No Current RealTimeAlerts Positions in Europe

With a recent spate of negative Italian data we thought it important to update the macroeconomic imbalances and risks in Italy. Below is a levels chart of Italy’s FTSE MIB index that we think is ripe for a correction given the looming election uncertainty.

As a long-standing member of the PIIGS, one of Italy’s most immediate threats is the upcoming election – including the possibility of a power vacuum alongside the transition away from the current technocratic government of PM Mario Monti (and therefore the reform measures passed during his term). This could jeopardize the stance of its sovereign and banking ratings.

Despite all the noise from former PM Silvio Berlusconi that he’ll make another run as a candidate and speculation around Monti putting his hat in for another term, what’s clear is that Berlusconi and his PDL are trailing badly in the opinion polls. Per Luigi Bersani of the Democratic Party (PD) is the current front-runner and despite Berlusconi’s comeback barks we believe he realizes that he personally has no shot to be elected PM. Yet, because a coalition government will have to be formed, Berlusconi may be thinking that the continuity of a Monti victory could bode well for the country’s health and that more politicking could garner more support for his party. While Berlusconi’s positioning and utterance may not be clear, expect the risk spotlight to turn up as elections are pushed forward (likely on February 17th or 24th) and for Berlusconi's political gravitas to be less than it was in the past.

Just today the Italian Senate approved 2013 budget law, which was largely expected. The bill will go to the Chamber of Deputies for final approval, likely tomorrow. Once the budget law is passed, we expect Monti to resign and the risks ahead of February’s election to heighten investor behavior.

Risk has largely abated across Europe (especially the periphery) since the summer and particular following Mario Draghi September ECB statement (9/6) to buy “unlimited” sovereign debt via the OMT program. In fact if we look at the period since the beginning of September 2012 Italy’s 10YR is down -24% to 4.42% and Sovereign 5YR CDS is down -42% to 269bps over this same period, including Bank CDS down an average -18%. Meanwhile, the broader Italian equity market (FTSE MIB), despite volatile swings is up +8.6%.

Taken together, we see risk in both a pullback in equities as heightening of risk alongside election indecision and the sovereign banking feedback loop (along with Spain) given its high debt load (at 120% of GDP).

Below is an update of the fundamentals we track, most of which continue to show slow to depressed levels, that suggest a return to growth may be further out than consensus currently forecasts.

Growth Slowing - As the data from Reinhart and Rogoff shows, when a country’s sovereign debt load exceeds 90% (of GDP) growth is dramatically impaired. We think the market will continue to punish Italy via higher servicing costs. We expect this red line to continue down and to the right and the country to underperform Bloomberg consensus expectations for -0.70% GDP in 2013.

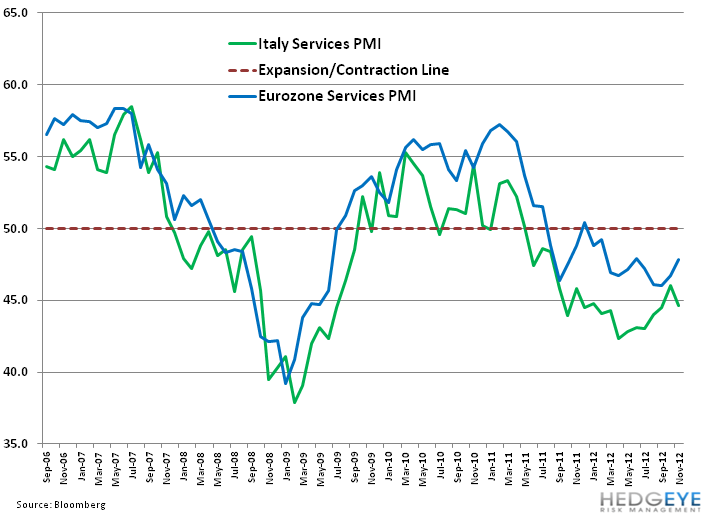

Underperforming Growth - A major leading indicator for growth is derived from PMI surveys. As the two charts below indicate, Manufacturing and Services PMIs are well under the Eurozone averages and have been under the 50 line that divides expansion (above) and contraction (below) since mid 2011.

Labor Cost Inefficiencies - A major factor behind Italy’s slower growth profile is stagnation in its productivity, witnessed by higher unit labor casts, while wages, despite declines, have yet to turn negative.

Economic Confidence Survey - Has trended down since 6/30/11.

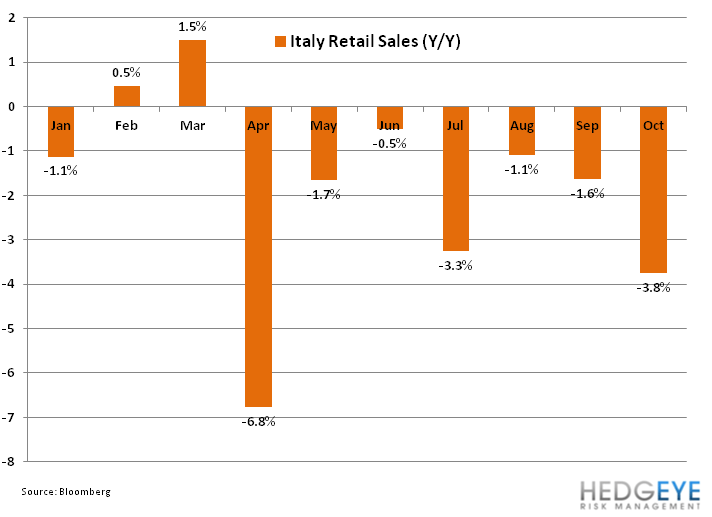

Retail Sales - Negative for 8 of 10 quarters reported this year and accelerating its decline over recent months.

Industrial Production – Slowing and underperforming, continued. A European Commission paper reviewing Italy noted that stagnation in production is the key factor behind Italy’s loss of cost competitiveness since the euro adoption.

New car registrations - Yet another metric we follow. Here again, no surprise, underperformance vs the EU average.

Smashed Piggy Banks - The Italian household savings rate moved from a high of 17.8% in mid 2002 down to 8.1% as of Q3 2011. The chart shows that Italians leveraged their savings in the upturn and in the downturn. The tapping of savings in the last three years demonstrates to pay off debt and the resilience of the Italian consumer to maintain previous spending levels.

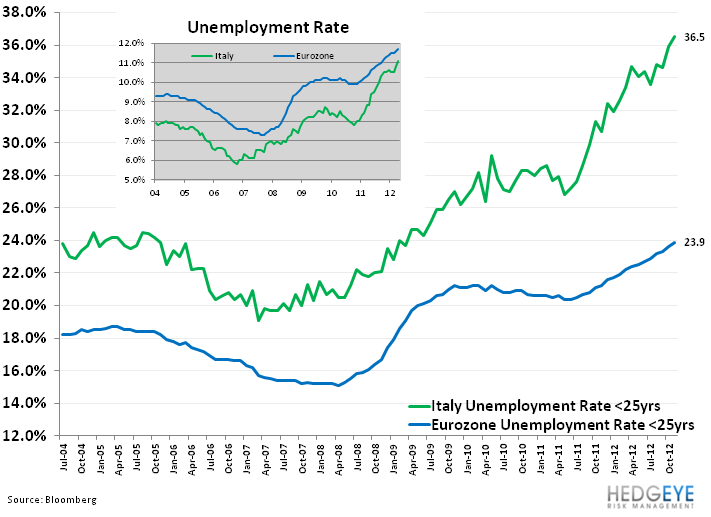

Unemployment Hooking - Another grave dynamic is the underemployment across Italian youths at 37%. While short of the 50% for Spanish youth, combine “a lost generation” with Italy’s demographic headwinds of an aging population (near oldest in Europe) and you have a cocktail that puts great pressure on social services, and the debt and deficit loads in the years ahead.

Matthew Hedrick

Senior Analyst