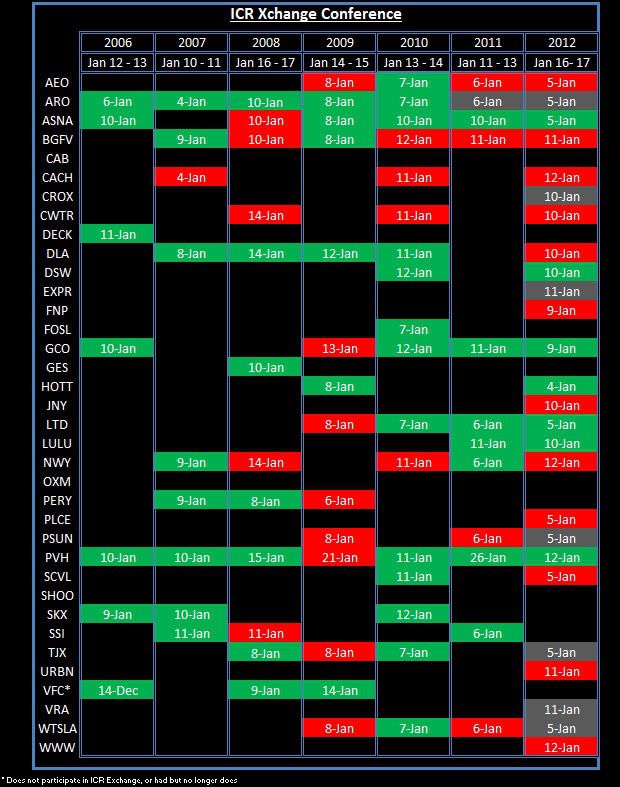

With the turn of the New Year so to comes ‘Pre-announcement Season’ with Sales Day and the annual ICR XChange conference set to take place over the next two-weeks – tomorrow and January 16-17th respectively. Historical context provides an interesting picture and precedent of pre-announcements over this period. As such, we’ve updated our pre-announcement scoreboard reflecting the more notable retail companies that will be present in Miami.

Companies that have issued positive releases are highlighted in green while those with less positive news are highlighted in red and reaffirmations of prior outlooks in grey. It’s worth noting that last year marked a significant increase in the number of pre-announcements from the sample set below jumping to 26 compared to a typical range of 12-18 between 2008-2011. The incremental delta came primarily from companies not participating in Sales Day more than doubling to 16 compared to ~7.5 on average during the prior four years. We expect this year’s pre-announcement activity like last year to be at least as active as we’ve seen in recent years.

If history is any indication, PVH, GCO, NWY, BGFV, and ASNA are most likely to pre-announce results over the next two weeks. The following are the only companies to never issue guidance: CAB, OXM, SHOO.

Other notable new additions and departures relative to last year’s ICR schedule include the additions of KORS, TUMI, TJX, and exclusions of FINL, BWS, SKX, MW.