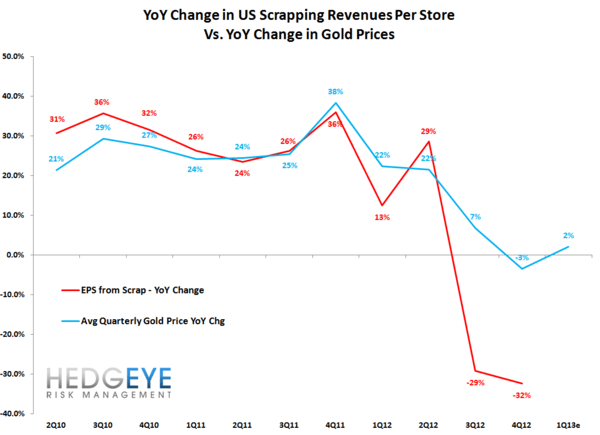

Pawn shops like EZ CORP (EZPW) are particularly sensitive to the price of gold. Think about how many people come in to pawn or sell gold jewelry or scrap it for cash. With the price of gold sinking week-after-week as the great commodity bubble deflates, pawns are getting hit. But it’s not just the price of gold that’s causing headaches for EZPW, it’s gold volumes. Since Q312, gold volumes have fallen off a cliff and have yet to recover. It’s a problem that will materially affect earnings going forward hence our short position on EZPW in our Real-Time Alerts. Another company that will bare the brunt of the decline in volumes is Cash America (CSH).