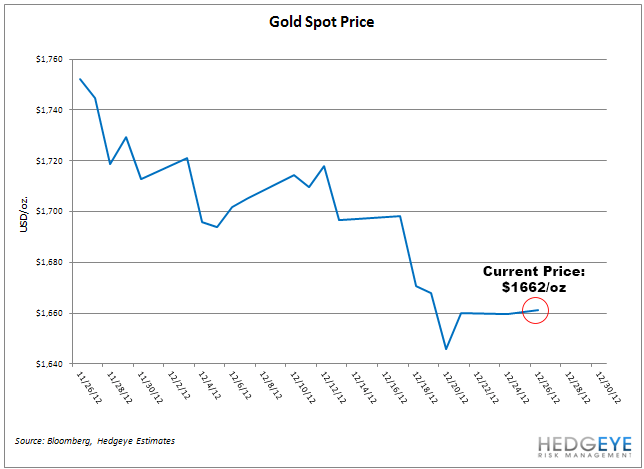

The great commodity super-cycle is in the process of turning and driving commodity prices down with it. As the American economy moves from "Growth Slowing" to "Growth Stabilizing," the artificial commodity bubble brought on by the policies of the Federal Reserve is now popping. Plenty of investors, from hedge funds to individuals, are long gold and it's beginning to really hurt. Gold snapped our long-term TAIL risk line of $1671 last week, which means the price is likely to continue falling until catching some kind of support. Gold is down nearly $100 over the last month alone and CFTC gold net long contracts are down -13% week-over-week as investors flee. This is what happens when you let Ben Bernanke take control of the wheel.