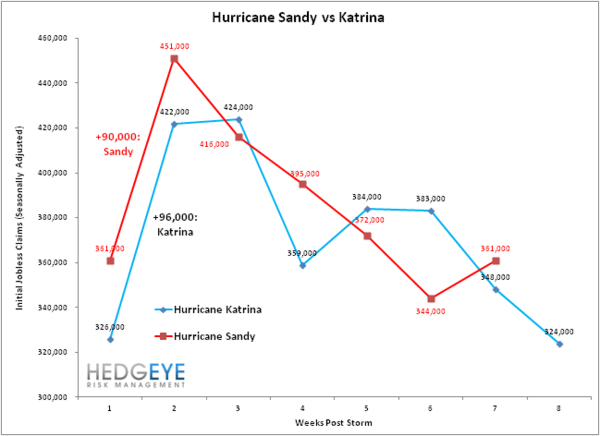

Jobless claims rose 18k to 361k last week, but the 4-week rolling average declined 14k to 368k bringing us back to pre-Hurricane Sandy levels. If we examine state data for NY, NJ and PA, the areas most affected by the storm, they’ve fully re-normalized. Despite the first rise we've seen the past five weeks, we expect claims data will continue moving lower in the coming months thanks to a seasonality distortion tailwind (i.e. holiday help). Add in the positive growth we’ve seen in the housing market recently and financials like Bank of America (BAC) and Citigroup (C) should benefit from the data.