TODAY’S S&P 500 SET-UP – January 3, 2013

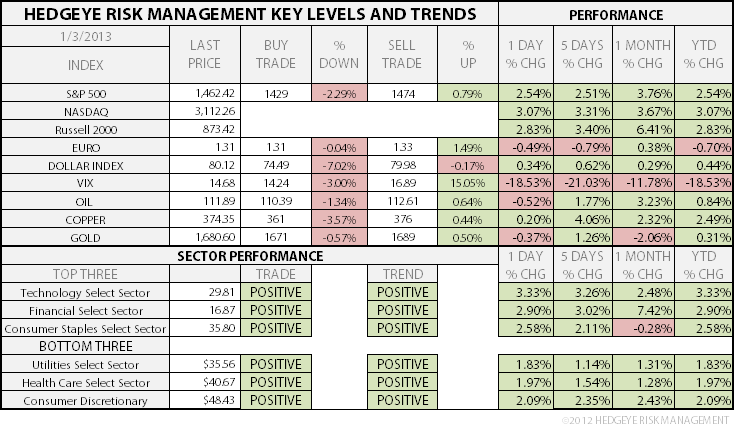

As we look at today's setup for the S&P 500, the range is 45 points or 2.29% downside to 1429 and 0.79% upside to 1474.

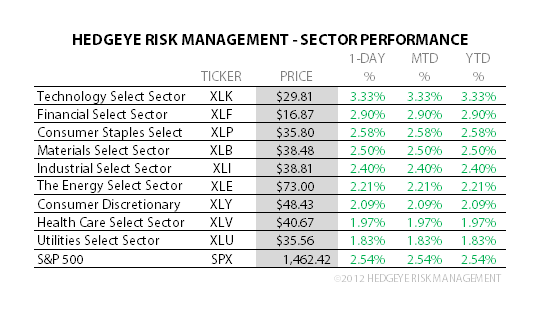

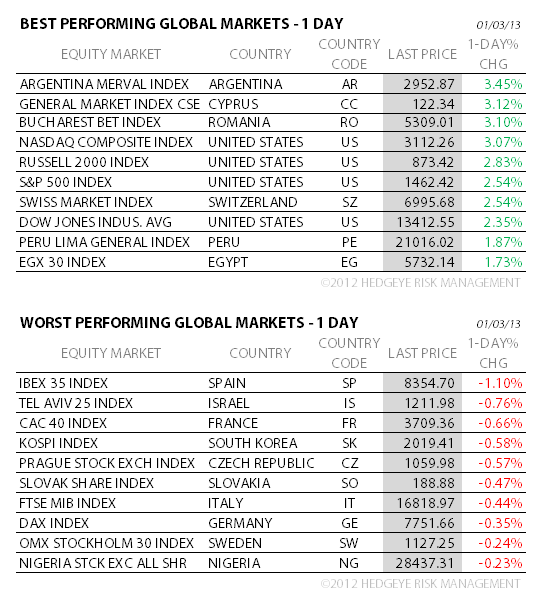

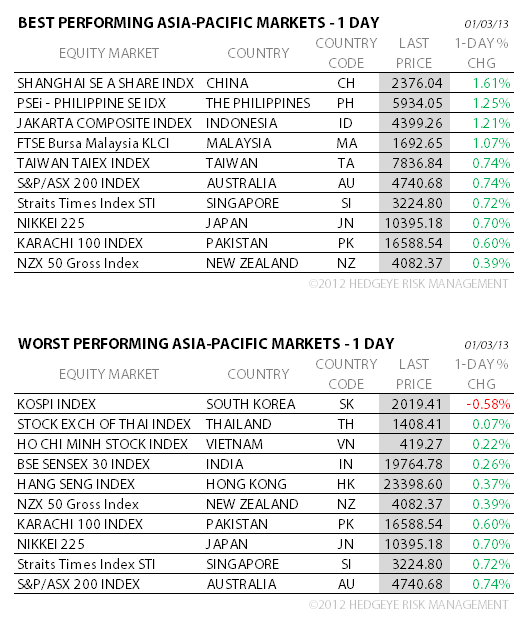

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.58 from 1.58

- VIX closed at 14.68 1 day percent change of -18.53%

- ECONOMIC DATA – the 3 big engines for Global #GrowthStabilizing (China, Germany, USA) all better sequentially in the last 24hrs (US PMI 50.7 DEC vs 49.5 NOV, w/ a very good employment reading within that report of 52.7; German unemployment 6.9% was solid; and Chinese non-manufacturing PMI of 56.1 DEC vs 55.6 NOV hit a 4mth high).

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, week of Dec. 28

- 7:30am: Challenger Job Cuts, Y/y, Dec., (prior 34.4%)

- 8:00am: RBC Consumer Outlook, Jan. (prior 46.9)

- 8:15am: ADP Employment Change, Dec., est. 140k (prior 118k)

- 8:30am: Initial Jobless Claims, wk of Dec. 29, est. 360k (prior 350k)

- 9:45am: Bloomberg Consumer Comfort, wk of Dec. 30 (prior -32.1)

- 9:45am: ISM New York, Dec. (prior 52.5)

- 10am: Freddie Mac mortgage rate survey

- 2pm: Fed releases minutes from Dec. 11-12 FOMC meeting

- 4:30pm: API weekly inventories

- U.S. Treasury to announce 1Y, 3Y, 10Y, 30Y auction sizes

GOVERNMENT:

- Congress convenes; almost 100 members will be sworn in to office for the first time

- Centers for Medicare & Medicaid Services holds a conference call briefing on an announcement related to the Affordable Care Act, 1:30pm

- American Bankers Association announces the release of the third quarter 2012 Consumer Credit Delinquency Bulletin, containing delinquency data for several consumer loan categories, 4pm

WHAT TO WATCH

- Google said to be set to end FTC antitrust probe with agreement today

- Boehner set to regain speakership as party base decries tax vote

- Sandy aid will get vote this month following delay, Boehner says

- Retailers may post slowest Dec. sales growth since 2008

- Ford, GM, other automakers release December sales

- Barnes & Noble releases holiday sales, Nook update

- AMR asks bankruptcy judge to approve revised supplier contracts

- China service industries expanded at fastest pace in 4 mos. in Dec.

- Paulson & Co. named as defendant in amended ACA Goldman Sachs lawsuit

- Al Gore’s Current TV is said to be sold for $500m to Al Jazeera

- Rambus barred from enforcing 12 chip patents in Micron lawsuit

- Amgen whistle-blower blocked from challenging Aranesp settlement

- Safeway CEO Burd to retire after 20 yrs

EARNINGS:

- Family Dollar (FDO) 7am, $0.75

- UniFirst (UNF) 8am, $1.33

- Worthington Industries (WOR) 8:30am, $0.41

- Progress Software (PRGS) 4:30pm, $0.34

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – both bonds and gold do not like growth improving; that’s why both lagged yesterday and don’t look any better today (10yr 1.83% and Gold fails at $1690 TRADE line resistance); Gold snapping its long-term TAIL line again of $1671 is when you get paid there on the short side. A better employment rpt could easily do that.

- Oil Drops From Highest in Three Months on Signs Gains Excessive

- Dust Bowl Wilting U.S. Wheat as Funds Turn Bearish: Commodities

- Gold Declines on U.S. Budget-Deal ‘Hangover’ as Dollar Rallies

- Copper Advances on Prospects for an Economic Rebound in China

- Soybeans Drop as Prospects Improve for South American Crops

- Australia Swelters Amid Most Wide-Ranging Heatwave Since 2001

- Gold Seen Sliding to $1,450 in 2013 on Investor Frustration

- Natural Gas 4Q Price Gains Boost Producers, Challenge Suppliers

- Coal’s Competitive Fuel Cost Advantage Over Gas Grows in 4Q

- Chavez Cancer Imperils $7 Billion Caribbean Oil Funding: Energy

- Rig Grounding Revives Debate Over Shell’s Arctic Oil Exploration

- Asia Naphtha Crack Rebounds; Vitol Sells Gasoline: Oil Products

- European Union Carbon-Dioxide Permits Decline to One-Month Low

- Gold’s 12-Year Bull Market “Not Yet Dead,” Credit Suisse Says

CURRENCIES

EURO – biggest relative opportunity on the long-side potentially here this morning w/ EUR/USD moving to immediate-term TRADE oversold at $1.31 (risk range = 1.31-1.33). At a bare minimum, if you are short it, you cover here – we might buy it (which is just one more bullish signal for global macro beta right now). Haven’t bought the Euro in a while.

EUROPEAN MARKETS

ASIAN MARKETS

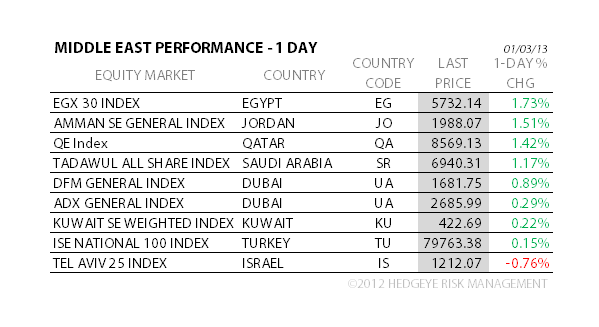

MIDDLE EAST

The Hedgeye Macro Team