TODAY’S S&P 500 SET-UP – January 4, 2013

As we look at today's setup for the S&P 500, the range is 42 points or 1.88% downside to 1432 and 1.00% upside to 1474.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.67 from 1.65

- VIX closed at 14.56 1 day percent change of -0.82%

- BONDS – massive 3wk move in Treasuries and now Bond Yields are in a Bullish Formation (bullish TRADE, TREND, TAIL) now that they took out my 1.85% TAIL risk line (1.96% last); no intermediate-term resistance in the 10yr to 2.4% and our asset allocation to Fixed Income remains 0%.

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Nonfarm Payrolls, Dec., est. 153k (prior 146k)

- 8:30am: Unemployment Rate, Dec., est. 7.7% (prior 7.7%)

- 10am: Factory Orders, Nov., est. 0.4% (prior 0.8%)

- 10am: ISM Non-Manf. Composite, Dec., est. 54.0 (prior 54.7)

- 10:30am: EIA natgas storage

- 11am: DoE weekly inventories

- 1pm: Baker Hughes U.S. rig count

- 1:15pm: Plosser speaks in San Diego on real business cycles

- 1:30pm: Lacker speaks in Baltimore on economic outlook

- 3:30pm: Yellen speaks in San Diego on systemic risk

- 5:30pm: Bullard speaks to economists in San Diego

GOVERNMENT:

- House, Senate meet to count electoral votes for president

- House to vote on $9.7b for national flood insurance program

- CFTC holds closed meeting on enforcement matters, 10am

WHAT TO WATCH

- Payrolls in U.S. probably held gains in Dec. as economy grew

- JPMorgan faces sanction for refusing to provide Madoff docs

- Abbott, J&J, Sanofi said to show interest in Bausch & Lomb bid

- Moody’s, S&P, Fitch must face fraud claims in Rhinebridge suit

- Cohen’s SAC fund tops most-profitable list amid insider probes

- Berkshire ex-executive Sokol won’t face SEC action, lawyer says

- Wal-Mart creates new role to oversee alternative format stores

- Facebook testing free calling on message app: L.A. Times

- Best Buy, Toys R Us say Wal-Mart misleading in ads: WSJ

- Euro-area manufacturing, services shrink more than estimated

- Euro-area Dec. consumer prices rise 2.2% in yr, est. 2.1%

- IBM insider case analyst agrees to U.S. return, court told

- ECB, China Trade, Chavez, Oscar Nominees: Wk Ahead Jan. 5-12

EARNINGS:

- Finish Line (FINL) 6:45am, $0.10

- Mosaic (MOS) 7am, $0.88, preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

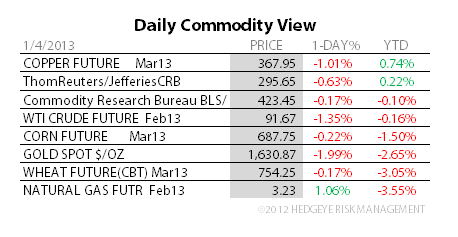

GOLD – getting plastered this morning, down another -2% (Silver down -5%) as the world comes to realize that there are many unintended consequences associates w/ A) #GrowthStabilizing and B) Bernanke’s experiment in unemployment targeting; if this jobs picture continues to improve, we think Gold continues lower – oversold here today.

- Oil Declines for a Second Day as Fed Discusses Curbing Stimulus

- Gold Seen Rallying From Worst Streak in Eight Years: Commodities

- Copper Declines Most in Two Weeks as Fed Signals Stimulus End

- Soybeans Rebound on Speculation Demand May Rise Following Slump

- Gold Set for Worst Run Since 2004 as Fed Sees End to Purchases

- Sugar Falls to Two-Week Low on Surplus; Coffee and Cocoa Slide

- SHFE Metal Stockpiles Expand as Copper Rises to Eight-Month High

- West African Cocoa Premiums Said to Drop on Better Crop Outlook

- Palm Oil Advances as Malaysian Shipments May Gain on Tax Revamp

- Uranium Rebound Seen as Japan Considers Nuclear: Energy Markets

- Mississippi Seen Navigable Through Jan. 26 After Rock Removal

- Oil May Increase as Economic Growth Spurs Demand, Survey Shows

- Gold May Drop to $1,600 on Moving Averages: Technical Analysis

- Rebar Advances to Five-Month High as Demand Increases in China

CURRENCIES

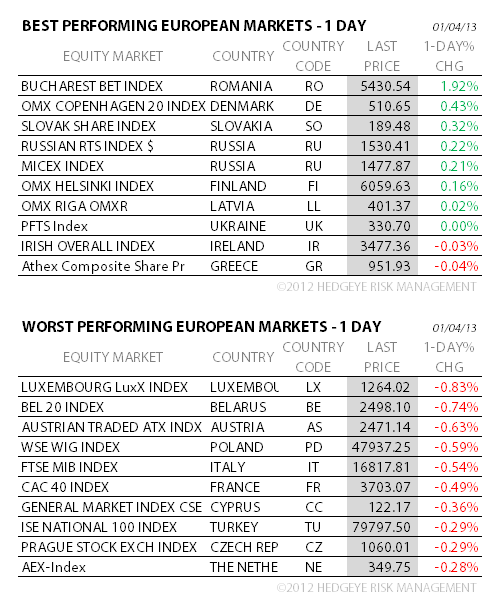

EUROPEAN MARKETS

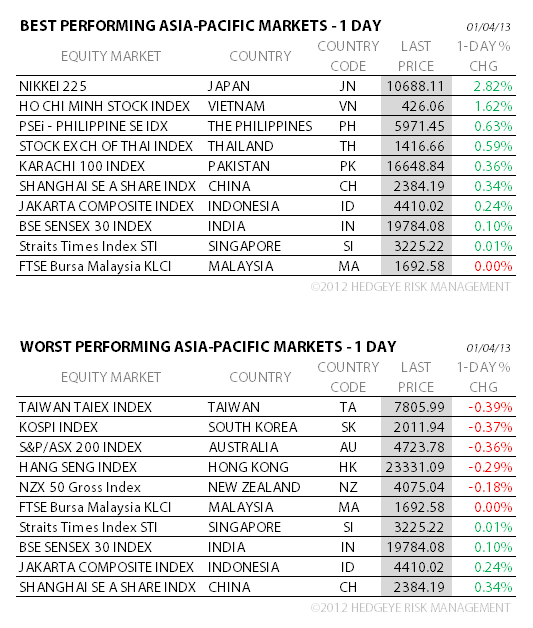

ASIAN MARKETS

JAPAN – in what might be the end of Keynesian policy “experimentation” gone gnarly, the Japanese are literally torching their currency at this pt (Yen down another -1.1% this morn) and the Nikkei is going Weimar style republic (+25.2% since mid OCT!); all the while, Japanese economic growth is one of the few majors in the world still slowing – this should end well.

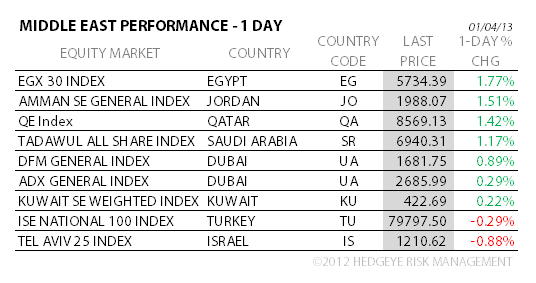

MIDDLE EAST

The Hedgeye Macro Team