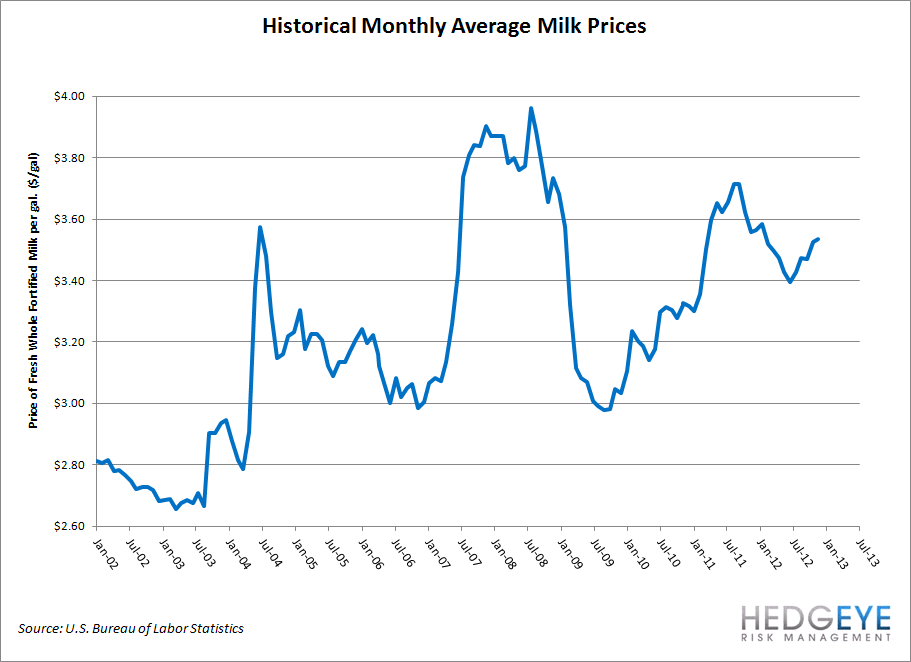

What do milk and the fiscal cliff have in common? Quite a bit, actually. As it stands, our government sets a minimum price for milk creating a floor. This helps milk producers in their financial planning and the like. If Congress can’t come to an agreement over the fiscal cliff, the calculation mechanism for the minimum price will revert to a 1949 law that reflects milk production technology that is 6 decades obsolete, adjusted for inflation.

This new floor would be about twice as much as the current market price. With a gallon of milk costing around $3.50 on average, consumers would see that double to $7 over time. That’s a meaningful impact to low income families and represents a total tax hike of $22.7 billion considering that per capita milk consumption is approximately 20.6 gallons per person per year. Retailers who rely on milk to drive store traffic will also feel the pain as well.