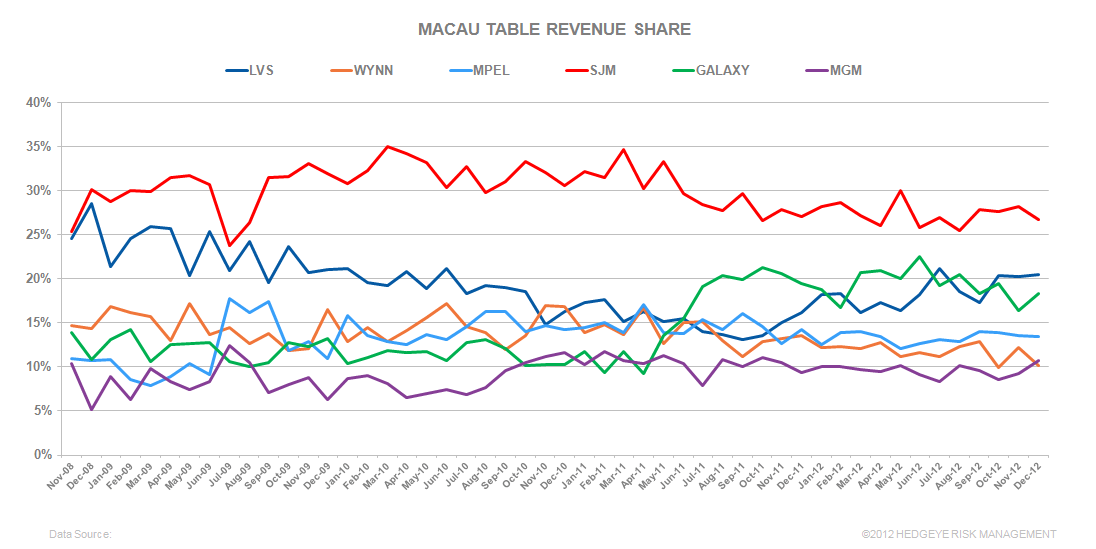

SEQUENTIAL MARKET SHARE

LVS

LVS’s MoM share increased 20bps to 21.0%. December’s share was better than its 6 month trailing market share of 20.2% and better than Sands’ 2011 average share of 15.7%.

- Sands' share was flat at 3.7%. For comparison purposes, 2011 share was 4.6% and 6M trailing average share was 3.8%.

- Mass share ticked down to 5.3%

- VIP rev share was flat at 3.0%

- RC share was 2.4%, down 10bps MoM

- Venetian’s share ticked up 10bps to 8.0%. 2011 share was 8.4% and 6 month trailing share was 8.1%.

- Mass share fell 40bps to 13.1%

- VIP share increased 30bps to 5.9%

- Junket RC share increased 1% to 5.1%

- FS was flat at 3.7%. This compares to 2011 share of 2.2% and 6M trailing average share of 3.2%.

- VIP ticked up 10bps to 4.6%.

- Mass share fell 30bps to 1.6%

- Junket RC fell 40bps to 4.1%

- Sands Cotai Central's table market share ticked up 10bps to 5.0% and compares to the 6M trailing average share of 4.5%.

- Mass share of 6.2%

- VIP share of 4.5%

- Junket RC share ticked down 10bps to 4.0%

WYNN

Wynn was the biggest share donor in December, losing 1.8% to 10.3% in December. Wynn’s 2011 share averaged 14.1% and their 6-month trailing share averaged 11.5%.

- Mass market share increased 50bps to 8.0%, an all-time property low

- VIP market share plunged 3.1% to 11.1%

- Junket RC share decreased 70bps to 10.7%, the lowest level since October 2007

MPEL

MPEL’s lost 20bps of share in December to 13.5%, below their 6 month trailing share of 13.7% and their 2011 share of 14.8%.

- Altira’s share fell 10bps to 4.0%, above its 6M trailing share of 3.9% but below their 2011 share of 5.3%.

- Mass share ticked up 10bps to 1.4%

- VIP fell 20bps to 5.1%

- VIP RC share fell 20bps to 5.2%

- CoD’s share fell 10bps to 9.4%. December’s share was above the property’s 2011 and in-line with 6M trailing share of 9.3% and 9.5%, respectively.

- Mass market share was flat 11.7%, in-line with an all-time high for the property set in November

- VIP share was flat at 8.5%

- Junket share fell 90bps to 9.0%

SJM

SJM’s share fell 1.5% to 26.1%. December’s share compares to their 2011 average of 29.2% and its 6M trailing average of 26.5%.

- Mass market share fell 1.6% to 28.7%, an all-time company low

- VIP share dropped 1.4%to 26.0%

- Junket RC share increased 1.6% to 29.0%

GALAXY

Galaxy was the largest share gainer in December, increased 2% points to 18.2%, below its 6M trailing share average of 18.5%

- Galaxy Macau share increased 2.5% to 11.0%, positively impacted by 3.86% and an easy comparison in November

- Mass share increased 70bps to 9.8%

- VIP share increased 3.3% to 11.5%

- RC share grew 60bps to 10.2%, reversing 6 consecutive months of share declines

- Starworld share fell 30bps to 6.2%

- Mass share increased 90bps to 3.5%

- VIP share fell 90bps to 7.3%

- RC share increased 10bps to 8.7%

MGM

MGM gained 1.3% share to 10.9% in December, above their 6M average of 9.7% and above their 2011 share of 10.5%.

- Mass share increased 1.2% to 8.1%

- VIP share grew 1.6% to 11.9%

- Junket RC fell 90bps to 10.5%

Slot Revenue

Slot revenue grew 7% YoY to $145MM in December.

- LVS took the top prize for YoY growth of 49% to $49MM

- Galaxy’s slot revenue grew 26% to $19MM, also setting a company record

- MPEL grew 3% YoY to $24MM

- MGM slot revenues fell 8% to $20MM

- WYNN fell 18% to $19MM

- SJM had the worst YoY performance in slots with a 29% YoY decline to $14MM