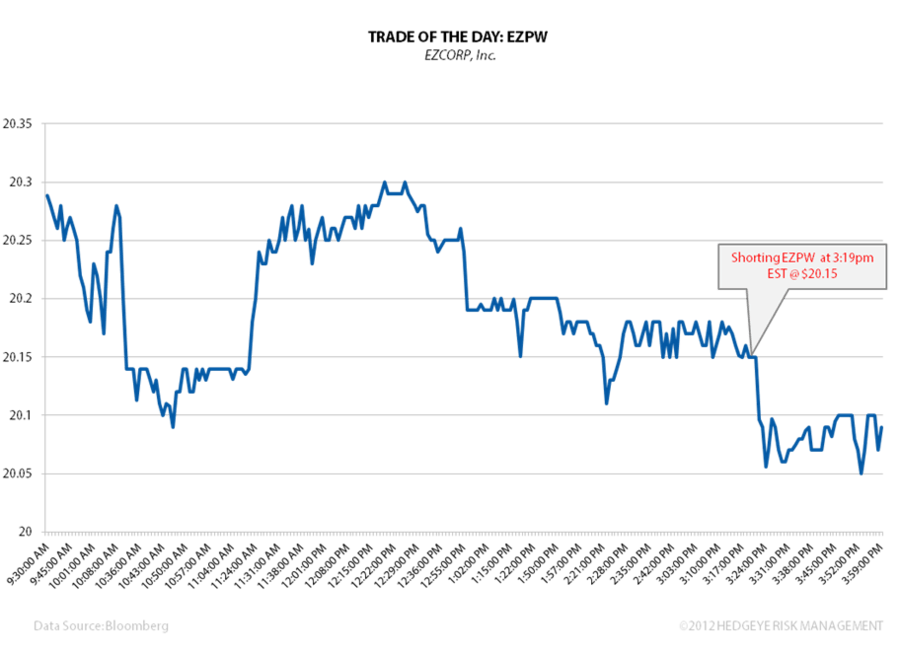

Today we shorted EZ CORP (EZPW) at $20.15 a share at 3:19 PM EDT in our Real-Time Alerts. Along with Cash America (CSH), EZ CORP will be one of the pawn shop operators affected by gold’s recent downturn. When gold falls, it takes pawns down with it. We remain bearish on the stock through Q1 2013.