This note was originally published at 8am on December 07, 2012 for Hedgeye subscribers.

Reflexivity. Reflexivity asserts that prices do in fact influence the fundamentals and that these newly-influenced set of fundamentals then proceed to change expectations, thus influencing prices; the process continues in a self-reinforcing pattern.

- Wikipedia

Last night we celebrated another great year, our fifth, at our firm’s annual holiday party. Not thinking ahead, I agreed two days ago to write this morning’s Early Look. Keith was proactively managing risk, as usual.

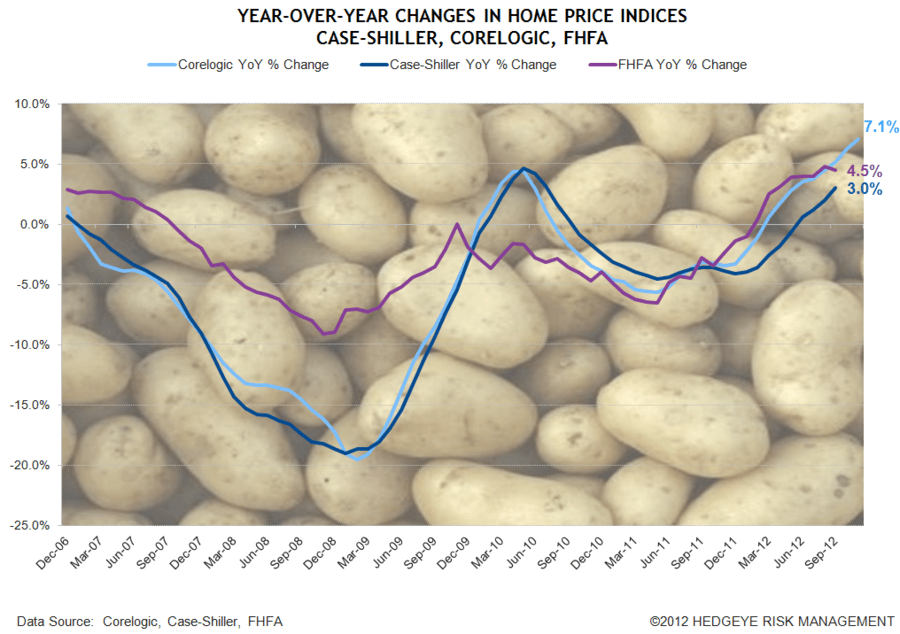

Housing has been in the news a lot recently. A few days ago, Corelogic reported that home prices had risen 6.3% in October vs. the prior year, the fastest rate of growth in a long time. What’s more, Corelogic provides an early look into the following month – something they’ve been doing for the last few months – that showed November’s growth is even stronger at +7.1%. Those are some serious numbers. It’s no longer just Wall Street taking notice. Main Street is starting to pay attention too.

Housing is reflexive. I would argue it’s also a Giffen good. Giffen goods are things people buy more of when the price rises. To economists, Giffen goods are a paradox, something that should not/cannot exist. In fact, at one point in time, the only Giffen good thought to have ever existed was potatoes in Ireland during the Great Irish Potato Famine. Economists later published papers on why this wasn’t a Giffen good after all.

Why would anyone buy more of something as the price rises? The short answer is because he or she expects the price to keep rising. Consider some empirical evidence from the housing market. In 1999, the median priced home in the U.S. cost $137,000. That same year, the Mortgage Bankers Association, or MBA, showed that demand for houses, as measured by their mortgage purchase applications index, stood at 276. Fast forward six years, and by 2005 the median priced U.S. home cost $218,000, an increase of 59%. Meanwhile, demand for homes had risen to 471 on the MBA index, an increase of 70%. Apparently, when houses cost 59% more, we choose to buy 70% more of them.

Fast forward another six years, to 2011, and median price had fallen to $165,000, a decline of 24%. Demand? Demand fell to 180, a drop of 62%. So, again, when houses cost 24% less, we bought 62% less of them. It’s pretty clear that housing is, at a most basic level, a Giffen good. Rising prices stoke greater demand, which fuels rising prices. That cycle, of course, works in reverse too.

So, whether it’s reflexive or a Giffen or a potato, it’s with this dynamic in mind that we’re hosting our 11am call this morning entitled “Could Housing’s Recovery Go Parabolic in 2013?” If you’d like to listen, email sales@hedgeye.com.

Our contention is that housing’s positive momentum is accelerating. On the call we’ll explain the underappreciated role being played by falling rates, growing modifications, and the upside potential from credit easing. We’ll also be laying out our new home price models in the context of supply and demand across the three major markets: existing, new and distressed homes. Of course, we’ll also be flagging the stocks we see as major winners from this dynamic.

Taking a step back, it’s worth reminding investors why housing matters. My sector, Financials, is up 21.9% year-to-date. Bank of America is up 88% year-to-date and is trading at a new high for the year. While there are several reasons why, none is more important than the improvement we’ve seen in housing. Housing is still in the early stages of a secular recovery that will last for years. Similarly, Financials are in the early stages of their own recovery. 2012 has been a good year for both so far (after having endured five straight years of misery), and we expect more progress in 2013 fueled largely by housing.

Josh Steiner, CFA

Managing Director