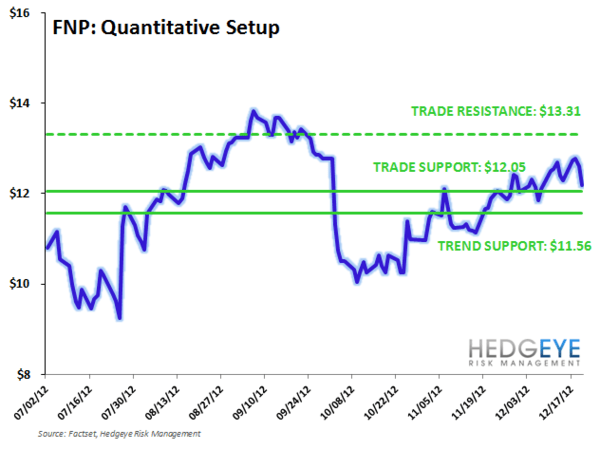

We added Fifth & Pacific (FNP) to our Real-Time Alerts this week as the quantitative setup clicked with our fundamental views on the stock. Our bullish stance comes from several factors, mainly that the stock has more unrealized value than many other names in retail. The Kate Spade brand is strong growth driver while Lucky Brand helps contribute to cash flow. While the Juicy Couture brand we view as a risk, we believe that FNP will soon get rid of the brand through a sale of some sort. We view 2013 as a good year for FNP and see upward revisions on the earnings side going forward.