“No one could remember when London had been so quiet.”

-Paul Reid

That’s what Paul Reid wrote about the French surrender to the Germans on June 22, 1940. It “staggered all of Britain. Britons began to realize that the way of life they had known and loved was vanishing.” (The Last Lion, pg 105)

And with the S&P Futures having a mini flash crash of -3.4% last night (1390 was the low) on the new “news” that our political overlords have no concept of real-time risk management, all was quiet.

Staggeringly quiet.

Back to the Global Macro Grind…

People who wake up every day begging for and/or getting paid by more Big Government Intervention in what were our free-markets have no business whining about this today. They want a deal? This is part of the deal. So deal with it.

While there’s no doubt some in the #PoliticalMedia panicked last night, maybe freaking out is the only thing left that will drive ratings off 8 year lows. Who knows. The Rest of Us just sat back and watched the #PoliticalClass self-implode.

Context in considering market risk is always critical. Understand that both Asian and European equity markets were immediate-term TRADE overbought to begin with, so I wouldn’t consider Asia’s closing prices overnight and/or how Europe is trading this morning anything to freak-out about.

ASIA:

- China (Shanghai Composite) only gave back -0.69% of its recent rip

- Japan (Nikkei) was down -1% after being up +17% in the last month

- Singapore and South Korea were down -0.38% and -0.95%, respectively

EUROPE:

- EuroStoxx50 is only down -0.59% this morning after going straight up since mid-November

- Germany (DAX) is -0.68% to 7619 (up +29.4% YTD and comfortably above its SEP 7451 closing high)

- Denmark (OMX Copenhagen) doesn’t care about any of this noise, UP +0.4% on the session

I know, who cares about Denmark? Let me assure you that the Danes don’t care about Captain Bailout America these days either. That’s the new world we are perpetuating – a very much polarized and protectionist one. Get used to it.

Global Fixed Income and Currency markets aren’t freaking-out like US Equity Futures traders either:

- US Treasury Yield (10yr) has literally moved 1 beep (basis point) in the last 24hrs (1.76% vs 1.77%)

- US Dollar Index is actually up +0.11% on the session to $79.37, making another higher long-term low

- EUR/USD only down 20 beeps to $1.32 showing no stress whatsoever

Spread risk and bond yields, globally, aren’t signaling much to me this morning; neither are commodities. Other than seeing a lot of bad jokes about Mayans on my Twitter stream, all I really see going on is a bunch of politically oriented people on TV looking emphatic on mute.

*Twitter and TV Viewer Note: when you are emphatic about everything, you emphasize nothing.

Where do we go from here?

You probably pick your favorite stock this morning and buy it on red. Don’t buy a Gold stock though. You’d think on an end-of-the-world morning like this Gold would actually go up. Nope.

Our intermediate-term strategy view remains the same as it has for the last month:

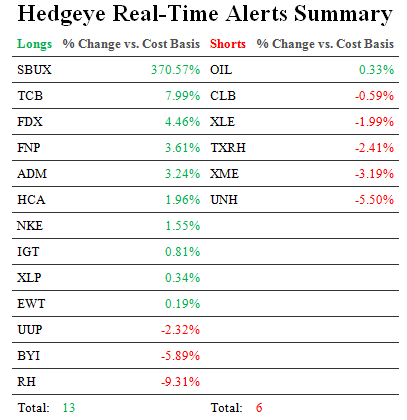

- Long Global Consumption Stocks (NKE had a great quarter last night – FDX acted well on earnings this week too)

- Short Commodities (we’re still short Oil and Energy related equities)

- Out of Fixed Income (we sold all of ours last Friday and might short bonds today if we get our price)

If someone in your workplace is running around like a chicken with their head cutoff this morning, do me a favor and tell them to relax and realize that the way of life we had during free-markets is vanishing. Shhh.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1, $105.99-110.65, $3.52-3.59, $79.01-79.71, $1.31-1.33, 1.70-1.85%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer